What Is The Difference Between Rich And Wealthy?

.What Is The Difference Between Rich And Wealthy?

Personal Finance - Millionaire Mob - March 8, 2019

Difference Between Rich and Wealthy

Is there a difference between a rich person and a wealthy person?

In this article, we will differentiate between rich and wealthy.

What is the Difference between Rich and Wealthy?

Most people use the two terms rich and wealthy interchangeably. But, do they mean the same thing? There is a difference between rich and wealthy.

In this article, we will focus on some of the significant differences between rich and wealthy

So, who has more money between wealthy and rich people? Before we look at the main differences between the rich and wealthy, let’s first look at the definition of rich and definition of wealthy.

What Is The Difference Between Rich And Wealthy?

Personal Finance - Millionaire Mob - March 8, 2019

Difference Between Rich and Wealthy

Is there a difference between a rich person and a wealthy person?

In this article, we will differentiate between rich and wealthy.

What is the Difference between Rich and Wealthy?

Most people use the two terms rich and wealthy interchangeably. But, do they mean the same thing? There is a difference between rich and wealthy.

In this article, we will focus on some of the significant differences between rich and wealthy

So, who has more money between wealthy and rich people? Before we look at the main differences between the rich and wealthy, let’s first look at the definition of rich and definition of wealthy.

Definition Of Wealthy

Wealthy is a term defined as the number of days that a person can sustain their existence without having to work. The wealthy make money doing nothing and can maintain their standard of living during their life without physically working or anyone in their household physically working.

What matters to the wealthy is not how much money they make, but rather how much money they keep as well as how long that money can work for them.

Can your wealth sustain you and pay for all of your bills for the rest of your life. Can you eat, drink, and travel the world without having to worry about how you will meet all these expenses?

The wealthy do not only have lots of money, but they also don’t worry about money. They can afford all their basic as well as a luxurious lifestyle with no money worries. The wealthy generate a lot of residual income, and their money keeps growing exponentially.

Money works for them and not the other way round. They have excess to keep them going and doing what they want as long as they want and their money does not get diminished. They have infinite wealth.

There are only a few wealthy people around the world. Most of these people were born in wealthy families, and the much they do about it is to maintain their status. However, there is no definite measure of wealthy and different people have varying perceptions on the issue.

Attributes of the Wealthy

Here are some of the characteristics of the wealthy:

Money works for them and is continually invested through fractional share investing

They have accumulated enough money that will likely never run out for the rest of their life

They have created multiple passive income sources

So, let’s have a look at some interesting research findings of the lifestyle of the wealthy people according to a specific group of people.

Research findings on what people believe it means to be wealthy

Here are some thought-provoking results in the survey about what being wealthy meant for different people. While 62% of people said that being wealthy means spending time with family, 55% alleged it as having time to oneself. 49%, on the other hand, believed it means owning a home, and 41% said it means eating out or having meals delivered to you by Uber.

A 33% thought that if you’re wealthy, then you can afford the cable, subscription services like Netflix movie/TV and music streaming and 27% said it means owning the latest tech gadgets. 17% held it means having a gym membership or a personal trainer and 12% said it is means using a home cleaning service.

Almost half of the people who were surveyed believed that to achieve the definition of wealth; one must save and invest money in the right investment vehicles to reap the benefits of compound interest.

Definition of Rich

The rich can be defined as people who have a lot of money which is a characteristic similar to the wealthy. A difference between wealthy and rich is that unlike the wealthy that have a lot of money and fewer expenses, the rich have a lot of money with many financial liabilities and expenses to meet.

Unlike the wealthy, the rich have many bills to pay, and they generally worry about money. Most of the income of the rich end up in the expenses column and not much end up on the assets column. This behavior differentiates the rich vs. wealthy.

Unlike the wealthy that can exist for the rest of their life without worrying about money, the rich worry about several things related to money. They worry about their jobs and businesses as well as how to maintain and manage them to sustain their lifestyle.

The rich can afford all the essentials as well as the luxuries of life, but they must also ensure that their businesses and investments are still running well and the right systems are in place to avoid collapse.

