How The World Is Starting To Look Like 1492 All Over Again

How The World Is Starting To Look Like 1492 All Over Again

Notes From the Field By James Hickman (Simon Black / Sovereign Man) May 14, 2026

In the year 1484, a thirty-something year old sailor from Genoa was working in Lisbon when he stumbled upon a bold idea. For the previous decade, he had served as a crewman on several Portuguese commercial expeditions to haul physical resources like gold, ivory, and fish from Asia back to European ports.

These voyages were treacherous; they all crossed into maritime territory controlled by the Venetians, Ottomans, or Egyptian Malmuk. So there was a high likelihood of a vessel being confiscated and its crew being captured or killed.

How The World Is Starting To Look Like 1492 All Over Again

Notes From the Field By James Hickman (Simon Black / Sovereign Man) May 14, 2026

In the year 1484, a thirty-something year old sailor from Genoa was working in Lisbon when he stumbled upon a bold idea. For the previous decade, he had served as a crewman on several Portuguese commercial expeditions to haul physical resources like gold, ivory, and fish from Asia back to European ports.

These voyages were treacherous; they all crossed into maritime territory controlled by the Venetians, Ottomans, or Egyptian Malmuk. So there was a high likelihood of a vessel being confiscated and its crew being captured or killed.

But through his marriage into a Portuguese navigator's family, this sailor had inherited a small library of nautical charts. And he spent years studying them and corresponding with scientists who studied cosmology.

Over time, he became convinced that a small fleet could reach Asia by sailing WEST, not east, and arrive to the spice markets of the Indies without passing through enemy territory.

The sailor’s name was Christopher Columbus. And he took his idea to the King of Portugal, John II.

The King was interested enough to convene a royal panel, but the ‘experts’ decided that Columbus had badly underestimated the size of the Earth and recommended against funding the voyage.

Columbus spent the next several years pitching his idea to anyone who would listen.

He sent his brother to make the case to Henry VII in England. He approached the French court. He crossed the border into Spain, secured an audience with Ferdinand and Isabella at Córdoba, and watched a second royal commission argue for nearly four years... before rejecting him for the same reasons the Portuguese had.

He gave up on Spain and was riding north to try the French court again when a royal courier caught up with him. Ferdinand and Isabella had just taken Granada on January 2, 1492 — a conquest that ended a decade-long war and brought the southern Mediterranean coast and its ports under their control.

With the war finally over and the southern frontier secured, the monarchs had excess cash to fund the next strategic venture.

So in April of that year, at the siege camp of Santa Fe outside Granada, Isabella signed the contract. A few months later, three small ships set sail— with the crew probably all assuming that they would not survive the voyage.

The Spanish crown’s investment paid off... and they spent the next century pulling staggering amounts of silver and gold out of the new continent Columbus had stumbled upon; Spain became the wealthiest power in Europe as a result.

This is how governments used to invest. They were like venture capital funds of their day, financing long-term bets on ports, territory, trade routes, and resources, all in an effort to secure strategic assets that compound over generations.

But for the last eighty years or so, the world has run a different experiment.

After 1945, the United States built a system in which the rest of the world manufactured goods, sold them to American consumers, and recycled their trade surpluses back into US Treasury bonds.

This system worked for decades; in fact the most rational thing a foreign government could do with its national savings was invest in US dollars and US government bonds. Any foreign country with a stockpile of Treasurys was considered stable and creditworthy.

But this system is now cracking. Rapidly.

After the Biden administration froze Russia's dollar reserves in 2022, foreign central banks understood that US government bonds were ‘safe’ only as long as their country stayed on America's good side.

Consequently, most foreign governments have been diversifying out of dollars ever since.

This year's Iran war drove the lesson home: the Strait of Hormuz, the narrow waterway through which roughly a quarter of the world's seaborne oil passes, has been closed since late February.

And every foreign country holding hundreds of billions of US government bonds has been reminded that, no matter how big their Treasury stockpile, they cannot feed their population with it. They cannot fill their people’s gas tanks with it. They cannot power homes with it.

So governments are reconsidering their US dollar positions more than ever.

Just like Ferdinand and Isabella, governments around the world started by acquiring gold; central banks have been buying it at the fastest pace in modern history since 2022.

But gold is only the leading indicator.

The next phase is foreign governments and central banks stockpiling other critical resources and materials— energy, fertilizer, copper, uranium, rare earths, food production, and even fresh water.

These are all strategic assets that no government can conjure out of thin air. And no amount of paper bonds can magically summon.

China has been running this playbook for fifteen years: they’ve purchased farmland in Africa, copper concessions in the Congo, rare-earth processing across central Asia, and the Belt and Road infrastructure that physically connects the resource to the buyer.

A large part of China’s investment capital has come from their steady liquidation of US Treasury holdings.

This is the Columbus-era calculus all over again. Whereas governments around the world used to stockpile US government bonds, they are now stockpiling strategic resources.

One obvious consequence is lower demand for US government bonds— which drives up interest rates, mortgage rates, and more. It probably also leads to a lot more inflation, i.e. the 1970s all over again.

But it also means that these critical resources— and the companies which produce them— should have a very, very bright future as foreign governments throw potentially trillions of dollars at the commodities sector.

This is the primary thesis behind Schiff Sovereign's monthly investment research service, Strategic Assets.

We look for profitable, well-managed real-asset businesses with pristine balance sheets that are trading at a low multiple of free cash flow— with clear catalysts for growth.

And those catalysts include our fragmenting world and the scramble to secure physical, critical assets.