Unlike the wealthy that have enough money at their disposal and don’t have to work to afford luxuries, the rich work and some have even gotten into debts to afford the fine things in life.

A lot of rich people have acquired their money through hard work, and only a few inherited their money. Most rich people must work or get employed to seek the money that they need to maintain their lifestyle.

To continue reading, please go to the original article here:

https://millionairemob.com/difference-between-rich-and-wealthy/

The Worst Things About Being a Millionaire

The Worst Things About Being a Millionaire

Kiplinger's Personal Finance | June 14, 2018 Updated for 2019

Who wants to be a millionaire? The more intriguing question would be, “Who doesn’t?” For most people, a million smackers conjures up images of vacations on the Riviera, Arabian racehorses and mattresses stuffed with freshly ironed $20 bills.

But being a millionaire today isn’t all it’s cracked up to be. Low interest rates and high living costs mean a million bucks in the bank doesn’t necessarily allow you to retire at 35, 45, 55 or even 65.

What’s worse, today’s million dollars comes with all the burdens of wealth: greedy relatives, rapacious lawyers and grasping investment advisers.

The Worst Things About Being a Millionaire

Kiplinger's Personal Finance | June 14, 2018 Updated for 2019

Who wants to be a millionaire? The more intriguing question would be, “Who doesn’t?” For most people, a million smackers conjures up images of vacations on the Riviera, Arabian racehorses and mattresses stuffed with freshly ironed $20 bills.

But being a millionaire today isn’t all it’s cracked up to be. Low interest rates and high living costs mean a million bucks in the bank doesn’t necessarily allow you to retire at 35, 45, 55 or even 65.

What’s worse, today’s million dollars comes with all the burdens of wealth: greedy relatives, rapacious lawyers and grasping investment advisers.

A Million Isn’t What It Used to Be

Financial advisers say a sustainable annual withdrawal from retirement savings is 4%. With a million-dollar nest egg, a 4% draw-down means annual income of $40,000. And that’s before taxes. If you stick with the 4% withdrawal rate and earn an average 8% on your money annually, you’ll be in good shape for the long run.

But can you really live on $40,000 a year? Most millionaires don’t want to. “If you are 45, 50, 55 years old and spend like a millionaire, then you are doing two things with your money that may well not work for you long term,” says Tom Davison, a financial planner in Columbus, Ohio.

“The first is not saving extra dollars now, and the second is establishing a lifestyle cost that, for most people, will be hard to cut back on later.”

That being the case, let’s say you pull $100,000 a year from your savings, you earn 8% a year, and you don’t adjust upward for inflation. Here’s how your account would fare: at the end of Year 1, you'd have $972,000 left; Year 5, $835,735; Year 10, $594,376; Year 15, $239,741; and Year 18, $0. Yup — broke in retirement.

To continue reading, please go to the original article here:

.How Anti-Fragile Are You?

.Notes From The Field By Simon Black

September 24, 2019 Bahia Beach, Puerto Rico

How Anti-Fragile Are You?

I arrived back home to Puerto Rico late last night after traveling back from our Total Access event in Las Vegas.

It was probably around 11:15 pm when I climbed into bed. And, within minutes, just as the sound of the waves outside was carrying me off to sleep, the whole house started violently shaking.

It turned out to be a magnitude 6.0 earthquake, about 20 miles off the west coast of the island.

I lived in Chile for seven years before this-- one of the world’s earthquake capitals-- so I’m no stranger to seismic activity.

Notes From The Field By Simon Black

September 24, 2019 Bahia Beach, Puerto Rico

How Anti-Fragile Are You?

I arrived back home to Puerto Rico late last night after traveling back from our Total Access event in Las Vegas.

It was probably around 11:15 pm when I climbed into bed. And, within minutes, just as the sound of the waves outside was carrying me off to sleep, the whole house started violently shaking.

It turned out to be a magnitude 6.0 earthquake, about 20 miles off the west coast of the island.

I lived in Chile for seven years before this-- one of the world’s earthquake capitals-- so I’m no stranger to seismic activity.

But earthquakes are EXTREMELY rare in Puerto Rico… as in, they almost NEVER happen. People simply do not expect them.

Hurricanes, tropical storms, etc., sure, those are common occurrences here.

And you might remember that Puerto Rico was almost wiped out from 2017’s Hurricane Maria. It devastated the island and much of the Eastern Caribbean, and two years later they still haven’t recovered.

Today there’s supposed to be some Tropical Storm coming through, which, by comparison to Hurricane Maria, is barely a bit of drizzle.

But the government here is on pins and needles, and so anxious to show that they’re ready for anything that they closed schools, many government offices, and even called up the National Guard…

I can’t help but feel bad for them. They’re so scarred from Hurricane Maria two years ago that they overreact in desperation at the first warning sign of a storm.

And then, in an instant, something completely unexpected happened: Puerto Rico was hit with a 6.0 earthquake, and the government has no idea how to react.

I need to caveat all this by saying I really love Puerto Rico. Moving here last year was a great decision. And though I’ve long praised the island’s unparalleled tax incentives, what keeps me living here is the lifestyle.

To continue reading, please go to the original article at

https://www.sovereignman.com/trends/how-anti-fragile-are-you-25620/

To your freedom & prosperity, Simon Black Founder, SovereignMan.com

.Money Can Kind Of Buy Happiness After All

.Money Can Kind Of Buy Happiness After All

By Kelsey Piper Sep 23, 2019, 8:00am EDT

It turns out money can kind of buy happiness after all

A new paper argues that, actually, winning the lottery totally does make you happy.

Does winning the lottery even make you happier? For a long time, researchers said no. Research hadn’t found any conclusive evidence that people who won large sums of money were happier afterward. There was even some evidence they were worse off.

This fact became widely known, partially because it’s so appealing to many people. It’s nice to think that life satisfaction isn’t just about how much money you have, that other things matter more, that we can’t solve all our problems with a sudden infusion of cash.

Money Can Kind Of Buy Happiness After All

By Kelsey Piper Sep 23, 2019, 8:00am EDT

It turns out money can kind of buy happiness after all

A new paper argues that, actually, winning the lottery totally does make you happy.

Does winning the lottery even make you happier? For a long time, researchers said no. Research hadn’t found any conclusive evidence that people who won large sums of money were happier afterward. There was even some evidence they were worse off.

This fact became widely known, partially because it’s so appealing to many people. It’s nice to think that life satisfaction isn’t just about how much money you have, that other things matter more, that we can’t solve all our problems with a sudden infusion of cash.

But there’s a problem with that research: It’s probably wrong. At least, that’s what is argued by economists Andrew J. Oswald and Rainer Winkelmann at the University of Warwick in the new academic book The Economics of Happiness.

Their chapter in the book makes the case that past research about the lottery was badly designed, which is why it found the counterintuitive conclusion that lottery winnings don’t make us happy, instead of the much more boring truth: They totally do.

Economists have good reason — beyond just curiosity — to care whether lottery winners are happier than the rest of us. Lottery winners represent a great chance to explore whether increases in income make people happier.

We know that there’s a well-established association between higher income and happiness, but it can be tricky to say for sure that it’s the higher income that causes happiness.

Maybe happier people earn more money, or depressed people tend to earn very little money, or people with some general quality of life successfulness will be both happy and rich.

Lottery winners are selected at random, so they can help answer this question for us: Does money cause happiness?

Here’s what we know about the effects of lottery winnings

The first paper to take a serious look at the happiness of lottery winnings was a 1978 paper by Philip Brickman and colleagues, titled “Lottery winners and accident victims: Is happiness relative?”

To continue reading, please go to the original article at

https://www.vox.com/future-perfect/2019/9/23/20870762/money-can-buy-happiness-lottery

.How Much Money Do You Need To Feel Wealthy?

.How Much Money Do You Need To Feel Wealthy?

By RETIREBYFORTY

Last time, I asked – Can YOU become a millionaire? Incredibly, 95% of voters picked yes. That’s awesome, I love it! It really isn’t that hard to become a millionaire in the U.S. if you make at least a median household income of $60,000/year. You just have to commit to saving and you’ll get there.