To your freedom,

James Hickman Co-Founder, Schiff Sovereign LLC

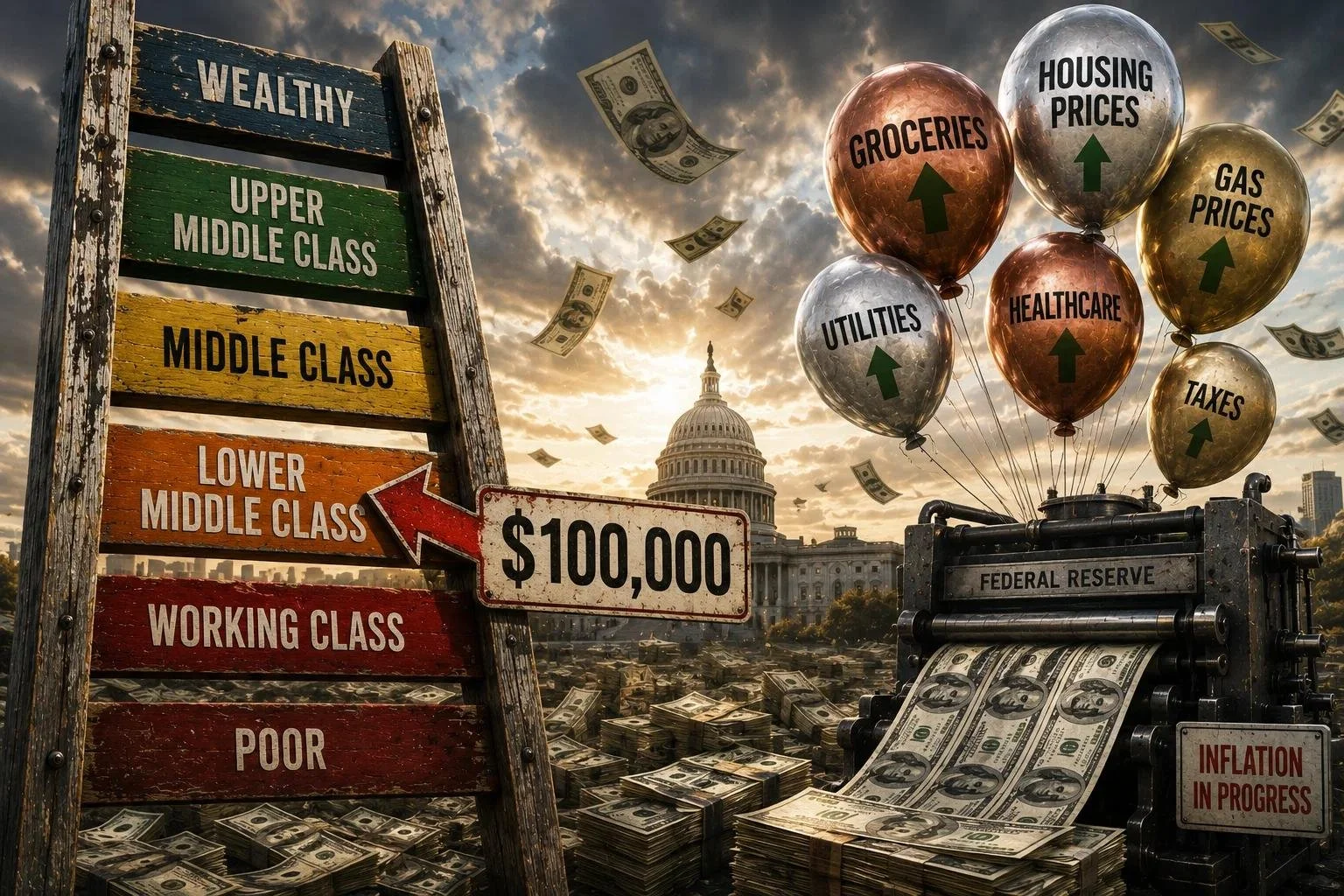

$100,000 Income is Now "Lower-Middle Class"

$100,000 Income is Now "Lower-Middle Class"

Notes From the Field By James Hickman (Simon Black/Sovereign Man) May 12, 2026

Henry VIII probably thought he was being extremely clever when he started debasing his currency in 1544... and assumed that, if he reduced the silver content slowly and gradually enough, perhaps no one would notice.

But the King was hilariously wrong.

$100,000 Income is Now "Lower-Middle Class"

Notes From the Field By James Hickman (Simon Black/Sovereign Man) May 12, 2026

Henry VIII probably thought he was being extremely clever when he started debasing his currency in 1544... and assumed that, if he reduced the silver content slowly and gradually enough, perhaps no one would notice.

But the King was hilariously wrong.

Despite centuries of warfare, invasions, and plagues, English rulers prior to Henry had been remarkably disciplined in maintaining 92.5% silver in their coins.

In fact, England’s kings were so serious about their coinage that, at one point in the 1100s, one of Henry VIII’s forebears rounded up every private minter who skimped on the silver content in their coins— and had the man’s testicles removed.

But Henry VIII did not share his ancestors resolve. So, drowning in debt, divorce, and too much war, he started to reduce the silver content and replace it with copper.

His new coins still looked vaguely similar to the original ones because they were given a cheap, silver wash. But the wash wore off quickly— especially on the side where Henry’s profile was carved.

Londoners soon began to notice that the king’s nose would turn orange once the silver sheen wore off, giving rise to the nickname “Old Coppernose”.

And yet the debasement continued— and this was Henry’s ‘clever’ idea.

There wasn’t a single shock or dramatic crash. Henry’s ‘Great Debasement’ was a years-long operation of slowly robbing prosperity from his subjects. Each year their coins would buy less. Prices would rise. Their cost of living increased. And overall they were worse off.

This is the same story of our own time.

Gallup reported last week that 55% of Americans believe their personal finances are getting worse; that’s the absolute rock bottom reading in 25 years of the survey.

It is worse than 2008, when the financial system was actually breaking. It is worse than the pandemic, when the economy was shut off.

And that 55% statistic is in a year when headline employment numbers and stock indices are supposed to be telling everyone they're doing fine.

Perhaps even more alarming is a recent analysis by a group called MoneyLion, which looked at Census data and found that, in 12 states in the US, a $100,000 income is now considered LOWER middle class.

For those who remember what life was like 25 years ago, making six figures was solid “made it” territory.

Not anymore. In Massachusetts, the lower-middle ceiling has crept up to $116,476. In New Jersey, $115,882. In California, $111,277.

Of course, it isn't hard to see what those states have in common. They tax heavily, regulate aggressively, and treat business and wealth as plump dairy cows to milk.

This isn’t magically going away if the Strait of Hormuz opens, or Congress passes a ban on corporations buying homes to rent.

The federal government runs trillion-dollar deficits every year, the Treasury borrows the difference, and the Federal Reserve accommodates the whole arrangement by expanding the money supply by trillions.

Long term inflation doesn't slow down until Washington decides to be fiscally responsible— and there is little evidence that's about to happen.

If you bought a house in 2010, or even 2021, the same forces hollowing out the dollar have been inflating the value of your assets; your house cannot be printed by the Federal Reserve, so as the money supply increases, your house costs more in nominal dollars.

That's why the people who feel worst about this economy are young people.

A recent Generation Lab survey found that more than 8 in 10 Americans aged 18-29 — the cohort least likely to own a home or hold meaningful investments — now describe the economy as bad or terrible. Only 2 percent of them call it "excellent."

This is why real assets matter. The Fed can manufacture as many dollars as it wants, but it cannot manufacture the things that actually have value: precious metals, energy, critical resources like uranium or copper, a profitable business producing something the world cannot function without.

Because every single time governments are given the choice between inflation and discipline, they pick inflation.

And just like Henry VIII, they think no one is going to notice.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

PS — Schiff Sovereign's investment research newsletter, Strategic Assets, exists for exactly this reason: to identify real assets and real businesses that not only protect wealth from debasement, but actually give you tremendous upside as Americans prioritize essential spending over luxuries.

We’ve seen some major winner in precious metals, fertilizer, industrial metals, shipping— and there is reason to believe we are still early.

Mark Zuckerberg Makes a Strong Case for Real Assets

Mark Zuckerberg Makes a Strong Case for Real Assets

Notes From the Field By James Hickman (Simon Black / Sovereign Man) May 7, 2026

Mark Zuckerberg had his hands full last week trying to calm the storm at his company.

In an employee conference call, he had to quell a great deal of panic over the company's performance.

Growth at Facebook/Meta is slowing, the stock price is down, and the company is dealing with significant regulatory and economic headwinds. And workers are unsettled.

Mark Zuckerberg Makes a Strong Case for Real Assets

Notes From the Field By James Hickman (Simon Black / Sovereign Man) May 7, 2026

Mark Zuckerberg had his hands full last week trying to calm the storm at his company.

In an employee conference call, he had to quell a great deal of panic over the company's performance.

Growth at Facebook/Meta is slowing, the stock price is down, and the company is dealing with significant regulatory and economic headwinds. And workers are unsettled.

So Zuckerberg took the mic and tried to assuage those concerns by explaining to everybody why ad revenue growth is slowing.

He said plainly, "If oil prices go up, then consumers spend more of their money on oil, on gas, and less on things that they would just buy that are kind of discretionary things that the advertising might serve."

Without really meaning to, Mark Zuckerberg made a really strong case for real assets.

It ultimately starts with energy costs. Energy costs are higher. And everyone wants to blame Iran and the Strait of Hormuz, but this trend has been building for a long time.

For years, oil was the second most hated asset on the planet, only edged out by coal.

Think about it— liberal elites hold conferences where they fly to dictator states in their private jets, only to parade oil and gas CEOs on stage and publicly shame them.

Then you have the legions of inspired idiots who glitter-bomb art and glue themselves to pavement to stop traffic (ironically increasing emissions), all in the name of "just stop oil."

They deface buildings and commit crimes, but they've been so successful that many oil companies themselves have turned their back on oil.

National governments, especially the previous Biden administration, have gone out of their way to tax, fleece, subvert, frustrate, and publicly ridicule oil companies.

Furthermore, the industry itself has been starved of capital because investors jumped on the bandwagon. Financial institutions stopped making loans, in some cases even debanking oil companies as a ridiculous form of virtue signaling.