The point of the previous post was for you to pick yes. Unfortunately, a million dollars doesn’t go as far as it used to. Most people don’t even consider a million dollars wealthy anymore. So how much money do you need to feel wealthy? Let’s check it out.

*This post was originally written in 2013. I’ve updated and expanded it with the latest info. I hope you enjoy this one.

How much money do you need to feel wealthy?

$3 million+ (28%, 555 Votes)

$5 million+ (26%, 529 Votes)

$10 million+ (29%, 579 Votes)

$100 million!!! (7%, 147 Votes)

2-3 times what you have now (3%, 69 Votes)

Total Voters: 2,007

How Much Money Do You Need To Feel Wealthy?

By RETIREBYFORTY

Last time, I asked – Can YOU become a millionaire? Incredibly, 95% of voters picked yes. That’s awesome, I love it! It really isn’t that hard to become a millionaire in the U.S. if you make at least a median household income of $60,000/year. You just have to commit to saving and you’ll get there.

The point of the previous post was for you to pick yes. Unfortunately, a million dollars doesn’t go as far as it used to. Most people don’t even consider a million dollars wealthy anymore. So how much money do you need to feel wealthy? Let’s check it out.

*This post was originally written in 2013. I’ve updated and expanded it with the latest info. I hope you enjoy this one.

How much money do you need to feel wealthy?

$3 million+ (28%, 555 Votes)

$5 million+ (26%, 529 Votes)

$10 million+ (29%, 579 Votes)

$100 million!!! (7%, 147 Votes)

2-3 times what you have now (3%, 69 Votes)

Total Voters: 2,007

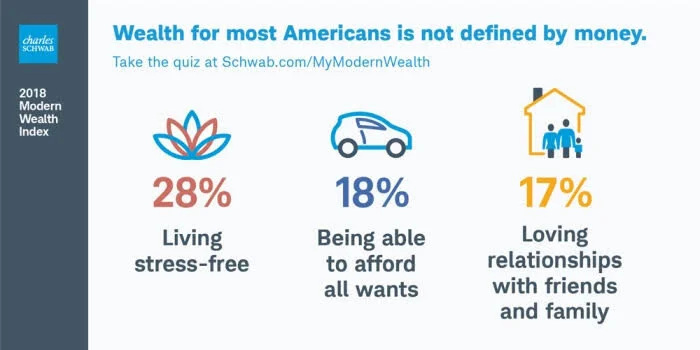

Wealth Isn’t All About Money

Of course, wealth isn’t all about money. Health, relationships, freedom, and happiness are all integral parts of wealth. Money won’t make you feel wealthy if you’re missing some of these. When asked about wealth in Charles Schwab’s 2018 Modern Wealth Index survey, two of the top three answers weren’t related to money.

Wealth Not All About Money

Those things are more difficult to measure, though because they are all subjective. We all have different definitions of happiness. My happiness doesn’t necessarily match yours.

In fact, I think the pursuit of happiness is misguided. We can’t measure those other things, so we’ll just focus on the money today. It’s way easier to figure out net worth than happiness.

When asked to focus on just the money, respondents said it takes $2.4 million to be considered wealthy.

I Don’t Feel Wealthy

Really, $2.4 million? That seems a tad low to me. Our net worth is over that line and I don’t feel rich at all. The problem is the survey is meant to be representative of the US population.

That means most of those surveyed are not millionaires. $2.4 million sounds like a lot of money to regular people, but millionaires don’t consider that wealthy.

Being wealthy is actually a moving target. It turns out most people need twice or more of their current net worth to feel wealthy. If someone is worth $5 million, they would say wealthy means $10 million. That’s pretty funny, isn’t it?

The 2x wealth corollary is pretty much spot on for me. When I wrote this in 2013, our net worth was about $1.5 million. I thought we’d feel wealthy when our net worth reaches $3 million.

Today, I think $3 million is merely comfortable, not wealthy. Like I said, it’s a moving target. However, I’m pretty sure I’ll feel wealthy when we hit $5 million…

UBS Wealth Study

To back up my $5 million = wealthy theory, here is a wealth study from UBS in 2013. It’s a bit older, but investors agreed that wealth isn’t just about having a certain amount of money.

The majority of investors define wealth as having no financial constraints on what they do. But when asked to assign a dollar amount to being wealthy, they say it takes $5 million.

This study targeted investors so the results skewed a bit higher. Investors surveyed were older than 25 years old and have at least $250,000 in investable assets; half have at least $1 million in investable assets. This group is doing a lot better than the average American household.

To continue reading, please go to the original article at

.Can You Become A Millionaire?

.Can You Become A Millionaire?

By RETIREBYFORTY

Recently, I saw a question on Twitter – Can anyone become a millionaire? My gut instinct said yes. I was sure anyone can become a millionaire if they just save and invest consistently. Inflation alone will make the millionaire status much easier to attain in 30 years.

Everyone will make a lot more money so it shouldn’t be that hard. That was my reply. However, there were a few dissenting opinions. I didn’t have any research to back it up so I didn’t argue and let it go.

Today, we’ll take a closer look and see if anyone can really become a millionaire. First, we’ll crank some numbers and then look at the psychological side of this question.

Median income

Let’s look at the average case first to see if they have a chance to become a millionaire. We’ll call our average family the Joneses. The median household income in the US is about $60,000 per year. Median household income means that half of the population makes more than this and half makes less. It’s the middle line.

That’s how much the Joneses make. If the Joneses save and invest consistently, can they become millionaires?

Can You Become A Millionaire?

By RETIREBYFORTY

Recently, I saw a question on Twitter – Can anyone become a millionaire? My gut instinct said yes. I was sure anyone can become a millionaire if they just save and invest consistently. Inflation alone will make the millionaire status much easier to attain in 30 years.

Everyone will make a lot more money so it shouldn’t be that hard. That was my reply. However, there were a few dissenting opinions. I didn’t have any research to back it up so I didn’t argue and let it go.

Today, we’ll take a closer look and see if anyone can really become a millionaire. First, we’ll crank some numbers and then look at the psychological side of this question.

Median income

Let’s look at the average case first to see if they have a chance to become a millionaire. We’ll call our average family the Joneses. The median household income in the US is about $60,000 per year. Median household income means that half of the population makes more than this and half makes less. It’s the middle line.

That’s how much the Joneses make. If the Joneses save and invest consistently, can they become millionaires?

Here are my assumptions

The Joneses will receive a 3% raise every year. This really isn’t much. It’s barely beating inflation, which is around 2%. I assume the Joneses will keep their saving rate steady. When they get any annual raises, they’ll save a bit more.

They’ll invest in the stock market and generate 8% return every year.

I’ll graph it out. We’ll see how long it’ll take the Joneses to reach millionaire status with different saving rates.

Ha! It is as I suspected. The Joneses can become millionaires in 31 years if they religiously save 10% of their income. The more they save, the faster they’ll become a millionaire.

Saving Rate Millionaire in

10% 31 years

20% 23 years

30% 20 years

40% 17 years

50% 15 years

From this table, it looks to me like anyone who makes median income AND is under 30 can easily become a millionaire. Saving 10% really isn’t that difficult at that level of income.

Of course, I recommend saving much more than that in order to achieve financial independence in a reasonable timeframe. You really should aim to save 50% of your income.

To continue reading, please go to the original article at

.Cheapest U.S. Cities for Early Retirement 2019

.Cheapest U.S. Cities for Early Retirement 2019

By Stacy Rapacon, Online Editor Kiplinger| July 4, 2019

Early retirement can be more than just a daydream for those long Tuesday afternoons at work. With some smart planning, you can make leaving the workforce early a reality. You just have to keep in mind the unique challenges facing early retirees.

First of all, entering retirement at a relatively younger age means needing to stretch your nest egg further (hopefully). One way to do that is to find the right retirement destination for you. That's because where you live makes a big impact on your budget. After all, settling down in a place where the cost of living is below the national average means your retirement savings pack in more purchasing power.