Pension funds stopped investing in oil companies. Hedge funds tried to take over oil companies solely to turn them into fantasy green projects.

The dearth of capital— in a capital intensive industry— made it very difficult for exploration companies to finance new discoveries.

Even in the labor market, young people around the world have been so brainwashed that no one wants to go into the oil and gas sector— even though it pays quite well— for fear of public humiliation and "being on the wrong side of history."

To be frank, it's actually kind of extraordinary that an industry deprived of capital and labor, suffering an endless onslaught of media hysteria and political assault, has managed to continue delivering, day after day, the energy that our civilization requires to function.

Blaming today's higher oil prices exclusively on Iran totally misses this history; the problems have been building for years.

Solving this energy challenge will take a long time— to finance new projects, find new discoveries, build the right kinds of infrastructure, and commercialize those discoveries in a way that keeps up with the rising energy demands of a growing world.

In the meantime, higher energy prices increase the production cost of just about everything else— food, housing, automobiles, consumer goods, even your monthly electricity bill. So, in the end, most things become more expensive.

This is ultimately what Mark Zuckerberg was saying— without fully saying it. For years there was an abundance of energy and global cooperation. Combined with low interest rates, the result was negligible price inflation and a feeling of widespread prosperity.

That feeling of prosperity meant consumers had plenty of disposable income for the sorts of things advertisers would sell on platforms like Facebook and Instagram.

As Zuckerberg explained, those same retail-focused companies are now selling to consumers and individuals who have less disposable income— precisely because they have to spend more money on essentials like energy and food.

We've been predicting this for the last several years, and we think this trend will continue for some time.

This is why a very sensible place to consider investing, even if just as a hedge against rising prices, is in the companies that produce these critical resources.

This is the core of our investment ethos, and to be frank, it has been very successful.

We've seen our mining stocks multiply by as much as ten times, with several others doubling, tripling, and quadrupling.

But it goes beyond mining; one agricultural company has doubled, and a fertilizer producer is up double digits in just a few months. We've been collecting dividends from industrial producers while their stocks tick higher.

Only a few companies we have researched are down, and we think they still have plenty of upside.

And we are still finding some really great real-asset businesses that are surprisingly, deeply undervalued. That includes energy companies.

There are a lot of reasons for high quality businesses being undervalued; but I think it's because people believe this is some sort of aberration— that tomorrow the spigots turn on and oil drops back to $40 a barrel.

The reality is all these challenges can be solved, but it's going to take a while. And in the meantime, we think these real-asset companies are going to be cash machines.

Keep an eye on your inbox tomorrow afternoon for the new issue of Strategic Assets about an interesting company that has the potential to capture this mismatch in expectations versus reality.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

The Last Time America Hit 100% Debt-to-GDP, A Golden Age Followed

The Last Time America Hit 100% Debt-to-GDP, A Golden Age Followed

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 30, 2026

In the spring of 1946, hundreds of thousands of American soldiers were coming home from Europe and the Pacific, maimed, bruised, and shell-shocked. The economy they returned to was upside down.

Detroit was making tanks, not automobiles. Factories were making bullets, not baby carriages. Food was rationed. Fuel was scarce. And, overall, life in America had been bleak for the better part of two decades. The Great Depression gave way to a stretch of war that led many Americans to fear that their kids would soon be speaking German and goose-stepping with the Hitler Youth.

The Last Time America Hit 100% Debt-to-GDP, A Golden Age Followed

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 30, 2026

In the spring of 1946, hundreds of thousands of American soldiers were coming home from Europe and the Pacific, maimed, bruised, and shell-shocked. The economy they returned to was upside down.

Detroit was making tanks, not automobiles. Factories were making bullets, not baby carriages. Food was rationed. Fuel was scarce. And, overall, life in America had been bleak for the better part of two decades. The Great Depression gave way to a stretch of war that led many Americans to fear that their kids would soon be speaking German and goose-stepping with the Hitler Youth.

Government finances were equally bleak. Between all of the massive public works programs of the Great Depression and eye-popping costs of World War II, the US national debt topped 100% of GDP by the mid-1940s.

And yet that moment was the beginning of a new Golden Age.

Think about the world at the time: Britain was bankrupt. Germany and Japan had been turned to rubble. And the Soviets had won their part of the war by feeding twenty million bodies into the meat grinder.

America came out the other side with full manufacturing capacity intact, the dollar enthroned as the world's reserve currency, and virtually no economic competition anywhere.

What followed was two decades of suburb-building, highway-laying, automobile-making, and semiconductor-launching prosperity. There were bumps along the way, but on balance the economic trajectory of America was up and to the right.

Consequently, the US national debt started falling. And it’s easy to understand why. By 1946 there was no more war, no more depression.

The United States had just spent four years consuming every available resource to defeat the Nazis. But once the war ended, military spending (and hence the budget deficit) dropped like a rock. Congress started to run budget surpluses and used them to pay down the debt.

Over the next three decades, America’s debt-to-GDP ratio fell from 106% in 1946 to just 23% by the mid-1970s.

This week, fresh data from the Bureau of Economic Analysis confirmed that America's debt-to-GDP ratio has officially crossed 100% once again.

One caveat: this number is based on what the government calls "debt held by the public"; it conveniently leaves out the trillions of dollars that Washington “owes itself”, including Social Security trust fund IOUs, federal pension obligations, and other intragovernmental holdings.

Well, that money has to be repaid too. Pretending otherwise might make the debt appear smaller. But a broader, most honest measure of the debt right now is actually 130% of GDP, well beyond the WWII record.

But fine, we’ll use the government’s official number of 100%, which is just announced this morning.

Yes, America has been here before. 100% is not unprecedented. But there is a major difference.

Back in 1946, the debt was at 100% of GDP because the US had just defeated the Nazis. The debt binge ended when the war ended.

In 2026, the United States is not fighting Hitler. There is no once-in-a-century pandemic. There is no specific crisis that, once over, will allow Congress to bring spending back into line.

Rather, the debt is so high because the debt is so high.

Interest on the federal debt is over $1 trillion per year. That’s a huge chunk of tax revenue. The rest of America’s tax revenue is consumed by mandatory entitlements like Social Security and Medicare.

Literally everything else, including the military, roads, and light bill at the White House, are funded with more debt.

So in other words, the deficit is structural and permanent. It will be there no matter how much Congress cuts... if they were even interested in fiscal reform.

And yet Congress shows no interest in spending cuts. Even when the most rampant and obvious fraud is presented with a bow on it, Congress does nothing.

Even worse— people who actually try to stop the fraud get publicly crucified, arrested, or sued.

In 1946, the political momentum of the United States focused on growth, productivity, and fiscal discipline. In 2026, all of it points the other way.

And the dollar's status as the world's reserve currency— a major advantage that helped pay down the postwar debt— is also slipping.

Foreign central banks have been quietly selling US Treasuries and buying physical gold at the fastest pace in modern history. Since the start of the year, they have unloaded tens of billions of dollars worth of US government bonds, and the interest rate on Treasurys have climbed in response.

That shows how foreign confidence draining out of the dollar in real time.

Now, none of this means the world is ending.

We are not pessimistic people. Humanity's best days are still ahead. The technological advances now arriving in robotics, artificial intelligence, nuclear power, and biotech are not incremental upgrades; they are giant leaps for mankind.

Civilization will improve, productivity will rise, and the economic problems will sort themselves out.

But getting there requires persevering through the next several years of challenges... during which time we expect the average American to see a lower standard of living driven by higher taxes, persistent inflation, and a regulatory burden that gets heavier by the day.

Of the three, inflation looks the most baked in. Foreign governments are abandoning the dollar at a rapid pace, so the Federal Reserve will almost certainly step in to ‘print money’ and bail out the Treasury.

The impact will be more inflation.

This is why we continue to write that real assets are the right place to be. In difficult and conflict-prone times, the basics like food, water, energy, critical industrial metals, and productive technology become the world's most valuable resources. They hold their value regardless of which currency happens to be in fashion, or how high inflation goes.

And the key point is that, right now, many of the best real asset producers— which have huge upside ahead— are trading at absurd discounts. So it’s a great time to consider this strategy.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

The ‘Expert’ Who Said ‘Globalization Would End War’ — 5 Years Before WWI

The ‘Expert’ Who Said ‘Globalization Would End War’ — 5 Years Before WWI

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 28, 2026

In 1909, a British journalist named Norman Angell published The Great Illusion, claiming that war between major global powers had become obsolete. Nations were too interlinked, he argued. Capital was too entangled. Trade was too valuable. And no nation would put that prosperity at risk. War and conquest were things of the past.

But think about the world back then: Europe was in the middle of la Belle Époque, a stretch of unprecedented peace and prosperity. It had been nearly 40 years since the last major war (Franco-Prussian War) in 1871.

The ‘Expert’ Who Said ‘Globalization Would End War’ — 5 Years Before WWI

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 28, 2026

In 1909, a British journalist named Norman Angell published The Great Illusion, claiming that war between major global powers had become obsolete. Nations were too interlinked, he argued. Capital was too entangled. Trade was too valuable. And no nation would put that prosperity at risk. War and conquest were things of the past.

But think about the world back then: Europe was in the middle of la Belle Époque, a stretch of unprecedented peace and prosperity. It had been nearly 40 years since the last major war (Franco-Prussian War) in 1871.

Gold-standard money moved across borders without friction. British capital financed German factories, German banks lent to Russian railways. And one of the largest trading relationships in the world was between supposed rivals Britain and Germany.

Mr. Angell's book sold over two million copies; it was translated into 25 languages and became a fixture in educated households. Diplomats quoted it. CEOs planned around it. Angell’s conclusions seemed true, without question.

Then the Great War broke out five years later, and the world’s great powers went on to vaporize 16 million human beings and their collective economies. Global trade did not recover its 1913 level for roughly half a century.

Bizarrely, Angell later won the Nobel Peace Prize "for having exposed by his pen the illusion of war and presented a convincing plea for international cooperation and peace." There would not be a less deserving recipient until Henry Kissinger and Barack Obama.

But this same mistake has been repeated again in our own time.

After the Soviet Union fell and American technology took the world by storm in the 1990s, it seemed that global peace and prosperity would last forever.

Even after 9/11 and the 2008 Global Financial Crisis, the world organized itself around America’s leadership.

The dollar was the world's dominant reserve currency. The World Trade Organization tore down tariffs across the board. NATO and the United States Navy guaranteed no major power would risk war.

America supplied the security, the currency, and the rules; in exchange, the world traded and grew under an American-led system. Goods, capital, and supply chains ignored borders.

And for decades it worked reasonably well. But we’re now witnessing its breakdown in real time.

As I write this letter to you, gas stations in Asia are rationing fuel. Hospitals are running out of medical supplies. Major petrochemical producers in South Korea and Singapore (Yeochun and PCS) have declared force majeure, meaning they cannot fulfill their commitments to customers.

The cause is simple: the Strait of Hormuz has been closed for weeks.

The Middle East ships roughly 25% of the world's polypropylene, 20% of its polyethylene, 25% of its sulphur, and 15% of its fertilizer. When that flow stops, factories stop. And remember that about half of what Americans buy comes from those same Asian factories.

Capital Economics, a global research firm, estimates that it could take three months for the resulting plastic shortages to spread globally, and four months until US automakers face aluminum shortages severe enough to cut production.

S&P Global's April survey of manufacturers worldwide shows supplier delivery times lengthening at the fastest pace since August 2022.

Purchasing activity is near a four-year high as companies scramble to stockpile while they still can. Respondents are using "panic" and "emergency" buying language for the first time since the pandemic supply crunch— when Americans waited months for a new car, lumber prices tripled, and store shelves sat empty.

Yet rather than work together to ease the strain, governments are making it worse. With trust between major powers in collapse, every cross-border deal is now treated as a security threat... so they are blocking deals, capping technology transfer, and walling off entire industries.

China just blocked Meta's $2 billion acquisition of an AI startup called Manus; Beijing argues that Manus was developed by Chinese founders with Chinese capital, and therefore an American giant cannot own it.

The United States has been doing the same thing for years— to its strongest allies, no less.

The Biden administration blocked Japanese company Nippon Steel's $15 billion acquisition of US Steel on "national security" grounds, even though Nippon had offered to invest $2.7 billion of Japanese capital into Pennsylvania steel mills.

(Trump later reversed this, and the deal went through with additional government stipulations.)

That is what de-globalization actually looks like in practice: not one dramatic rupture, but the slow accumulation of friction— a closed strait here, a blocked deal there, escalating tariffs, sanctions, "national security" reviews.

Stack enough of this friction together and the world looks entirely different.

Travel becomes harder and more expensive. Raw materials and finished goods become costlier. Specialization and trade become economic drags rather than efficiencies as nations are forced to make more things at home— including the goods that other countries can already manufacture more efficiently.

This is already happening, and it’s difficult to fix. It’s unlikely that anyone can wave a magic wand and bring back the geopolitical cooperation that fueled the world for decades.

The world is not coming to an end. Far from it. But it is changing rapidly.

Less cooperation, more conflict, and more tension has profound implications for future prosperity.

One of the obvious implications we see is that real assets— energy, food, gold, industrial metals— grow in value during times of conflict and global friction.

Tension and protectionism don't reduce demand for any of them; they just make supply harder to get, so prices rise. When supply chains snap and borders tighten, these are the assets that benefit most.

So if you agree with our thesis, i.e. that the world is heading towards more conflict and less cooperation, real assets (and the companies which produce them) are an excellent hedge to offset that risk with financial gain.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Why Central Banks Are STILL Dumping Dollars for Gold

Why Central Banks Are STILL Dumping Dollars for Gold

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 22, 2026

In late February 2022, days after Russia invaded Ukraine, the United States responded by freezing billions of dollars of assets owned by the Russian government.

Whether or not that action was justified is beyond the point. US government bonds had long been considered the safest asset on earth. But every central banker on the planet learned an important lesson that day– US Treasury bonds were only safe as long as their country stayed on America’s good side.

Why Central Banks Are STILL Dumping Dollars for Gold

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 22, 2026

In late February 2022, days after Russia invaded Ukraine, the United States responded by freezing billions of dollars of assets owned by the Russian government.

Whether or not that action was justified is beyond the point. US government bonds had long been considered the safest asset on earth. But every central banker on the planet learned an important lesson that day– US Treasury bonds were only safe as long as their country stayed on America’s good side.

Consequently, foreign governments and central banks began quietly moving a portion of their strategic financial reserves into assets that Washington could not freeze or sanction. And the most important of those assets was physical gold.

Within months, the collective buying of foreign central banks was running faster than at any point in modern history.

Compared to a previous baseline of about 650 metric tons per year in 2018 and 2019, central bank gold purchases jumped to over 1,000 tons starting in 2022.

It stayed there through 2023. It hit a record 1,100 tons in 2024. Even in 2025, when gold went parabolic to $4,500 an ounce and they could have paused or even taken profits, they were still net buyers of roughly 800 tons.

Holding Treasury bonds requires trusting that the US government will not freeze their assets, will not weaponize the dollar, and will not run deficits large enough to force the debasement of the dollar itself.

None of those three conditions holds anymore.

The United States ran a $2 trillion deficit last year— no recession, no economic crisis, no war, no bailouts. It was just business as usual. Congress won’t lift a finger to cut even the most blatant fraud and graft.

Consequently, the national debt is now pushing $40 trillion, with interest costs eating $1.2 trillion per year— nearly a quarter of total tax revenue. And foreigners are rapidly losing confidence.