With that in mind, we pinpointed 50 great places in the U.S. for early retirees—one in each state—focusing on living costs, median incomes and poverty rates for residents ages 45 to 64, as well as local tax environments and labor markets (just in case you want a second act to stretch your retirement savings further).

Of our 50 picks, these 31 destinations offer particularly low living costs, which heightens the chances of your money lasting through your extra-long retirement and beyond. The list is ordered alphabetically by state.

Cheapest U.S. Cities for Early Retirement 2019

By Stacy Rapacon, Online Editor Kiplinger| July 4, 2019

Early retirement can be more than just a daydream for those long Tuesday afternoons at work. With some smart planning, you can make leaving the workforce early a reality. You just have to keep in mind the unique challenges facing early retirees.

First of all, entering retirement at a relatively younger age means needing to stretch your nest egg further (hopefully). One way to do that is to find the right retirement destination for you. That's because where you live makes a big impact on your budget. After all, settling down in a place where the cost of living is below the national average means your retirement savings pack in more purchasing power.

With that in mind, we pinpointed 50 great places in the U.S. for early retirees—one in each state—focusing on living costs, median incomes and poverty rates for residents ages 45 to 64, as well as local tax environments and labor markets (just in case you want a second act to stretch your retirement savings further).

Of our 50 picks, these 31 destinations offer particularly low living costs, which heightens the chances of your money lasting through your extra-long retirement and beyond. The list is ordered alphabetically by state.

Huntsville, Ala.

Total Population: 444,908

Share Of Population, Age 45 To 64: 27.8% (U.S.: 26.1%)

Retired Cost Of Living: 5.4% Below The National Average

Median Income, Age 45 To 64: $77,266 (U.S.: $69,909)

State's Retiree Tax Picture: Tax Friendly

As one of the 10 Cheapest States Where You'll Want to Retire, the Heart of Dixie boasts many great spots for affordable living. And Huntsville, in northern Alabama, is one of the best. It offers all the low-cost, low-tax advantages as the rest of the state, but adds more generous household incomes.

Home to NASA's Marshall Space Flight Center, the Redstone Arsenal and the Huntsville campus of the University of Alabama, the city offers a robust economy and a highly educated population.

You can also find plenty of cultural attractions, from a sculpture trail to a symphony orchestra, as well as opportunities for outdoor recreation (think bass fishing). In fact, Alabama at-large offers many of Florida's popular retirement attractions—warm weather, nice beaches and plenty of golf—all at a typically lower price.

To continue reading, please go to the original article at

.Crypto-Fiat Currency is a Disaster for Your Privacy

Crypto-Fiat Currency is a Disaster for Your Privacy

By Chris Lowe, Editor, Inner Circle Sep 12, 2019, 8:08 am EDT

We’re not the first to worry about financial privacy in a digital world

Imagine a new type of cash…

Unlike the kind you carry in your wallet, it exists only in digital form.

There’s no more need for ATMs. Tip jars are a thing of the past. Even vending machines are digital.

Every time you spend money, it’s through a digital app. And it’s recorded in a government database.

Crypto-Fiat Currency is a Disaster for Your Privacy

By Chris Lowe, Editor, Inner Circle Sep 12, 2019, 8:08 am EDT

We’re not the first to worry about financial privacy in a digital world

Imagine a new type of cash…

Unlike the kind you carry in your wallet, it exists only in digital form.

There’s no more need for ATMs. Tip jars are a thing of the past. Even vending machines are digital.

Every time you spend money, it’s through a digital app. And it’s recorded in a government database.

The feds collect and store details on every transaction you make. They also know exactly where you are in the world every time you buy something.

In today’s dispatch, I (Chris) will show you why this scenario is already becoming a reality around the world… and why it’s a disaster if you value your liberty.

Then tomorrow, we’ll look at why it’s coming to America… and what you can do about it.

We’re not the first to worry about financial privacy in a digital world…

A pioneering computer scientist called Paul Armer sounded the alarm on this back in the 1970s.

In the 1950s and 1960s, Armer headed the computer science departments at the RAND Corporation think tank and at Stanford University.