In the first quarter of 2026, the dollar's share of global foreign exchange reserves fell 2.3 points, a quarter of the previous decade's entire decline in ninety days. Non-dollar transactions gained ground quickly on the SWIFT payment network, rising from 18% to 31% in the Middle East and from 35% to 42% in Asia.

And for the first time since 1996, the world's central banks now hold more gold than they hold US Treasury securities.

The big picture is that foreign governments are setting up for a new monetary order, one in which physical reserves matter more than paper promises from Washington.

So governments are securing as many physical reserves as they can.

It’s not just gold, either. Energy, fertilizer, industrial metals, and shipping are all getting the same treatment as gold: repatriated, stockpiled, or rerouted to suppliers inside friendly borders.

Countries across the Western Hemisphere are rebuilding domestic production for fuel, uranium, copper, and food, because they can no longer count on the old, postwar order to deliver the goods on schedule at a price they can live with.

We can already see the early signs– the same loss of trust that has driven central banks to buy so much gold is starting to lead to bulk buying of other real assets… which means that the prices of these strategic resources will likely rocket higher.

This means that the companies which produce those real assets (as well as their shareholders) are likely set to make a LOT of money in the future.

With assets like gold or silver, you could buy the metals outright. But today that means paying near all-time highs.

In our analysis it’s a much better deal to own the companies that produce them. As real asset prices rise, margins expand and profits multiply.

For example, gold has roughly tripled in three years. But one mining company we featured in Strategic Assets (Schiff Sovereign's monthly investment research service), is up 5x in the same period. And a silver miner we featured went up nearly 10x.

Energy, industrial metals, and shipping can offer the same leverage.

We look for profitable, well-managed real asset businesses with clean balance sheets and clear catalysts, trading at a low multiple of free cash flow, positioned to benefit from the exact shift central banks are already executing.

None of this makes us permabulls on gold, silver, or anything else. The environment is too volatile for certainty, and our edge is not in calling the next move. Our edge is applying the same disciplined criteria to very well run businesses and adjusting when the facts shift.

We chase returns, not attachment to any particular company or commodity.

And our approach has worked. Out of 20+ companies we have featured, one we sold at 10x and another at 6x, several current positions are up 2-4x, and only three are in the red. However we think those three have substantial upside from here.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Argentina Got This Warning Before Its Collapse. America Just Got It Last Week.

Argentina Got This Warning Before Its Collapse. America Just Got It Last Week.

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 20, 2026

In early December 2001, ‘normal’ life very suddenly ceased to exist in Argentina— anything that remotely resembled a functional society came to an abrupt end. And that is by no means an exaggeration. The banking system collapsed. Financial transactions ground to a halt. Desperate people looted supermarkets for food, and then grocery shelves emptied. Energy ran short. Riots broke out in the streets, and police were shooting citizens in the face.

Argentina Got This Warning Before Its Collapse. America Just Got It Last Week.

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 20, 2026

In early December 2001, ‘normal’ life very suddenly ceased to exist in Argentina— anything that remotely resembled a functional society came to an abrupt end. And that is by no means an exaggeration. The banking system collapsed. Financial transactions ground to a halt. Desperate people looted supermarkets for food, and then grocery shelves emptied. Energy ran short. Riots broke out in the streets, and police were shooting citizens in the face.

The crisis raged so much that the President of Argentina fled the country by helicopter. Five presidents rotated through the office in two weeks. Then the country defaulted on $93 billion in sovereign debt— the largest default in history at the time.

Argentina was left in such a deep constitutional crisis that it didn't even have the money or the legal framework to hold an immediate election.

This wasn’t exactly a surprise.

For years leading up to the crisis, Argentina had been struggling. The country was in the midst of a major economic depression. Unemployment was high. GDP was shrinking. Inflation was increasing. Crime was rising.

And yet, even with all of that negativity, life was at least in the ballpark of normal.

Basic services still functioned. Grocery stores had food. Banks were open and had money. And, even though unemployment was high, the vast majority of people still had jobs.

But it all collapsed in the span of three weeks. Poof. All because of too much debt.

To its credit, one of the groups that saw this coming was the IMF, which had warned the Argentine government multiple times about a looming crisis.

Even in early 2001, the same year as the crisis, IMF reports flagged Argentina’s soaring debt-to-GDP ratio, citing its "sharp deterioration in the public finances," and deficits running well above the targets Buenos Aires had agreed to.

Well, the United States just received the same warning from the IMF last week. Even the language in the report is eerily similar.

In its 2026 Article IV consultation on the United States of America, the IMF warned that America's “persistently high fiscal deficits [and] the continued rise in debt‑GDP ratio” creates a "growing financial stability tail risk" for both the US and the global economy.

They stressed "the pressing need to address the US's longstanding fiscal imbalances through a frontloaded fiscal adjustment."

That last part means that Congress must make critical spending cuts NOW. Not later. Time is running out.

The IMF cites US government debt reaching 123.9% of GDP and deficits equal to 7.5% of GDP. More importantly, they point out that the US government has no credible plan to reduce them.

To be fair, America is not Argentina, and the US boasts major advantages— including one of the world's most innovative economies and the deepest capital markets on earth.

But it’s nearly impossible to argue that the US isn’t heading towards a major debt crisis. The rest of the world has already figured this out— and the data prove it.

For example, in the first quarter of 2026, the share of global foreign exchange reserves denominated in US dollars fell by 2.3 percentage points, down to 56.1%.

That’s an unprecedented move in global reserves. To put that quarterly decline in perspective, the US dollar's reserve share declined by roughly 10 percentage points over the previous decade...

... which means that roughly a quarter of that 10-year decline happened in the past 90 days! That’s evidence of a significant acceleration in the world’s loss of confidence in America.

The SWIFT international payments network tells the same story. The dollar's share of international payments dropped substantially in Q1. In the Middle East, for instance, non-dollar transactions jumped from 18% to 31% in three months. In Asia, from 35% to 42%.

Another data point: the world's central banks now hold more gold than US Treasury securities for the first time since 1996.

This comes as no surprise to our readers. We've been writing about this for the past 17 years.

Back in 2009, we were laughed at for suggesting that the United States could one day face a debt crisis. Today even the IMF is saying it.

We often cite that line from Hemingway's The Sun Also Rises — "How did you go bankrupt?" "Two ways. Gradually, then suddenly." The de-dollarization data suggests we're entering the "suddenly" phase.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

P.S. We've been warning about the US fiscal trajectory for years, long before it was fashionable. For most of that time, these concerns were dismissed as alarmist.

Now it's a mainstream view. And the rest of the world is repositioning.

The sensible course of action is to do the same. International diversification, real assets, a second residency, an offshore bank account — these aren't doomsday preparations. They're rational responses to a fiscal trajectory that is a risk to the global economy.

That is exactly what we cover each month in Plan B Confidential — specific, legal, practical steps to diversify across borders, from second residencies and offshore banking to tax optimization and real asset strategies that make sense regardless of how this plays out.

https://www.schiffsovereign.com/trends/argentina-got-this-warning-before-its-collapse-america-just-got-it-last-week-155037/?inf_contact_key=0e78a2143153df024cd70fe991ce4b0a0610b17be1dd28ffc304ba09276be34a

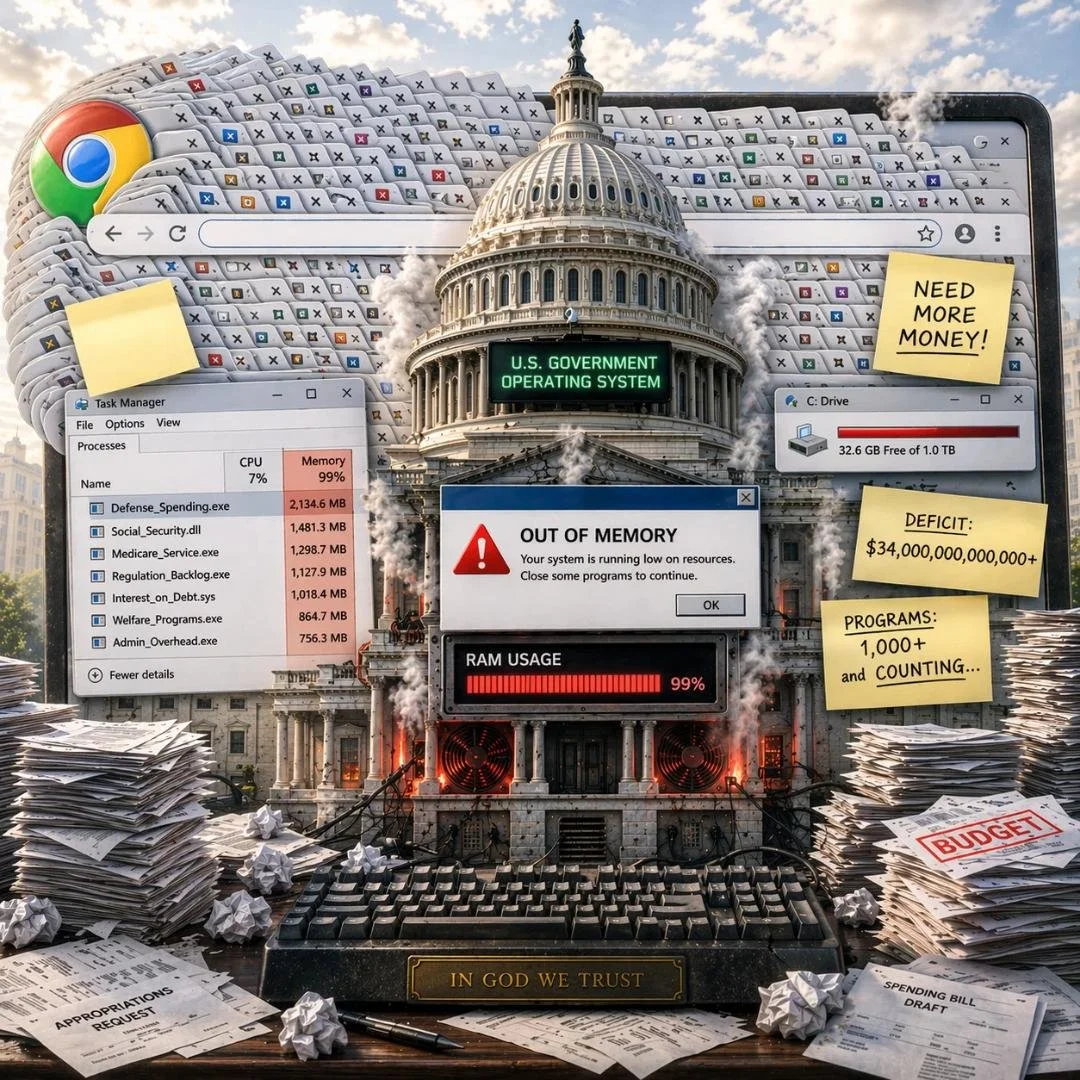

Why the Government Runs Like a Bloated Chrome Tab

Why the Government Runs Like a Bloated Chrome Tab

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 17, 2026

I had a Commodore 64 “computer” when I was a kid. I know I’m dating myself with that reference... but I’m telling you— back in the 80s, a Commodore was pretty hot stuff. It was basically an antique typewriter that you plugged into a television (sort of like a Nintendo or other gaming console). And they called it a Commodore “64” because it had a whopping 64 kilobytes of RAM.

"Kilobytes" is not a typo. For context, most mobile phones today have 8 gigabytes of RAM, and a gigabyte is roughly 1 million times a kilobyte.

Why the Government Runs Like a Bloated Chrome Tab

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 17, 2026

I had a Commodore 64 “computer” when I was a kid. I know I’m dating myself with that reference... but I’m telling you— back in the 80s, a Commodore was pretty hot stuff. It was basically an antique typewriter that you plugged into a television (sort of like a Nintendo or other gaming console). And they called it a Commodore “64” because it had a whopping 64 kilobytes of RAM.

"Kilobytes" is not a typo. For context, most mobile phones today have 8 gigabytes of RAM, and a gigabyte is roughly 1 million times a kilobyte.

****************************

pic

The average email today (without attachments) is nearly 100 kilobytes, i.e. 50% more than the entire memory of my Commodore. Yet, back in the 80s, software developers were able to do miraculous things with that tiny amount of memory.

64 kilobytes was somehow enough to play games like Pitfall and Impossible Mission, bang out a school report on a dot-matrix printer, and all sorts of other things.

And it wasn’t just Commodore— Nintendo and Sega put out hundreds of titles on consoles that had comparably tiny amounts of memory.

In order to make all of this magic happen, programmers had to be absolutely ruthless about every single line of code. Every byte mattered. There was zero bloat. Zero inefficiency.

And software teams routinely fought with each other about what features would be in a game, versus what features would be thrown out— because there simply wasn’t enough memory to include what everyone wanted.

***********************************

In short, the software industry had to live within its means. Yet despite those severe memory limitations, they put out timeless classics. It was a Golden Age for software development.

But then something happened. Technological and manufacturing breakthroughs made memory abundant... and cheap. Whereas 64 kilobytes of memory was considered a luxury in the 80s, soon megabytes of RAM... and then gigabytes of RAM, became readily available.

Memory eventually became so abundant that it felt practically infinite. No one had to make any tough decisions to optimize their code for RAM limitations... because there was always more memory available.

As a result, bloat eventually crept in. Here are a few examples.

Literally right now as I write this, I have a number of tabs open in my browser (I use Brave, by the way). ProtonMail takes up 409 megabytes of RAM... for a single tab. And a web-based PowerPoint presentation in my browser takes up 957 megabytes of RAM!

And don’t get me started on Windows.

Microsoft has been rolling out a ‘feature’ to “pre-load” data in its File Explorer application that consumes 67.4 megabytes of RAM. That’s more than 1,000x the memory requirement as my Commodore 64 had... for the sole purpose of being able to look at files and folders on your computer.

The level of bloat and memory waste is absurd (and also why I use Linux).

There’s hardly anyone in the industry today who remembers the bygone days of having to make ruthless decisions over every line of code; rather, the software industry today is accustomed to being able to publish bloated code... because memory has been so abundant for so long.

Unfortunately conditions have now dramatically changed.

Thanks in large part to surging AI demand, there is now a global memory shortage. RAM supply is scarce and has skyrocketed in price.

The industry, quite predictably, is fretting over the supply side, complaining that memory manufacturers need to build new factories and produce more RAM.

Very few prominent voices in software are saying, “Gee guys, maybe we should be more efficient in our code and use less RAM. Maybe it shouldn’t take 67 megabytes to look at our system files... Or 400+ megabytes for a single browser tab.”

In other words, there’s very little push to be more efficient and live within their means.

If you’re starting to see where I’m going, this story should sound familiar... because it’s very similar to how the government spends our money.

*********************************

Once upon a time in America, Congress fought passionately over every dollar. They knew they had to live within their means, and every budget item mattered. Politicians debated passionately about which programs stayed and which had to go.

But that was the past. America has been the world’s superpower, and the US dollar the world’s reserve currency, for eight decades.

Consequently, the US government has been able to run massive deficits and rack up a gargantuan national debt with impunity, leading politicians to believe that America’s financial resources are infinite.

Today there’s no one in government who remembers the days of responsible spending. That’s why there’s so much bloat and why deficits are so high.

But, just like the memory market, a sudden scarcity is emerging. Foreign creditors— who used to provide ample funds to the Treasury market— are starting to invest their capital elsewhere.

We can see this impact with interest rates, which are now hovering near multi-decade highs... as well as gold prices, which remain near all-time highs.

Faced with a sudden scarcity of financial resources— and the shocking realization that government spending cannot be infinite— Congress is choosing the predictable route.