Then, in 1975, he issued a chilling warning about what would happen to our privacy if governments ditched physical cash and moved to a purely digital money system.

In an article titled “Computer Technology and Surveillance,” Armer said such a system would become a powerful surveillance tool for the state.

This wasn’t lost on the KGB….

In 1971, Russia’s secret police tasked a group of advisors to devise a plan.

KGB higher-ups wanted to figure out how to create a surveillance system that would keep track of everyone inside the U.S.S.R. without them knowing about it.

The computer scientists’ proposed solution was to get rid of physical cash and replace it with digital currency transactions. As Armer wrote…

To continue reading, please go to the original article at

https://investorplace.com/2019/09/crypto-fiat-currency-is-a-disaster-for-your-privacy-lrg/

.How the Feds Can Finally Win Their War on Cash

.How the Feds Can Finally Win Their War on Cash

By Chris Lowe November 28, 2018

Say goodbye to the dollars in your wallet… Why governments hate cash and cryptos… Last chance to join Bill, Doug, and Mark in tonight’s special broadcast… In the mailbag: “Your freedom ends as soon as it crosses into mine”…

We’re living in a Surveillance Society…

When we left off yesterday, we were discussing the Surveillance Society – the Deep State’s attempt to monitor, record, and process everything you say and do.

Every search you make on Google… every page you like on Facebook… every purchase you make with a credit or debit card… every song you listen to on iTunes… every show you watch on Netflix… every email you send… every phone call you make – your digital activity is being watched and tracked around the clock.

How the Feds Can Finally Win Their War on Cash

By Chris Lowe November 28, 2018

Say goodbye to the dollars in your wallet… Why governments hate cash and cryptos… Last chance to join Bill, Doug, and Mark in tonight’s special broadcast… In the mailbag: “Your freedom ends as soon as it crosses into mine”…

We’re living in a Surveillance Society…

When we left off yesterday, we were discussing the Surveillance Society – the Deep State’s attempt to monitor, record, and process everything you say and do.

Every search you make on Google… every page you like on Facebook… every purchase you make with a credit or debit card… every song you listen to on iTunes… every show you watch on Netflix… every email you send… every phone call you make – your digital activity is being watched and tracked around the clock.

There are also hundreds of millions of cameras and microphones in smartphones, laptops, and “smart devices” such as Amazon’s Echo, Google Home, or Facebook’s Portal.

And with the new advances in facial recognition we’ve been telling you about… odds are you’ll show up on one of America’s 30 million CCTV cameras. (That’s one for roughly every 11 citizens.)

The U.S. Surveillance Society is already formidable. And it’s about to get even more formidable… as the feds come after the last refuge of financial privacy – cash.

Before we get to that, a final reminder about tonight’s special broadcast…

Tonight at 8 p.m. ET, we’re hosting an evening with Bill Bonner, Doug Casey, and Mark Ford.

It’s a rare chance to hear these three legendary newsletter men and self-made millionaires share their secrets about business, investing, and life that I (Chris) think you’re going to love.

You will also have the opportunity to “partner” with Bill, Doug, and Mark on a new venture they’ve been keeping under wraps until now.

Now, back to why the feds want to kill cash…

Cash is a remnant of the analog age. That makes it a safe haven from digital snooping.

Take a stack of $50 bills from under your mattress… buy something with them… and the feds can’t easily track you.

To continue reading, please go to the original article at

https://www.legacyresearch.com/the-daily-cut/how-the-feds-can-finally-win-their-war-on-cash/

.Your Savings Are at Risk in the Cashless World That’s Coming

Your Savings Are at Risk in the Cashless World That’s Coming

Chris Lowe Investor Place September 13, 2019

They’re Coming For Your Money – Every Last Cent…

That may sound like a weird, tinfoil-hat type of thing to say.

But it’s what’s at stake in the War on Cash.

As we’ve been showing you, governments are planning to seize control of your wealth by getting rid of banknotes and coins.

That means no more Ben Franklins. No more nickels and dimes. Nothing but electronic 1s and 0s in a government database.

Your Savings Are at Risk in the Cashless World That’s Coming

Chris Lowe Investor Place September 13, 2019

They’re Coming For Your Money – Every Last Cent…

That may sound like a weird, tinfoil-hat type of thing to say.

But it’s what’s at stake in the War on Cash.

As we’ve been showing you, governments are planning to seize control of your wealth by getting rid of banknotes and coins.

That means no more Ben Franklins. No more nickels and dimes. Nothing but electronic 1s and 0s in a government database.

In a purely digital-currency world… the feds will be able to track, monitor, and record all your financial transactions.

Worse, your savings will be subject to whatever crazy policies central bankers come up with to cope with the next financial crisis… with little chance of escape.

Think of this as a “digital slaughterhouse”…

It’s a term I (Chris) borrowed from currency expert Jim Rickards. As he put it…

When pigs are going to be slaughtered, they are first herded into pens for the convenience of the slaughterhouse. When savers are going to be slaughtered, they are herded into digital accounts from which there is no escape.

As I showed you yesterday, this is a trend already in motion.

https://investorplace.com/2019/09/crypto-fiat-currency-is-a-disaster-for-your-privacy-lrg/

China plans to roll out a fully digital version of its currency in November. Canada, Britain, Norway, and Sweden are also looking into purely digital versions of their national currencies.

Today, I’ll show you why these countries are creating a roadmap that other governments – including in the U.S. – will follow.

https://finance.yahoo.com/news/savings-risk-cashless-world-coming-144512361.html

.Laurentian Bank Will Not Accept Rolled Change For Deposit

Laurentian Bank Will Not Accept Rolled Change For Deposit

Montreal man has $800 in rolled change, but his bank won't deposit the money

Lauren McCallum, Verity Stevenson 2 days ago

Julien Perrotte brings rolled change to his bank each year. But now, Laurentian Bank says it will not deposit the coins into his account.

Julien Perrotte stood in front of the representative at his local bank last week, unsure he properly understood what she was telling him.

He was carrying about $800 worth of coins, sorted and rolled, that he had collected over the past year. But she said Laurentian Bank wouldn't deposit them.

"I'm like, 'It doesn't make sense,'" Perrotte told CBC News.

Laurentian Bank Will Not Accept Rolled Change For Deposit

Montreal man has $800 in rolled change, but his bank won't deposit the money

Lauren McCallum, Verity Stevenson 2 days ago

Julien Perrotte brings rolled change to his bank each year. But now, Laurentian Bank says it will not deposit the coins into his account.

Julien Perrotte stood in front of the representative at his local bank last week, unsure he properly understood what she was telling him.

He was carrying about $800 worth of coins, sorted and rolled, that he had collected over the past year. But she said Laurentian Bank wouldn't deposit them.

"I'm like, 'It doesn't make sense,'" Perrotte told CBC News.

The woman told him he could exchange the coins for bills at local grocery stores, corner stores and pharmacies because "they love coins."

But Perrotte, who works as an independent insurance claims adjuster, says he doesn't have time to shop around for a small business to take his change — especially when it's a service he expects to receive from his bank.

He called Laurentian Bank's customer service line to see if there was any other way the bank would take his hundreds of loonies and toonies.

He was told it was a new policy at the bank not to accept coins.

"Pretty much, I was exasperated," said Perrotte, who has been a member of Laurentian Bank for 15 years.

"It's so absurd.… Everyone has coins, that's for sure. Poor people, rich people."

The other option Perrotte considered was to exchange the coins at a Coinstar machine, which are at some grocery stores and malls, but the machines charge about 12 per cent in fees for the service.

"So I would lose like 80 bucks just to try to get rid of money. And my bank doesn't want my money!" Perrotte said.

Some bank branches going cashless

As Perrotte points out, the Royal Canadian Mint is still producing coins as legal tender. But he now wonders who is ensuring that banks will take them.

He's worried other banks will follow Laurentian's lead.

In a response to a request for comment from CBC News, Royal Canadian Mint spokesperson Alex Reeves said the Crown corporation's mandate is limited to manufacturing and distributing Canadian currency.

To continue reading, please go to the original article at