Rather than look to themselves to become more efficient, to make objective and ruthless decisions about what programs stay and what programs go, to live within their means... they are instead demanding more resources.

Of course they always start with calls to “tax the rich”. But these taxes invariably trickle down to the middle class; just ask anyone who had to submit an AMT return this week.

But the point here isn’t to argue whether Jeff Bezos should or shouldn’t pay more tax. The point is that Congress’s approach is entirely wrong.

As we discussed yesterday, they fail to understand a very simple point: higher tax rates don’t generate higher overall tax revenue. Higher tax revenue comes from a booming economy.

So they should instead invest their energy into ensuring maximum productivity... which ultimately means fewer regulations, and in general staying out of the way.

It’s also insane that they are specifically refusing to cut spending. Despite hundreds of billions worth of documented fraud, they do nothing about it. They’ve also pledged to NOT reform Social Security and Medicare, i.e. the single biggest budget items in government.

It’s the exact opposite of what they should be doing. They still don’t have the right mentality to solve America’s #1 problem... and it’s why having a Plan B makes so much sense.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

There Is No "Fair Share" — There Is Only “More”

There Is No "Fair Share" — There Is Only “More”

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 16, 2026

In April 1971, Keith Richards loaded his family and his Bentley onto a cross-Channel ferry and drove south until he hit the Mediterranean. He rented a 19th-century villa called Nellcôte on a hillside above Villefranche-sur-Mer, and converted the basement into a recording studio.

There Is No "Fair Share" — There Is Only “More”

Notes From the Field By James Hickman (Simon Black / Sovereign Man) April 16, 2026

In April 1971, Keith Richards loaded his family and his Bentley onto a cross-Channel ferry and drove south until he hit the Mediterranean. He rented a 19th-century villa called Nellcôte on a hillside above Villefranche-sur-Mer, and converted the basement into a recording studio.

Over the following year the rest of the Rolling Stones rotated through the house and nearby properties to record the double album that became Exile on Main St., while staying deliberately out of reach of the British tax authorities.

The top marginal income tax rate in Britain at the time was 75%, and a surcharge on the highest earners pushed the effective rate on the wealthiest past 90%.

Three years later, under Denis Healey's 1974 budget, the top rate on earned income would climb to 83% and the rate on investment income would reach 98%.

Britain would spend the rest of the decade watching capital flee and begging the IMF for emergency loans.

David Bowie, Rod Stewart, Michael Caine, Sean Connery, and a long line of less famous wealthy Britons eventually ran the same arithmetic as the Stones and reached a similar conclusion. Capital left the country in every form it could fit into, including bonds, businesses, luxury cars, and rock stars.

But politicians never learn.

Senator Cory Booker of New Jersey has backed legislation that would push the top federal income-tax rate to 43%.

Senator Chris Van Hollen of Maryland is pushing a version that lands at 49%.

Both men describe it, as they always do, as wealthy Americans finally paying their "fair share."

What exact percent is their fair share? Are we to believe they will be satisfied at 43% or 49%?

As always, that phrase is deliberately left undefined.

Never-mind that the top 1% of filers already paid 40.4% of all federal income taxes in 2022 while the bottom 50% paid roughly 3%.

They are also conveniently ignorant of the fact that raising the top marginal rate doesn’t actually raise revenue at all.

Since the end of the Second World War, U.S. federal tax revenue has averaged around 17% to 18% of GDP, dipping toward 15% in deep recessions and climbing near 20% in booms. The swings track the business cycle, not tax policy.

The top marginal rate, over that same stretch, has been all over the map: 91% under Eisenhower, 28% under Reagan by 1988, 39.6% under Clinton, 37% today. Yet regardless of whether tax rates were 91% or 37%, the IRS always collects around 17% of GDP.

The conclusion is obvious: if the government wants to collect more tax revenue, they should focus on setting the right conditions for an economic boom. In short, make the pie bigger for EVERYONE, and hence the government’s slice will grow as well.

Making the pie bigger isn’t that hard, either. America’s private economy is legendary. All Congress has to do is get out of the way. Attempt to run a balanced budget. Restore credibility. Make it easier for businesses and individuals to be productive. REMOVE idiotic laws instead of creating new ones.

But they’re not interested in any of those things.

Congress has documented evidence of hundreds of billions of dollars in fraud. Yet they do nothing. They have also pledged to do nothing about Social Security— which is set to run out of money in six years.

The regulatory code in the Land of the Free already runs over 188,000 pages. Yet they expand it every session.

This is the opposite of what they should be doing. And instead of figuring out how to live within their means, they just demand more resources... even though it never works.

Britain tried its 98% tax experiment in the 1970s and spent a decade regretting it.

Ironically the current Labour government has forgotten that painful lesson; they recently abolished the 110-year-old "non-dom" regime, and more than 10,000 millionaires have already left the country.

In the United States, Elizabeth Warren's Ultra-Millionaire Tax proposal does not just impose a wealth tax. It bundles her wealth tax with an additional 40% exit tax on anyone who renounces US citizenship.

You do not create a 40% tollbooth at the border unless you fully expect people to try to walk through it.

These are not serious ideas to grow an economy. Rather, they are insidious policies designed to trap people in a system which steals their prosperity. That is why a Plan B makes so much sense.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

The $13,000 Apartments the Government Won't Let You Buy

The $13,000 Apartments the Government Won't Let You Buy

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 14, 2026

On May 20, 1862, Abraham Lincoln signed the Homestead Act into law, and it essentially said: here's 160 acres of land. It's yours. For free. All you have to do is live on it and improve it. And between 1862 and 1934, the federal government distributed 270 million acres under the program — roughly 10% of all the land in the United States.

Even as far back as the American Revolution, the Founding Fathers understood that property ownership made people more engaged, more productive citizens. Ownership meant that you had a vested financial interest in your community... and your country.

The $13,000 Apartments the Government Won't Let You Buy

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 14, 2026

On May 20, 1862, Abraham Lincoln signed the Homestead Act into law, and it essentially said: here's 160 acres of land. It's yours. For free. All you have to do is live on it and improve it. And between 1862 and 1934, the federal government distributed 270 million acres under the program — roughly 10% of all the land in the United States.

Even as far back as the American Revolution, the Founding Fathers understood that property ownership made people more engaged, more productive citizens. Ownership meant that you had a vested financial interest in your community... and your country.

Over time, that idea fused with the concept of "the American Dream". And for decades that dream was a reality for millions of people.

After World War II, for example, America underwent a massive construction boom. Between postwar prosperity, the GI Bill, and the arrival of the modern 30-year fixed mortgage, home ownership surged from about 44% in 1940 to 62% by 1960.

More importantly, housing was affordable.

In 1950, median family income was about $3,000, yet the median home cost roughly $7,350. That’s just ~2.5 times median household income. Plus, with prevailing mortgage rates back then 4.5%, the monthly payments were trivial.

Because of that, families across America could easily make ends meet on a single income.

Today the median home sells for about $412,000. Median household income is roughly $83,700. That puts housing at 5x household income— double what it was in the 1950s.

More importantly, at today's mortgage rate of roughly 6.4%, the monthly payment on a median home (assuming a 20% down payment) consumes roughly 30% of household income.

The down payment is also so high these days that buying a home is nearly impossible, especially for young people or low-income workers. Even in dual-income households, homeownership is increasingly out of reach.

As we discussed on Friday, America’s housing problems go far beyond the ‘greedy’ Wall Street investors that are getting most of the blame for rising home prices.

Construction materials cost 40% more than they did five years ago, courtesy of the Federal Reserve printing trillions during the pandemic and igniting inflation.

Plus the regulatory permitting maze adds enormous costs. In Fremont, California, development fees alone run $157,000 per home before a single nail is hammered. And that doesn’t even include additional permitting costs and utility connection fees.

The government used to give away 160 acres for free. Now local governments charge six figures for permission to build.

Go figure that California, with its endless lip service about affordable housing, is also the epicenter of American homelessness.

But it turns out there's a ready-made solution staring policymakers in the face.

The office property market is a complete bloodbath right now. Between the sluggish economy, AI reducing demand for workers, and the lingering work-from-home paradigm, the prices of office properties across the country have tanked.

More than 200 distressed office buildings changed hands across the country in 2025, with average sale prices down 37% from 2019. In Manhattan, a 920,000-square-foot tower sold for $8.5 million, down from $332.5 million. That’s a 97% decline!

Then there’s 401 South State Street in Chicago, a 485,000-square-foot office building that sold last October for $4.2 million, down from $68.1 million in 2016. That’s less than $9 per square foot.

Housing in Chicago isn’t cheap. So just imagine you’re young, fresh out of college, and staring at the prospect of paying $1,200 per month to live in a cramped apartment with three roommates.

Instead, you could pay about $13,000 for 1,500 square feet worth of space in the 401 South State Street office building that would be yours to own.

Yes, duh, it’s an office building. So it wouldn’t have the conveniences of a traditional home— like private bathrooms and kitchens. But for $13 grand?!!? Who cares. You'd have your own private space, a roof over your head, and a door that locks.

Frankly, that's not so different from military barracks and university dorms. Americans manage just fine with communal facilities when the price is right.

That's the beauty of capitalism. Such living accommodations aren’t for everyone. But at a low enough price, a LOT of people would happily trade convenience for affordability. Shower at the gym. Eat at the fast-casual spot around the corner. Live with walking distance to work downtown.

Most 20-somethings might think that’s pretty cool— especially compared to the alternative of paying out the nose for rent and never managing to save enough money to buy a house.

Same logic for a family of six crammed into a two-bedroom public housing unit in decrepit conditions; they could have a few thousand square feet to themselves.

Here’s another scenario. Let’s say a family in Topeka, Kansas locked in a 2% mortgage during the pandemic. Dad got laid off and can't find another job locally. But they don’t want to sell the house to move across country, uproot the kids, and buy a new house somewhere else at a 6% rate. So they're stuck.

Instead, Dad buys 1,000 square feet in one of these bankrupt office buildings for less than $10k. His family stays home, he commutes to his new job in a new city, and flies home on the weekends to see his kids. They make it work... which they wouldn’t be able to afford with hotels or an AirBnb.

This would be a genuine ‘starter home’— a place where someone could actually save money and build toward a proper mortgage, instead of hemorrhaging rent to Blackrock every month while still falling behind.

But the government won't allow it.

Zoning codes, building regulations, occupancy requirements— a labyrinth of rules that forbid you from such options.

Let grown adults decide for themselves. That's how capitalism is supposed to work.

Nobody would pay $400,000 for a unit with no bathroom. But $13,000? For a lot of Americans, that's not a sacrifice— it's an opportunity.

The same politicians who claim to care about the poor, the homeless, and young people priced out of the American Dream have the obvious solution sitting right in front of them.

But they won't take it, because that would mean getting out of the way.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

PS — Another way to opt out of America's housing affordability disaster is to look elsewhere.

There are plenty of countries where you can buy a beautiful home in a major city for a fraction of what a starter unit costs in the US, and several of those purchases also qualify you for residency or eventual citizenship. So you're not just buying a home, you're buying optionality. We cover the best programs, exact thresholds, and on-the-ground intelligence in Plan B Confidential.

Two Weeks to Stop the Spread of War

Two Weeks to Stop the Spread of War

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 8, 2026

On August 15, 1945, after two of their cities had been obliterated by the world's first nuclear weapons, the people of Japan heard the voice of their young Emperor for the first time ever.

Hirohito went on what was a relatively new communications medium at the time—the radio— and gave one of the most bizarre speeches in all of human history, in which he told his subjects that "the war situation has developed not necessarily to Japan's advantage."

Two Weeks to Stop the Spread of War

Notes From the Field By James Hickman (Simon Black/Sovereign Man) April 8, 2026

On August 15, 1945, after two of their cities had been obliterated by the world's first nuclear weapons, the people of Japan heard the voice of their young Emperor for the first time ever.

Hirohito went on what was a relatively new communications medium at the time—the radio— and gave one of the most bizarre speeches in all of human history, in which he told his subjects that "the war situation has developed not necessarily to Japan's advantage."

Talk about an understatement.

It's one of the more famous examples in a long list throughout history of speeches that have ended conflicts, where leaders paint whatever picture they want.

Perhaps even more famously, Richard Nixon promised "peace with honor" in Vietnam on the campaign trail in 1968.

It was one of the most brilliant political statements of its era, because everyone heard what they wanted to hear. Those who wanted an end to the war heard "peace." The war hawks heard "honor." Everyone got what they wanted out of it.

But ultimately there was neither peace nor honor. The war dragged on for seven more years, resulting in a humiliating withdrawal from Saigon in April 1975, complete with desperate helicopter evacuations from the US Embassy rooftop.

This is the sort of stuff that peace deals and conflict resolutions are made of— situations where you can talk out of both sides of your mouth, and both sides of the conflict can declare victory.

And if both sides can claim victory, that's actually a good thing. Because the only other way to end a war is to have the other side so utterly demolished that they have no choice but to accept defeat.

The alternative is to give both sides an out.

That's what's happening with Iran.

It's a strange situation from a military and strategic perspective given that Iran has been objectively obliterated; major infrastructure is demolished, key leadership was assassinated, the military is weakened, the government is vulnerable— and yet Iran actually thinks they are winning. Or at least they act like it.

It reminds me of when Charlie Sheen was on a three-day cocaine binge giving live interviews and talking about "winning." That's Iran right now.

The reason is because the American media is so deranged, so pro-Iran and anti-Trump, that they have managed to convince the Iranians that they are much stronger than they actually are.

But at this point the political realities have started surfacing in the US. The administration is worried about high gas prices and the midterms, and there’s a lot of pressure to end the conflict.

Now there’s an arrangement where both sides can declare victory. The US can say they accomplished their objectives — dismantled Iran's military and defense capabilities, degraded their nuclear program, eliminated key leadership, and dismantled their ability to fund and spread terror.

And the Iranians can say they stood up to the ‘evil empire’ and forced the Americans to walk away.

That is essentially what both sides are saying right now. And while the full implications remain to be seen, this is where the proverbial rubber meets the road.

We've been saying since this war started that it could end up being a very big deal for the fate of the United States... so what happens during negotiations over the next few weeks is crucial.

On one hand, there is a possibility they could strike a deal to lift sanctions against Iran and allow Iranian oil to be sold on the global market— as long as it's priced in US dollars.

Between Iran and Venezuela, that could create a massive financial incentive for the whole world to continue to hold US dollars, and thus to buy US government bonds.

But it could just as easily go the other way if the Iranians continue to think they are in a position of strength and that they have the advantage.

One thing we can be pretty sure about is that there probably won't be a resolution in two weeks.

I couldn't help but think of the infamous "two weeks to stop the spread" when COVID first emerged. That was an unrealistic timetable then, and two weeks is an unrealistic timetable now.

International negotiations are extremely difficult, and the tried and true tactic of rogue-nation geopolitics is to let negotiations drag on.

The Soviets perfected this approach. Their strategy was always to exhaust the negotiation partner. Westerners tend to like quick and speedy deals, but rogue nations in general tend to use that impatience to their advantage. So it's hard to believe in the two-week time frame.

But the clock has certainly started, however long it takes. And by the end we should have a very good sense for what this means for America.

The consequences could be massive— for inflation, for the dollar, for bond markets, for the trajectory of the entire US economy.

This could still be a deal that helps prop up the dollar and US government bonds for years, if not decades, to come. But if that doesn't happen, the best-case scenario is probably a stalemate where both sides walk away, flip the switch, turn off the war, almost pretend it never happened. And hopefully the world just ignores it and gives America a pass.

Time will tell. But probably not in the next two weeks.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC