Can an Iraqi Dinar RV Reach $3.00+ Matching Kuwait? Here’s What You Need to Know : Awake-In-3D

Can an Iraqi Dinar RV Reach $3.00+ Matching Kuwait? Here’s What You Need to Know

On November 2, 2023 By Awake-In-3D

In RV/GCR

The three strongest currencies in the world are held by Iraq’s neighboring nations – Kuwait, Bahrain and Oman. How does Iraq compare economically and politically against these powerhouse currencies, and can the Iraqi Dinar RV support such valuations?

This is Section 3 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

This section represents the culmination of the 3-section article series which set out to analyze and explain the important factors surrounding a potential revaluation (RV) of the Iraqi Dinar (IQD)

Can an Iraqi Dinar RV Reach $3.00+ Matching Kuwait? Here’s What You Need to Know

On November 2, 2023 By Awake-In-3D

In RV/GCR

The three strongest currencies in the world are held by Iraq’s neighboring nations – Kuwait, Bahrain and Oman. How does Iraq compare economically and politically against these powerhouse currencies, and can the Iraqi Dinar RV support such valuations?

This is Section 3 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

This section represents the culmination of the 3-section article series which set out to analyze and explain the important factors surrounding a potential revaluation (RV) of the Iraqi Dinar (IQD)

Section 1, Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events provided a detailed, historical context surrounding the Iraqi Dinar, This included its evolution, the impact of wars, the role of economic sanctions, and the popular reasons for speculations regarding an Iraqi Dinar revaluation.

Section 2, A Sky High Iraqi Dinar RV Boils Down to This identified and explained every key economic and political stability indicator that directly influences and supports a strong and stable currency exchange rate.

Building upon the knowledge acquired regarding key economic indicators in Section 2, we now direct our focus toward a comparison of Iraq’s neighboring countries, distinguished by their robust and stable currencies.

This analysis centers on the examination of the key economic indicators and political stability indices that underpin countries with very strong (high) exchange rate in U.S. Dollar terms. Specifically, the nations of Kuwait, Bahrain, and Oman.

By comparing these nations with Iraq, we will gain valuable insights into the practical determinants that may influence the potential revaluation of the Iraqi Dinar.

3.1 Iraq’s Regional Neighbors with Strong Currency Exchange Rates

Let’s start by establishing a baseline of currency exchange rates within the region.

Kuwait (KWD): 1 KWD = $3.23

Bahrain (BHD): 1 BHD = $2.65

Oman (OMR): 1 OMR = $2.60

Iraq (IQD): 1 IQD = $0.00076 (1310 IQD per 1 USD)

3.2 Key Regional Economic Indicators to Support an Iraqi Dinar RV

The relevance of this comparative analysis lies in the examination of fundamental economic indicators which serve as the bedrock of currency dynamics.

These indicators allow us to assess the currency dynamics and economic environments within Iraq and its regional counterparts.

Here are the key economic indicators we shall scrutinize and compare for each country:

National Gross Domestic Product (GDP)

Economic Growth (GDP Growth Rate)

Core Inflation Rate

Current Account Balance

Public Debt (as a Percentage of GDP)

Foreign Exchange Reserves

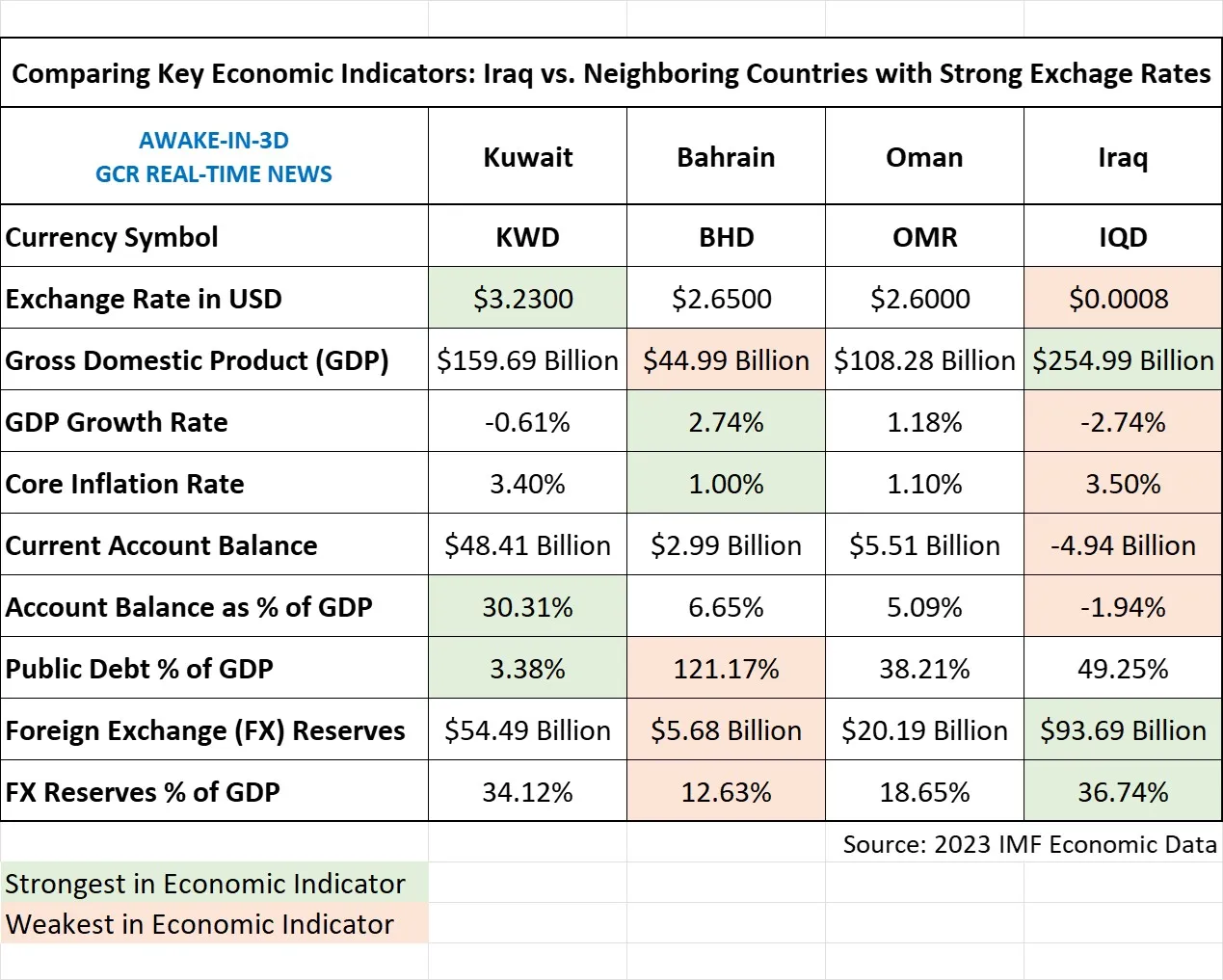

The following chart summarizes a direct comparison of these key economic indicators between Iraq, Kuwait, Bahrain and Oman based on the latest 2023 economic data.

Source Data: 2023 IMF Economic Research

3.2.1 What this Economic Comparison Indicates Relative to an Iraqi Dinar RV

National Gross Domestic Product (GDP):

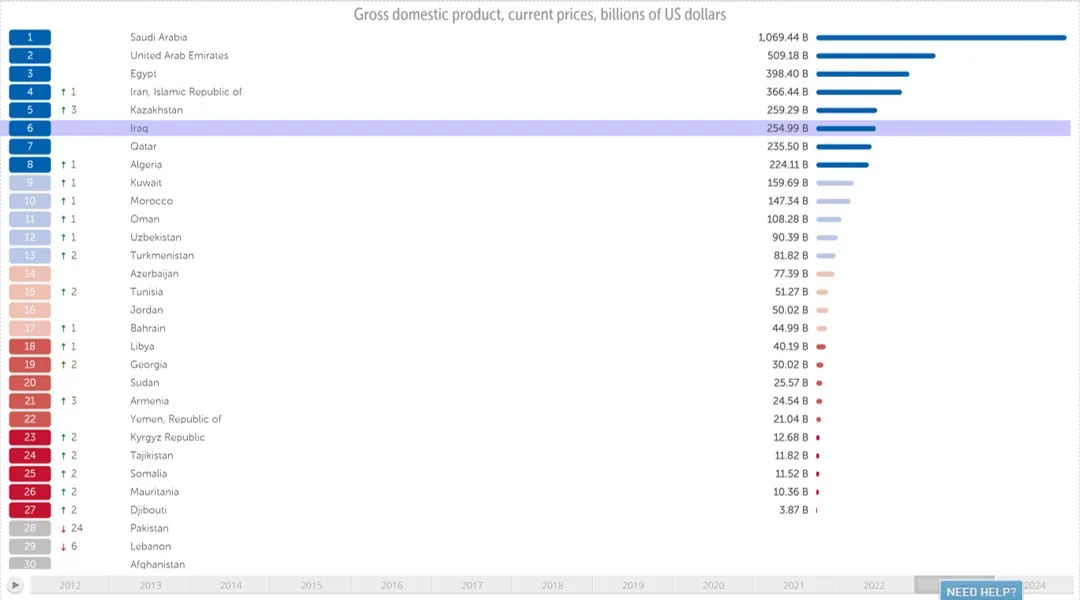

Iraq has the highest GDP among the mentioned countries at $254.99 billion, indicating the largest economic size in the region.

While Iraq’s GDP is relatively large, its economy is heavily dependent on its competitive strength in oil exports and processing efficiency (production cost per barrel of oil). Given Iraq’s ongoing need for infrastructure efficiency and capacity upgrades, its competitive position is weaker than that of neighboring nations .

Moreover, Iraq’s economy suffers from a broader set of structural issues, including elevated levels of financial and political corruption, which prevents the confidence necessary for significant foreign capital investment.

GDP OF MIDDLE EASTERN REGION. Source: IMF

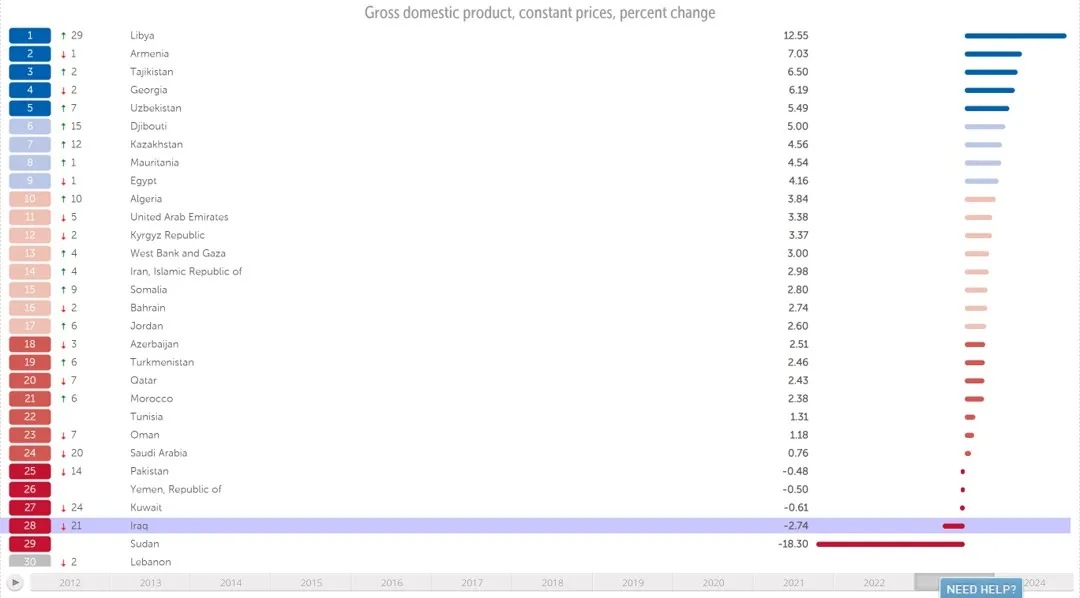

Economic Growth (GDP Growth Rate):

Bahrain leads in economic growth with a GDP growth rate of 2.74%. This positive growth rate signifies a thriving economy.

Oman’s growth rate is 1.18%, indicating a moderately growing economy.

Kuwait has a negative growth rate of -0.61%, suggesting a contraction in its economy.

Iraq’s GDP growth rate is -2.74%, showing a significant economic output decline, which can likely be attributed to ongoing security issues and political instability.

GDP GROWTH RATE OF MIDDLE EASTERN REGION. Source: IMF

Inflation Rates:

Bahrain has a relatively low inflation rate of 1.0%, indicating price stability.

Oman’s inflation rate is also low at 1.1%, contributing to stable purchasing power.

Kuwait’s inflation rate is 3.4%, relatively high compared to its neighbors, which may affect consumer affordability.

Iraq, with an inflation rate of 3.5%, experiences even higher price increases, impacting the living standards of its citizens, which is reflected by Iraq’s contracting GDP above.

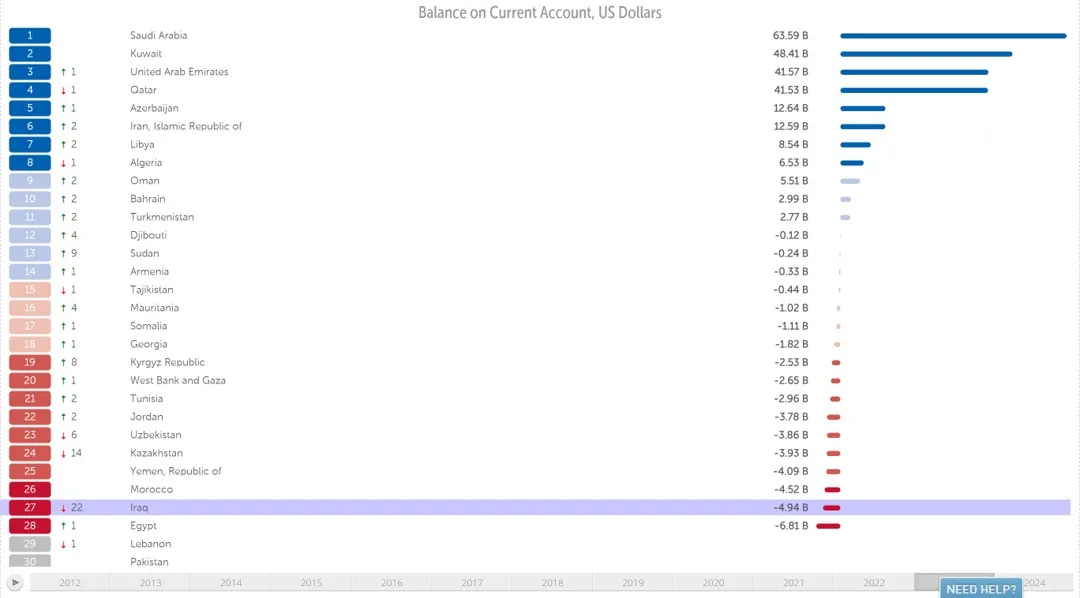

Current Account Balance:

Kuwait maintains a significant surplus with a current account balance of $48.41 billion, reflecting strong international trade.

Oman has a surplus of $5.51 billion, indicating a healthy trade balance.

Bahrain’s surplus is $2.99 billion, showcasing its economic stability.

Iraq, however, has a deficit of -$4.94 billion, implying that it imports more than it exports, which can strain its foreign exchange reserves.

CURRENT TRADE ACCOUNT BALANCE OF MIDDLE EASTERN REGION. Source: IMF

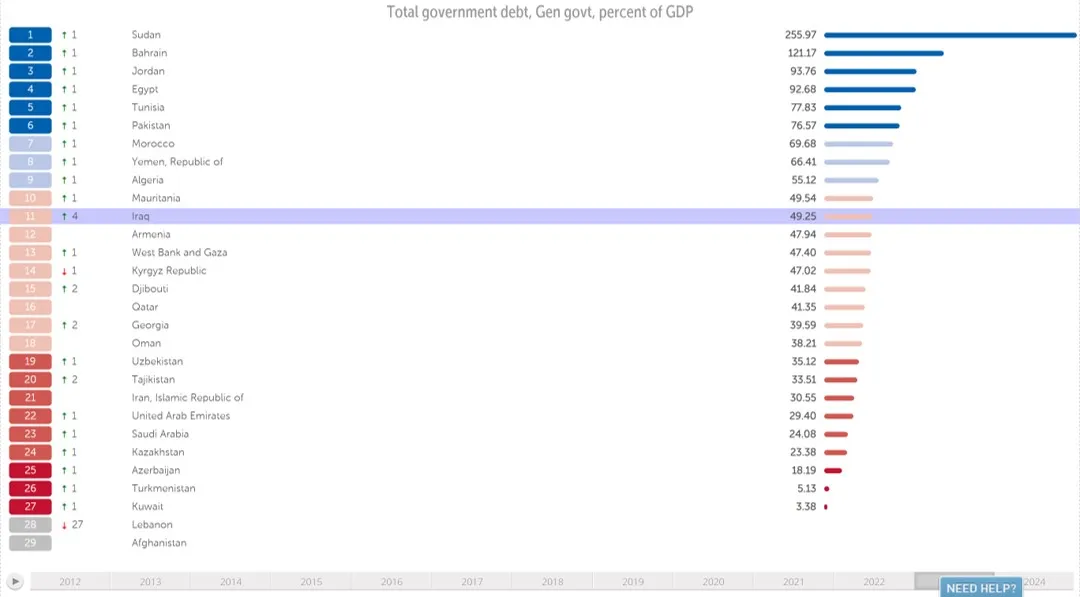

Public Debt (as a Percentage of GDP):

Kuwait’s public debt is relatively low at 3.38% of its GDP, reflecting fiscal responsibility.

Oman’s public debt is 38.21% of its GDP, suggesting a higher debt burden.

Bahrain’s public debt is notably high at 121.17% of GDP, indicating significant fiscal challenges.

Iraq’s public debt is 49.25% of its GDP, which is relatively high and indicates a substantial debt burden.

PUBLIC DEBT OF MIDDLE EASTERN REGION. Source: IMF

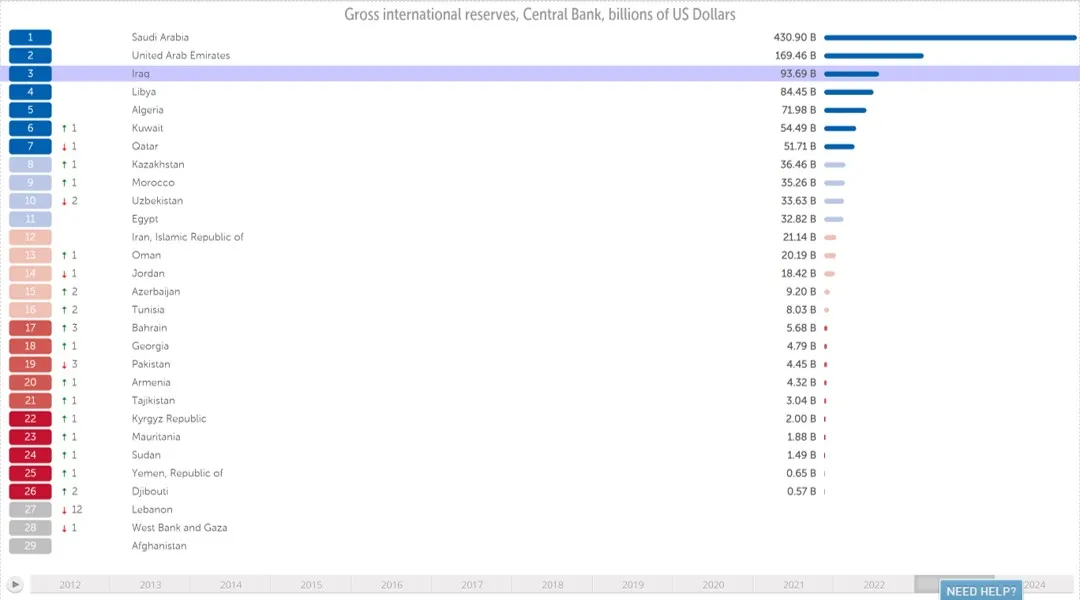

Foreign Exchange Reserves:

Kuwait holds foreign exchange reserves of $54.49 billion, which is substantial and provides stability to its currency.

Oman’s reserves are $20.19 billion, providing a buffer against external economic shocks.

Bahrain’s reserves are $5.68 billion, which, while lower than its neighbors, still contributes to currency stability.

Iraq’s foreign exchange reserves are $93.69 billion at approximately 37% relative to GDP – stronger than any of its neighbors. This would serve well in maintaining a strong currency peg to the U.S. dollar (or a basket of currencies including the USD).

FOREIGN EXCHANGE (FX) OF MIDDLE EASTERN REGION. Source: IMF

The Bottom Line

Iraq faces substantial economic challenges compared to its neighbors with stronger currencies being the weakest in 5 out of 8 key indicators.

These challenges include a negative GDP, economic contraction, higher inflation rates, a trade deficit, and a relatively high public debt burden. Consequently, Iraq’s ability to support an equally high exchange rate as its neighbors is limited by these economic constraints.

However, the weakness around Iraq’s key economic indicators is not so severe as to prevent a significant currency RV in the $2.00-$2.75 range.

Iraq appears to have the basic economic strength to support a currency peg similar to Kuwait, Bahrain and Oman.

So what’s holding Iraq back from Revaluing the IQD with a new currency peg? Perhaps the political stability index can provide an answer.

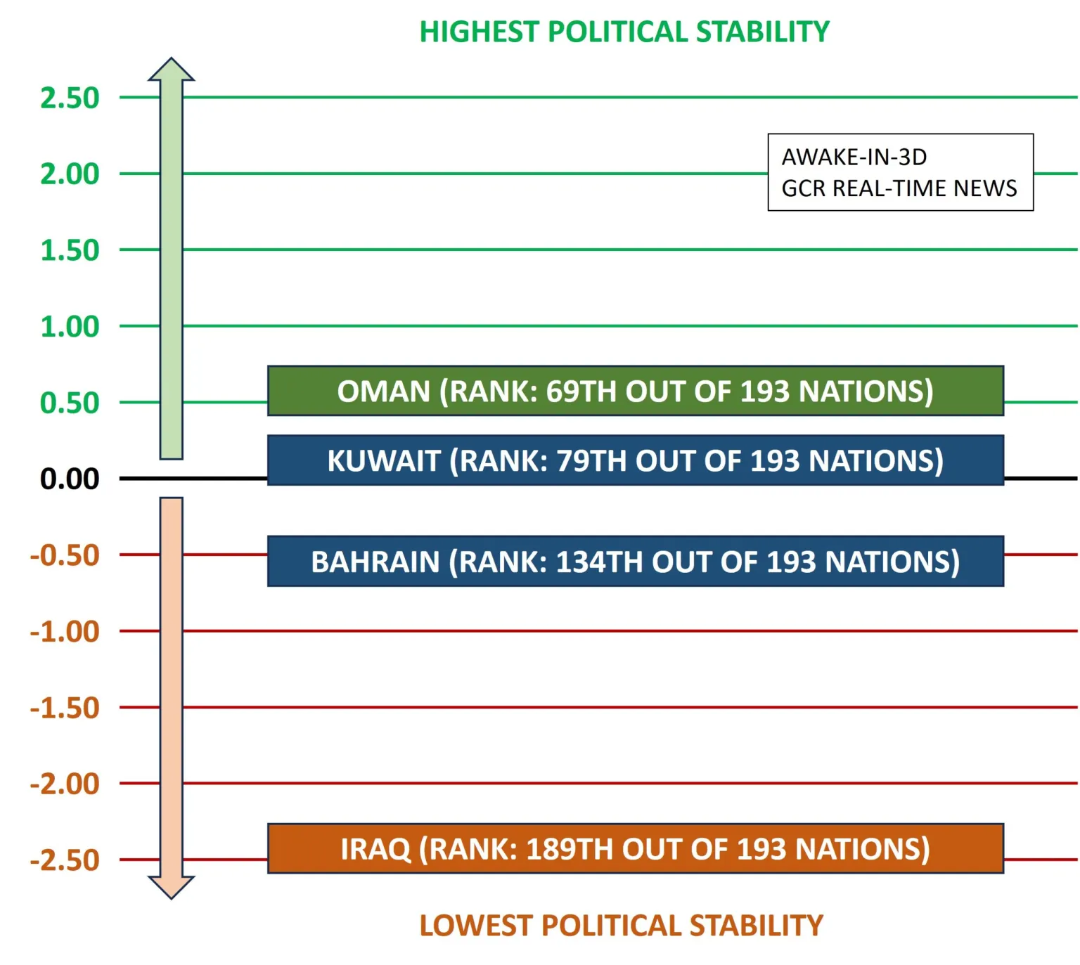

3.3 Political Stability: The Most Significant Challenge Facing an Iraqi Dinar RV

Political stability is a pivotal element in the realm of global economics and currency valuation. Understanding the political stability index is integral to our comparative analysis.

This index measures the perceived likelihood of a country’s government being destabilized or overthrown through unconstitutional or violent means, including politically motivated violence and terrorism.

An index value of 2.5 points indicates a strong and secure political environment, while a value of -2.5 points reflects a weak and insecure setting. The global average index value for 2021, derived from 193 countries, stands at -0.07 points.

Here is how the different countries rank in terms of overall political stability:

Oman: With a commendable index of 0.51, Oman holds the 69th place in the global political stability rankings, signifying a robust and stable political environment.

Kuwait: Kuwait secures the 79th position in global political stability standings with an index of 0.30, indicating a relatively stable political climate.

Bahrain: Bahrain ranks 134th in global political stability standings, albeit with a modestly negative index of -0.51, reflecting specific political challenges.

Iraq: Within this regional context, Iraq stands at the 189th position in political stability rankings out of a total of 193 countries. Iraq’s political stability index stands at -2.4, signifying a significantly weaker and insecure political environment.

Source Data: 2021 TheGlobalEconomy.com

Conclusion

In unison, these comparisons have underscored the interplay of economic indicators and political stability that define the currency dynamics within Iraq and its regional counterparts.

Clearly Iraq has a long way to go in reducing the political and financial corruption that dominates how the international business and foreign exchange markets view Iraq in terms of overall risk vs. reward.

Until the endemic corruption that plagues Iraq is addressed and mitigated, any serious attempts to float or peg a revalued IQD substantially higher will likely fail to achieve the desired results such an RV would yield.

Sources:

IMF Economic Data: https://data.imf.org/?sk=2ab615ea-9fb9-45b2-8d65-a031a6204fea

Political Stability Index: https://www.theglobaleconomy.com/rankings/wb_political_stability/

Section 1, Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events provided a detailed, historical context surrounding the Iraqi Dinar, This included its evolution, the impact of wars, the role of economic sanctions, and the popular reasons for speculations regarding an Iraqi Dinar revaluation.

Section 2, A Sky High Iraqi Dinar RV Boils Down to This identified and explained every key economic and political stability indicator that directly influences and supports a strong and stable currency exchange rate.

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/can-an-iraqi-dinar-rv-reach-3-00-matching-kuwait-heres-what-you-need-to-know/

Central Bank Losses Grow and Bailouts Arrive: Is the Federal Reserve Next? Awake-In-3D

Central Bank Losses Grow and Bailouts Arrive: Is the Federal Reserve Next?

On October 26, 2023 By Awake-In-3D

The global fiat currency debt system is facing an unprecedented financial crisis as central bank losses are significantly increasing month by month. Some are already requiring public bail-outs.

These institutions, which include the U.S. Federal Reserve, are grappling with losses that not only show no sign of relenting, but also pose a substantial risk to the stability of financial systems around the world.

As the financial system grapples with these mounting losses, the Federal Reserve may have immunity (for now).

Central Bank Losses Grow and Bailouts Arrive: Is the Federal Reserve Next?

On October 26, 2023 By Awake-In-3D

The global fiat currency debt system is facing an unprecedented financial crisis as central bank losses are significantly increasing month by month. Some are already requiring public bail-outs.

These institutions, which include the U.S. Federal Reserve, are grappling with losses that not only show no sign of relenting, but also pose a substantial risk to the stability of financial systems around the world.

As the financial system grapples with these mounting losses, the Federal Reserve may have immunity (for now).

Central bank losses continue to escalate, growing from month to month, posing a severe threat to global financial stability. Recent examples are Sweden’s Riksbank and the Bank of England.

The impact of these losses on everyday taxpayers is significant as they may ultimately shoulder the costs of bailouts to cover central bank deficits.

The U.S. Federal Reserve stands apart, thanks to its control over the world’s reserve currency and the use of deferred assets.

Global Central Bank Losses on the Rise

Flag outside of Sweden’s Central Bank building – Sveriges Riksbank

The financial predicament of central banks worldwide is indeed causing global concern, with the following facts highlighting the magnitude of the issue:

Sweden’s Riksbank reported a loss of over SEK 80 billion in 2022 resulting in a negative equity position (insolvency) of SEK -18 billion. It now needs a capital injection of at least SEK 80 billion to restore its equity to the basic level required by the Sveriges Riksbank Act.

The Bank of England, for instance, has already incurred losses estimated at £24 billion from selling bonds as of April 2023, a figure that experts predict could soon soar to a staggering £100 billion.

The U.S. Federal Reserve is not immune to these mounting losses, as it recently breached the $100 billion mark in losses.

In the midst of this financial turmoil, the U.S. Federal Reserve stands apart from the mounting financial problems of other central banks. Unlike its global counterparts, the Federal Reserve possesses a secret weapon.

A Growing Burden on Taxpayers – Bailouts

These central bank losses aren’t confined to the world of finance; they have a tangible impact on everyday people.

The burden of these losses ultimately falls on taxpayers, who may be required to cover the deficits created by these central bank losses.

The potential need for bailouts and the resulting public financial burden is an issue that cannot be ignored.

The Federal Reserve’s Secret Weapon

In the midst of this financial turmoil, the U.S. Federal Reserve stands apart from the mounting financial problems of all other central banks. Unlike its global counterparts, the Federal Reserve possesses a secret weapon.

The Fed is different because of its unique position as the issuer and controller of the world’s reserve currency, the U.S. Dollar.

Right to left: Janet Yellon – US Treasury Secretary and Jerome Powell – Federal Reserve Chairman

This distinctive role affords the Federal Reserve the following unparalleled advantages:

The Federal Reserve’s capacity to print its own currency provides it with the power to meet its debt obligations without the risk of default. This sets it apart from central banks that do not have this privilege.

The Federal Reserve employs a clever strategy involving “deferred assets,” which effectively conceals its losses and maintains normal operations without disruption. This strategy allows the Federal Reserve to maintain its operations indefinitely, even when facing mounting losses.

Can the Federal Reserve Go Bankrupt?

A crucial question arises: Can the U.S. Federal Reserve Bank go bankrupt, just like other central banks facing insurmountable losses? The answer lies in the Federal Reserve’s “unique” position of monetary privilege.

The Federal Reserve’s Special Bankruptcy Shield

The Federal Reserve’s financial stability is underpinned by its unique status as the issuer of the world’s reserve currency and its power to print money to meet its obligations. This affords the Federal Reserve the following key advantages:

Its control over the world’s reserve currency grants it the ability to meet debt obligations without the risk of insolvency, even as central bank losses mount.

The Federal Reserve’s use of “deferred assets” allows it to conceal losses effectively, ensuring its ongoing normal operations without disruption, even in the face of mounting financial challenges.

As the financial system grapples with these mounting losses, the Federal Reserve may have immunity (for now).

However, the broader implications of central bank losses raise questions about the global financial landscape and the role of central banks in the everyday lives of people around the world.

Supporting Articles:

https://www.reuters.com/markets/us/fed-losses-breach-100-billion-interest-costs-rise-2023-09-15/

https://thehill.com/opinion/finance/3955889-the-fed-is-bankrupt/

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/central-bank-losses-grow-and-bailouts-arrive-is-the-federal-reserve-next/

A Sky High Iraqi Dinar RV Boils Down to This: Awake-In-3D

A Sky High Iraqi Dinar RV Boils Down to This

On October 24, 2023 By Awake-In-3D

In RV/GCR

This is Section 2 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

A working knowledge of the economic and political factors that support a currency’s stability and strength is a powerful tool for determining the potential exchange rate within the Iraqi Dinar RV landscape.

This article outlines what you need to know.

Part 1, Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events provided a detailed, historical context surrounding the Iraqi Dinar, This included its evolution, the impact of wars, the role of economic sanctions, and the popular reasons for speculations regarding an Iraqi Dinar revaluation.

A Sky High Iraqi Dinar RV Boils Down to This

On October 24, 2023 By Awake-In-3D

In RV/GCR

This is Section 2 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

A working knowledge of the economic and political factors that support a currency’s stability and strength is a powerful tool for determining the potential exchange rate within the Iraqi Dinar RV landscape.

This article outlines what you need to know.

Part 1, Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events provided a detailed, historical context surrounding the Iraqi Dinar, This included its evolution, the impact of wars, the role of economic sanctions, and the popular reasons for speculations regarding an Iraqi Dinar revaluation.

Coming Soon

Part 3 will bring everything together to analyze and present a comparison between economic and political indicators for Iraq and the three strongest currencies in the world – Kuwait, Oman, and Bahrain.

This section explains the key economic and political stability indicators that are used to generally assess and determine the potential strength and stability of any nation’s currency.

2.1 Key Economic Indicators for Currency Strength and Stability for an Iraqi Dinar RV

While there are many economic indicators that influence currency exchange rates, these are the top five indicators that best serve the scope of this study (keeping it straight forward).

Inflation Rates: Lower inflation rates signify a stable economy, bolstering a currency’s value.

Economic Growth: Indicators like the GDP growth rate are essential in evaluating a country’s economic health. Strong economic growth often results in a robust currency.

Current Account Balance: A surplus in the current account, where a country exports more than it imports, positively supports currency appreciation.

Public Debt: Countries with large public debts are less appealing to foreign investors due to the risk of inflation and default, putting downward pressure on currency value.

Foreign Exchange Reserves: The amount of foreign currency held by a country influences its own currency’s value. Countries with substantial reserves have the ability to better manage and maintain (currency pegs) their currency’s value.

2.2 Understanding Currency Peg Policies

A nation’s monetary policy related to currency pegs ultimately sets the exchange rate. Large economies today, such as the United States and the European Union, allow their currencies float (no peg is used) solely on market forces.

Smaller economies will peg their currencies to other, widely utilized currencies such as the U.S. Dollar, the Euro, or a basket of globally dominant currencies.

When countries engage in international trade, they aim to maintain the stability of their currency. Currency pegging, or fixing, is a method used to achieve this. It involves tying a nation’s currency to another currency, such as the U.S. dollar.

Countries choose to peg their currency to safeguard the competitiveness of their exported goods and services. A weaker currency benefits exports and tourism, as it makes everything more affordable for foreign buyers.

The fluctuation of exchange rates can negatively affect international trade, making currency pegging a viable option for stability.

Many countries, including some that peg their currency to the U.S. dollar, opt for this approach to ensure their goods and services remain competitive.

2.3 Ending the Bretton Woods Agreement Created Fixed vs. Floating Currency Practices (Global Fiat Currencies)

The 1944 Bretton Woods Agreement pegged the U.S. dollar to gold, reducing volatility in international trade relations. As a result, most global nations then pegged their currencies to the U.S. dollar and it became the new world reserve currency.

THE 1944 BRETTON WOODS CONFERENCE WHERE THE US DOLLAR WAS PEGGED TO GOLD AND BECAME THE NEW WORLD RESERVE CURRENCY

However, the Bretton Woods system ended in 1971 when the United States de-pegged the dollar from gold, and the Great Global Fiat Currency System Experiment was born almost overnight.

Since then, countries now decide how their currencies operate in the foreign exchange market – a hard peg or a floating exchange rate.

There are, in essence, two primary types of currency exchange rate policies today: floating and fixed.

5-YEAR CHART: THE US DOLLAR IS A FLOATING CURRENCY RATE – CHANGING VALUE THROUGH MARKET FORCES

Major currencies, like the Japanese yen, euro, and U.S. dollar, are floating currencies, with their values determined by supply and demand in foreign exchange markets. This system is influenced by market forces, signaling economic strength or weakness.

On the other hand, fixed currencies derive their value from being linked to another currency, providing increased stability. Many developing economies use fixed exchange rates to ensure stability in their international trade activities.

5-YEAR CHART: THE IQD IS A FIXED CURRENCY PEGGED TO THE US DOLLAR AND RARELY CHANGES

Iraq employs a fixed exchange rate policy, pegging the IQD to the U.S. Dollar.

2.4 Political Stability Likely the Critical Factor Influencing Potential Iraqi Dinar RV Rate

Countries with greater political stability are more likely to maintain stable currencies with higher exchange rate valuations. Political stability is a key factor in currency valuation and vitally important for a “high-rate” Iraqi Dinar RV.

For a significant currency revaluation to take place, Iraq must address various challenges, including political instability, corruption, and security concerns. Achieving economic stability and implementing necessary reforms are crucial prerequisites for the potential revaluation of the IQD.

2.4.1 The Political Stability Index

The Political Stability Index measures the likelihood that a government will be destabilized or overthrown by unconstitutional or violent means, including politically motivated violence and terrorism. It is based on various indexes from reputable sources such as the Economist Intelligence Unit, the World Economic Forum, and the Political Risk Services.

A Political Stability Index value of 2.5 points indicates a strong, secure political environment in a country. Conversely, a country with a value of (-2.5) points indicate a very weak, insecure political environment. The average index value for 2021, based on 193 countries, was (-0.07) points.

Source: https://www.theglobaleconomy.com/rankings/wb_political_stability/

Conclusion of Section 2

This section has examined essential economic and political stability indicators that influence a country’s currency valuation. Understanding the role of these factors is vital in evaluating an Iraqi Dinar RV exchange rate potential.

In Section 3, we will apply what we’ve learned here and review how Iraq compares to a regional selection of strong, stable currencies, assessing Iraq’s economic and political position in the context of its neighboring countries.

This will reveal a clearer picture of how Iraq stacks up and its ability to set and maintain a much stronger exchange rate for the IQD in an Iraqi Dinar RV.

Part 1, Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events provided a detailed, historical context surrounding the Iraqi Dinar, This included its evolution, the impact of wars, the role of economic sanctions, and the popular reasons for speculations regarding an Iraqi Dinar revaluation.

Coming Soon

Part 3 will bring everything together to analyze and present a comparison between economic and political indicators for Iraq and the three strongest currencies in the world – Kuwait, Oman, and Bahrain.

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/a-sky-high-iraqi-dinar-rv-boils-down-to-this/

Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events: Awake-In-3D

Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events

On October 23, 2023 By Awake-In-3D

In RV/GCR

This is Section 1 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

Amidst years of speculation, rumors, and expectations surrounding an Iraqi Dinar Revaluation (RV), there exists a base case to be made deserving serious consideration.

Coming Soon

Part 2 will identify and explain every key economic and political stability indicator that directly influences and supports a strong and stable currency exchange rate.

Part 3 will bring everything together to analyze and present a comparison between economic and political indicators for Iraq and the three strongest currencies in the world – Kuwait, Oman, and Bahrain.

Staging an Iraqi Dinar Revaluation (RV): A Unique Background of Events

On October 23, 2023 By Awake-In-3D

In RV/GCR

This is Section 1 of: The Ultimate Guide to Every Economic and Political Reason for an Iraqi Dinar Revaluation (RV)

Amidst years of speculation, rumors, and expectations surrounding an Iraqi Dinar Revaluation (RV), there exists a base case to be made deserving serious consideration.

Coming Soon

Part 2 will identify and explain every key economic and political stability indicator that directly influences and supports a strong and stable currency exchange rate.

Part 3 will bring everything together to analyze and present a comparison between economic and political indicators for Iraq and the three strongest currencies in the world – Kuwait, Oman, and Bahrain.

However, it is crucial to ground any discussion in the real economic, financial, and political environment surrounding Iraq today.

While the speculative nature of previous claims may not align with economic reality, it is important to acknowledge the continuous improvements witnessed in Iraq’s economic development.

These advancements provide a legitimate rationale in support of considering the eventual revaluation of the Iraqi Dinar.

This report outlines a comprehensive set of factors contributing to this perspective, aiming to provide a thorough analysis of the landscape surrounding the case for an Iraqi Dinar revaluation (RV).

1.1 The Evolution of the Iraqi Dinar

The history of the Iraqi Dinar dates back to its introduction as Iraq’s official currency in 1932. At its inception, the IQD was at par with the British pound, reflecting a stable economy and strong financial position.

However, the subsequent decades witnessed a series of significant events that led to the devaluation of the IQD.

1.1.1 The Impact of Wars on the IQD

The Iran-Iraq war (1980-1988) and the subsequent Gulf War in 1991 had profound effects on Iraq’s economy and its currency.

These prolonged conflicts strained resources, disrupted economic stability, and resulted in the devaluation of the Iraqi Dinar.

See related article: IQD History: CBI Governor Speaks Publicly About Currency RV/RD in 2011

1.1.2 Economic Sanctions and Trade Restrictions

Economic sanctions, imposed by the international community due to various political and security issues, have played a pivotal role in the fluctuations of the Iraqi Dinar’s value.

Sanctions often limited Iraq’s ability to engage in international trade, leading to a decline in foreign currency reserves and contributing to the devaluation of the IQD.

1.2 Popular Reasons Fueling Speculation around an IQD Revaluation

Despite these challenges, speculations about the potential revaluation of the Iraqi Dinar have persisted.

Proponents of an Iraqi Dinar RV often highlight several primary arguments supporting their position.

These include:

1.2.1 Iraq’s Abundant Oil Reserves

Likely the most popular reason supporting expectations of an Iraqi Dinar revaluation is that Iraq possesses one of the world’s largest oil reserves, and the successful exploitation of these resources should significantly boost its economic potential.

This substantial oil wealth is a critical factor in the potential revaluation of the IQD.

SIDEBAR: Oil Credits for the USA?

Many argue that Iraq could support a high exchange rate to the U.S. Dollar because of a much rumored “Oil Credit Agreement” purportedly set up between Iraq and the USA after the Gulf War.

However, there is no conclusive evidence (other than what’s posted on various RV related internet sites) that supports such an agreement actually exists.

The trickle of oil imported from Iraq renders any Oil Credits insignificant. Source: US Energy Information Administration.

Furthermore, if such an Oil Credit Agreement did exist, the fact remains that in 2022:

The USA consumed 19.1 million barrels/day of petroleum

The USA produced 19.99 million barrels/day of petroleum

The USA imported 8.32 million barrels/day of petroleum

The USA only imported an average of 332 thousand barrels/day from Iraq (4% of USA’s total petroleum imports)

Source: US Energy Information Administration (https://www.eia.gov/energyexplained/oil-and-petroleum-products/imports-and-exports.php)

Source: US Energy Information Administration.

Given that the USA imports such an insignificant amount of petroleum from Iraq, the value of any “Oil Credits” would not support any meaningful role in an Iraqi Dinar RV.

1.2.2 Iraq’s Prospects of Economic Growth

Another popular reason offered in support of an IQD revaluation is Iraq’s potential for continued economic growth.

Underpinned by its oil resources and untapped economic potential, the community of IQD RV’ers has continued to grow over the years with committed interest.

Certainly there is a valid case to be made for a successful Iraqi Dinar revaluation being closely tied to Iraq’s ability to harness its economic potential.

Does Iraq now have a robust economic credentials to support a stable, high-value exchange rate?

A detailed analysis of Iraq’s key economic indicators will be presented in Section 3 of this report (link).

1.2.3 Political Stabilization in Iraq

Finally, Iraq’s purported progress in establishing political stability is another popular argument made in support of a significant currency revaluation.

Iraq’s journey towards political stability has been marred by challenges like corruption, security concerns, and political instability.

Protests in Baghdad over corruption, lack of jobs, and poor services in 2019. Photo: REUTERS/Khalid al-Mousily

As Iraq takes steps towards establishing lasting political stability and independent governance, the probability of a major currency revaluation (RV) would definitely increase.

Yet, has the government of Iraq (GOI) really made significant inroads to political stability?

This subject will be outlined in Section 3 of this report.

1.3 International Agencies and their Effect on Exchange Rates

It’s important to clarify that international agencies, such as the United Nations Security Council (UNSC) and the International Monetary Fund (IMF), do not possess the direct authority to arbitrarily set a country’s currency exchange rate (valuation).

This means that no international agency can mandate that the Iraqi Dinar (IQD) be changed from $3.00 per IQD to $0.0007 per IQD – or visa versa.

IMF members pose for a photograph April 22, 2017 at the IMF Headquarters in Washington, DC. Photo: Getty Images News

Currency exchange rates are primarily shaped by market forces, economic indicators, and the nation’s own financial policies.

While these agencies do not directly dictate exchange rates themselves, they do exert influence through mechanisms such as economic and geopolitical sanctions which may significantly impact a nation’s currency value.

1.4 Executive Orders and Economic Sanctions were a backdrop for an Iraq Dinar Revaluation

In the aftermath of the Gulf War and during the reconstruction of Iraq, a series of Executive Orders were issued to address assets, legal issues, and economic stability.

These Executive Orders collectively aimed to protect Iraqi assets, maintain the stability and security of Iraq, and support post-conflict reconstruction and development. Notably:

1.4.1 Executive Orders Effecting Iraqi Economic Reality

President George W. Bush signs executive orders and directives in the Oval Office on August 27, 2004 . Photo: White House Archives by Paul Morse

Here’s a list of every EO and U.S. Treasury Sanctions related to Iraq.

Executive Order 13303 (May 22, 2003)

Purpose: Protect the Development Fund for Iraq and Iraqi assets from being seized by creditors.

Safeguard the Development Fund for Iraq.

Prohibit attachment or judicial processes against Iraqi assets.

Ensure oil proceeds are used for Iraq’s reconstruction.

Maintain the stability and security of Iraq.

Executive Order 13315 (August 28, 2003)

Purpose: Expand measures to address security threats to Iraq’s stability, security, and reconstruction.

Broaden sanctions against individuals and entities.

Counteract threats to Iraq’s peace and security.

Support economic reconstruction and political reform.

Provide humanitarian aid to the Iraqi people.

Executive Order 13350 (July 29, 2004)

Purpose: Terminate previous national emergencies and modify EOs to address Iraq’s stability and security.

End prior national emergencies.

Modify EOs to counter Iraq’s stability threats.

Protect Iraq’s assets.

Promote reconstruction and development.

Executive Order 13364 (November 29, 2004)

Purpose: Modify protections for the Development Fund for Iraq while recognizing changes in Iraq’s circumstances.

Terminate prohibitions related to the Development Fund.

Balance asset protection with Iraq’s needs.

Address the evolution of Iraq’s financial situation.

Maintain the national emergency declared in EO 13303.

Executive Order 13438 (July 17, 2007)

Purpose: Block the property of individuals and entities that threaten Iraq’s stabilization efforts.

Block assets of those threatening Iraq’s stability.

Prohibit contributions to or from blocked individuals.

Counteract violence undermining peace and reconstruction.

Support Iraq’s economic and political progress.

Executive Order 13668 (May 27, 2014)

Purpose: End immunities granted to the Development Fund for Iraq, considering Iraq’s changing circumstances.

Terminate immunities related to the Development Fund.

Recognize changes in Iraq’s situation.

Balance asset protection with Iraq’s progress.

Maintain the national emergency declared in EO 13303.

1.4.2 Specifics Regarding Executive Order 13303

EO13303 Signed May 22, 2003. Photo: The American Presidency Project

There is much speculation over Executive Order 13303, issued by President George W. Bush in 2003, regarding the revaluation (RV) of the Iraqi Dinar.

Aimed to safeguard the Development Fund for Iraq and protect Iraqi petroleum-related assets, this order prohibited the attachment, judgment, or lien against these assets, aiming to facilitate Iraq’s reconstruction and stability.

Executive Order 13303 has been continuously extended beyond its initial issuance in 2003.

On May 16, 2023, a notice was issued to extend the national emergency with respect to the stabilization of Iraq, originally declared by Executive Order 13303 on May 22, 2003.

The order aimed to prevent obstacles to the orderly reconstruction of Iraq, the restoration of peace and security, and the development of political, administrative, and economic institutions in Iraq.

Executive Order 13303 does not directly mention the Iraqi Dinar currency or address a potential revaluation of the Iraqi Dinar but plays a role in protecting Iraq’s economic interests.

1.4.3 Economic Actions and Sanctions Levied Against Iraq by the U.S. Treasury

There were a number of Actions and Sanctions-related documents issued by the U.S. Treasury against Iraq. Below is a summarized explanation of each document.

OFAC Sets Out Expectations for Compliance with U.S. Sanctions

Establishing the Central Bank of Iraq/Oil Proceeds Receipts Account (May 22, 2003)

This document, issued on May 22, 2003, establishes the Central Bank of Iraq/Oil Proceeds Receipts Account.

The purpose of this account is to receive funds generated from the sale of Iraqi petroleum and petroleum products. It plays a crucial role in managing and allocating the revenue generated from oil sales for the benefit of Iraq.

Establishing the Iraq Stabilization and Insurgency Sanctions Regulations (June 13, 2003)

This document serves as an overview of the Iraq Stabilization and Insurgency Sanctions Regulations (ISISR) and was created around the same period as the ISISR.

It discusses several aspects of the sanctions on Iraq, including exporting to Iraq, financial transactions, prohibitions related to Iraqi cultural property, immunities from attachment, and exemptions for U.S. military forces operating in Iraq. The document provides a broader perspective on the sanctions’ context and application.

The Termination of Iraqi Sanctions and Removal from Chapter V of 31 C.F.R. (September 13, 2010)

What is 31 CFR Chapter V?

Title 31: Chapter V – OFFICE OF FOREIGN ASSETS CONTROL, DEPARTMENT OF THE TREASURY

Title 31 refers to Code of Federal Regulations (CFR) for the U.S. Department of Treasury

Subtitle B refers to Regulations Relating to Money and Finance

Chapter V refers specifically to the Office of Foreign Assets Control under the Department of the Treasury

https://www.ecfr.gov/current/title-31/subtitle-B/chapter-V/part-576

In September 2010, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) marked a significant milestone by formally ending economic sanctions on Iraq. This marked the removal of the Iraqi Sanctions Regulations from 31 C.F.R. Chapter V and introduced the Iraq Stabilization and Insurgency Sanctions Regulations (ISISR).

This transition was in line with several Executive Orders, including Executive Order 13303 (May 22, 2003), Executive Order 13315 (August 28, 2003), Executive Order 13350 (July 29, 2004), Executive Order 13364 (November 29, 2004), and Executive Order 13438 (July 17, 2007).

On September 13, 2010, the ISISR replaced the earlier Iraqi Sanctions Regulations, and as of that date, there were no comprehensive economic sanctions remaining against Iraq.

The ISISR contain the current OFAC restrictions related to Iraq and Iraqi property. As of the date of this document, there were no broad-based sanctions against Iraq. However, specific individuals and entities associated with the former Saddam Hussein regime were subject to prohibitions and asset freezes.

These individuals and entities were determined to have committed or posed a significant risk of committing acts of violence that could threaten the peace, stability of Iraq, the Government of Iraq, or undermine efforts for economic reconstruction, political reform, or humanitarian assistance in Iraq.

On September 13, 2010, the ISISR replaced the earlier Iraqi Sanctions Regulations, and as of that date, there were no comprehensive sanctions against Iraq.

Summary

This section has provided a detailed historical context surrounding the Iraqi Dinar, including its evolution, the impact of wars, the role of economic sanctions, the popular reasons for speculations regarding an Iraqi Dinar revaluation, and the role of international agencies and Executive Orders in currency exchange rates.

Coming Soon

Section 2 will identify and explain every key economic and political stability indicator that directly influences and supports a strong and stable currency exchange rate.

Section 3 will bring everything together to analyze and present a comparison between economic and political indicators for Iraq and the three strongest currencies in the world – Kuwait, Oman, and Bahrain.

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/staging-an-iraqi-dinar-revaluation-rv-a-unique-background-of-events/

Liquidation of China’s U.S. Bond Holdings Breaks Record in August: Awake-In-3D

Liquidation of China’s U.S. Bond Holdings Breaks Record in August:

On October 20, 2023 By Awake-In-3D

In GCR Roadmap Events, Fiat Debt System Collapse

China’s ongoing selloff of U.S. Treasury Bonds is a strong indicator of an impending crisis in global fiat currency debt markets.

What may appear to be small ripples in financial markets often foreshadow monumental waves that can reshape the financial landscape. Such is the case with the ongoing selloff of China’s U.S. bond holdings.

This liquidation trend may well be an unequivocal indication of an approaching crisis in U.S. dollar credit and bond markets, hinting at the logical conclusion of the global fiat currency debt system.

“China’s divestment of U.S. Bonds and Equities is more than just a financial transaction; it is a signpost on the roadmap to the collapse of the fiat currency system and the rise of a new asset-backed system via an RV/GCR”

Liquidation of China’s U.S. Bond Holdings Breaks Record in August:

On October 20, 2023 By Awake-In-3D

In GCR Roadmap Events, Fiat Debt System Collapse

China’s ongoing selloff of U.S. Treasury Bonds is a strong indicator of an impending crisis in global fiat currency debt markets.

What may appear to be small ripples in financial markets often foreshadow monumental waves that can reshape the financial landscape. Such is the case with the ongoing selloff of China’s U.S. bond holdings.

This liquidation trend may well be an unequivocal indication of an approaching crisis in U.S. dollar credit and bond markets, hinting at the logical conclusion of the global fiat currency debt system.

“China’s divestment of U.S. Bonds and Equities is more than just a financial transaction; it is a signpost on the roadmap to the collapse of the fiat currency system and the rise of a new asset-backed system via an RV/GCR”

The financial markets have been saturated with discussions about rising yields, with experts offering various explanations for the recent credit/bond market phenomenon. However, we cannot ignore the prominent role played by a significant player on the global stage—China.

China’s consistent and aggressive selloff of U.S. Treasuries, spanning 20 of the past 22 months, is not merely an isolated act but rather a pivotal piece of a broader puzzle.

I view China’s deliberate divestment of U.S. bonds as a compelling indicator of an impending crisis in U.S. dollar credit and bond markets, ultimately hinting at the fate of the global fiat currency debt system.

I further believe we are witnessing the increasing tremors of a seismic shift in the foundations of the global financial system.

Key Facts

China held over $1.1 trillion in U.S. Treasury securities as of September 2021.

Chinese investors liquidated a record-breaking $21.2 billion worth of U.S. bonds and stocks in August 2023.

China’s U.S. bond holdings witnessed a selloff in 20 of the past 22 months, signaling a consistent trend.

Chinese investors also sold a record $5.1 billion of U.S. stocks in August 2023, contributing to the selloff in U.S. securities.

This divestment of U.S. bonds and stocks by China raises concerns about the impact on U.S. credit and bond markets and the global fiat currency financial system.

In recent months, the world has witnessed tumultuous movements in financial markets, particularly in the United States, leading to growing concerns about rising yields and their impact on global economies.

While mainstream pundits debated the causes behind these changes, it has become increasingly clear that one of the major players affecting U.S. bond markets is none other than China’s U.S. bond holdings.

In August, Chinese investors executed the most substantial liquidation of U.S. bonds and stocks in four years, raising questions about their motives and the consequences for the global financial landscape.

The data from the U.S. Treasury reveals a striking trend – China has been actively reducing its holdings of U.S. Treasuries for the past 22 months, with an eye-catching 20 of those months witnessing a consistent selloff.

China’s Selloff of U.S. Securities is part of a global trend

Source: US Treasury Data

While there are various theories to explain rising yields, it appears that China’s aggressive selling of U.S. Treasuries plays a pivotal role in this equation. Foreign central banks have also been involved in this selloff, notably dumping the most Treasuries since the beginning of the year.

However, the situation is more complex than it initially appears, as a broader perspective unveils a more intricate narrative. According to Bloomberg, in August, Chinese investors liquidated substantial amounts of U.S. bonds and stocks. This raises speculation that Beijing may be using these measures to protect its currency, the yuan, as it continues to weaken against the U.S. dollar.

The parallels with Russia’s decision to offload its Treasury holdings in 2018, preempting the weaponization of the U.S. dollar against it, are hard to ignore.

Given China’s territorial ambitions, such as the potential annexation of Taiwan in the future, it is prudent to consider that they might be distancing themselves from U.S. Treasury holdings, anticipating potential financial constraints similar to those faced by Russia.

Analyzing the specifics of China’s U.S. bond holdings liquidation in August, the bulk of the $21.2 billion in sales comprised Treasuries and U.S. equities. Contrary to the belief that China refrained from selling U.S. Treasuries, the data shows that they actively reduced their holdings of these government securities.

This selloff occurred as the onshore yuan experienced a significant depreciation against the U.S. dollar, reaching its lowest point since November 2022.

This led Beijing to instruct state-owned banks to intervene in the currency market to stabilize the yuan’s value, reinforcing the theory that the liquidation was intended to amass U.S. dollar cash reserves for potential intervention operations.

However, this liquidation might be part of a broader strategy to ensure China has access to U.S. dollars when needed to safeguard the yuan.

A similar rationale could apply to the sale of U.S. equities in their portfolio. In August, Chinese investors also sold a record $5.1 billion worth of U.S. stocks, notably around the same time when the S&P index witnessed a significant drop following the Federal Reserve’s final rate hike decision in late July.

The August selloff of U.S. treasury and agency bonds raises questions regarding the demand for U.S. debt, which has traditionally been a cornerstone of the global fiat financial system.

In conclusion, the ongoing liquidation of China’s U.S. bond holdings, particularly in August’s record-breaking selloff, is sending ripples through the global financial markets. While the exact motivations behind this move remain speculative, the possibility that China is preparing for economic contingencies and potential challenges, such as a weakened yuan or geopolitical concerns, cannot be dismissed.

The ongoing crisis in U.S. dollar credit and bond markets poses a fundamental question about the sustainability of the current fiat currency debt system.

In my view, China’s divestment of U.S. Bonds and Equities is more than just a financial transaction; it is a signpost on the roadmap to the collapse of the fiat currency system and the rise of a new asset-backed system via an RV/GCR.

Supporting articles:

Yahoo Finance: https://finance.yahoo.com/news/china-sells-most-us-assets-223331094.html?fr=sycsrp_catchall

Bloomberg News: https://www.bloomberg.com/news/videos/2023-10-20/china-economy-has-bottomed-out-standard-chartered-says-video

BNN Finance: https://bnn.network/finance-nav/chinas-sell-off-of-us-treasury-bonds-a-shift-on-the-global-financial-chessboard/

My primary thesis is that the Global Fiat Currency Debt System must come to its logical conclusion before Our GCR will be introduced – which includes the release of the “General Redemptions” funding for RV/GCR exchanges.

But how do you track the connected events and progress of the logical conclusion of the Fiat Financial System?

It’s easy when you follow my unique RV/GCR Roadmap right here at GCR Real-Time News

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/liquidation-of-chinas-u-s-bond-holdings-breaks-record-in-august/

Tracking the Global Shift of Gold as the East Prepares for a Global Currency Reset (GCR): Awake-In-3D

Tracking the Global Shift of Gold as the East Prepares for a Global Currency Reset (GCR)

On October 16, 2023 By Awake-In-3D

In RV/GCR, Fiat Debt System Collapse

A Golden Eastern Shift is Hitting the Fan of the West

Throughout the on-goings of global finance and geopolitics, a tectonic shift is quietly unfolding. As the global shift of gold continues moving from West to East, it becomes obvious that the world’s economic order is also shifting in preparation for an impending financial system reset.

At its core, this narrative focuses on the discerning movements within the international monetary landscape, hinting at the logical conclusion of the global fiat currency debt system.

“This transference of gold holdings and trade practices is a direct consequence of an inescapable truth: the global fiat currency debt system, which has underpinned the financial structure for decades, is nearing the point of a credit market freeze and collapse.”

Tracking the Global Shift of Gold as the East Prepares for a Global Currency Reset (GCR)

On October 16, 2023 By Awake-In-3D

In RV/GCR, Fiat Debt System Collapse

A Golden Eastern Shift is Hitting the Fan of the West

Throughout the on-goings of global finance and geopolitics, a tectonic shift is quietly unfolding. As the global shift of gold continues moving from West to East, it becomes obvious that the world’s economic order is also shifting in preparation for an impending financial system reset.

At its core, this narrative focuses on the discerning movements within the international monetary landscape, hinting at the logical conclusion of the global fiat currency debt system.

“This transference of gold holdings and trade practices is a direct consequence of an inescapable truth: the global fiat currency debt system, which has underpinned the financial structure for decades, is nearing the point of a credit market freeze and collapse.”

Regions and countries outside the Western-allied nations are keenly aware that the 50-year-old, but increasingly fragile, global fiat currency experiment is teetering on the brink of a debt-fueled implosion.

This shift underscores a remarkable global preparation for an impending global currency reset (GCR), poised to realign the very fundamentals of the current global financial structure.

The Global Shift of Gold: Key Facts and Figures

Central banks bought a record-breaking 1,136 tons of gold in 2022, the highest in over 70 years.

In the first half of 2023, central banks increased their gold reserves by 378 tons, surpassing the previous half-year record from 2019.

China was the leading purchaser of gold, followed by Singapore, Poland, India, and the Czech Republic.

Central banks outside Western nations significantly contributed to the growing trend of gold purchases.

Gold prices surged in various non-Western currencies in 2023, including a 14.6% increase in Indian rupees, 18.0% in Chinese renminbi, 34.3% in Russian rubles, 22.1% in South African rand, and 114.0% in Turkish lira.

The BRICS nations have been reducing their holdings of soaring US government debt, with the BRICS’ share declining from 10.4% to 4.1% since January 2012.

The East, notably China, the United Arab Emirates, and Russia, is expanding its gold trading infrastructure to create alternatives to Western-dominated gold trading centers.

Countries like China and Russia have positioned themselves as top gold producers, ranking among the world’s top three for years.

Russian gold exports to China have surged significantly since mid-2022, indicating a structural shortage of gold in the Chinese market.

Chinese refineries on the LBMA’s Good Delivery List have increased from six to thirteen since 2009.

The number of regular (full) members of the LBMA from China has grown from one to seven in just 15 years.

India has established a trading infrastructure for gold futures contracts on the Multi Commodity Exchange of India Limited (MCX) and the India International Bullion Exchange (IIBX) for trading spot gold contracts.

Moscow is developing a new infrastructure for precious metals trading, independent of Western institutions, to establish a Moscow World Standard (MWS) for precious metals trading, a Moscow International Precious Metals Exchange, and a new gold price fixing system.

Shifting Balances: The Old and New World Order

The Western nations have long held the reins of global economic influence, effectively commanding international monetary policies and dominating currency markets.

However, the discernible global shift of gold from West to East is more than just the physical transfer of a precious metal—it signifies a profound global realignment.

Purchases of gold moving through the SCO now dominate Western markets. Source: World Gold Council, Incrementum AG

This transference of gold holdings and trade practices is a direct consequence of an inescapable truth: the global fiat currency debt system, which has underpinned the financial structure for decades, is nearing the point of a credit market freeze and collapse.

In 2022, central banks around the world, especially in non-Western countries, bought a remarkable 1,136 tons of gold—the largest recorded gold purchases by central banks in over 70 years.

This trend in the global shift of gold is not slowing down; during the first half of 2023, central banks increased their gold reserves by a staggering 378 tons. What’s even more striking is that the majority of these purchases came from countries in the East.

China led the way, followed by Singapore, Poland, India, and the Czech Republic. This move is significant, as it marks a shift in the center of gravity of gold ownership and underscores the East’s deepening interest in the precious metal.

“The evidence for a financial system transformation is rapidly taking shape, poised to transition from fiat currencies to an alternative financial system backed by tangible assets.”

With the formal introduction of these regions and alliances, and their resolute stance to safeguard their wealth and economic interests, the stage is set for a monumental transformation of the global financial system. This paradigm shift, underscored by the shifting sands of gold ownership, serves as a tangible harbinger of a new era—ushering in a post-fiat, asset-backed financial world.

What This Global Shift of Gold Means

As gold flows to regions outside the Western-allied nations, the world witnesses a tangible shift in the global economic order.

The evidence for a financial system transformation is rapidly taking shape, poised to transition from fiat currencies to an alternative financial system backed by tangible assets.

The proactive steps taken by Eastern nations and alliances are a reflection of their profound awareness that the financial landscape is teetering on the brink of a substantial reset, rendering the ongoing paradigm obsolete.

The East, both resolute and informed, appears to be standing at the leading edge of this transformative process, heralding a global currency reset (GCR) that not only promises a more robust and resilient financial future, but also signifies the logical conclusion of the fading fiat currency experiment.

The age-old verity that “a global shift of gold moving from the West to the East” encapsulates a world in flux, cognizant of the imminent financial reset, and earnestly preparing for the world beyond the fiat debt system.

The new financial system will pivot on tangible assets like gold as an integral component of a post-global fiat currency debt structure.

Supporting article: https://goldswitzerland.com/5-signs-that-gold-will-increasingly-flow-to-the-east/

© GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

Breaking News: A Zimbabwe Single Currency is Now on Track: Awake-In-3D

Breaking News: A Zimbabwe Single Currency is Now on Track

On October 15, 2023 By Awake-In-3D

Amidst a backdrop of historical financial turmoil, Zimbabwe has embarked on an ambitious quest to establish a Zimbabwe single currency.

In my opinion, this is relevant to the RV/GCR since Zimbabwe would need it’s own sovereign currency, instead the basket of foreign currencies they use today, in order to participate in the GCR.

How could a country have an asset backed currency if they don’t currently have their own currency?

This journey, laden with rich history and bold decision-making, reflects the nation’s steadfast commitment to restoring economic stability.

Breaking News: A Zimbabwe Single Currency is Now on Track

On October 15, 2023 By Awake-In-3D

Amidst a backdrop of historical financial turmoil, Zimbabwe has embarked on an ambitious quest to establish a Zimbabwe single currency.

In my opinion, this is relevant to the RV/GCR since Zimbabwe would need it’s own sovereign currency, instead the basket of foreign currencies they use today, in order to participate in the GCR.

How could a country have an asset backed currency if they don’t currently have their own currency?

This journey, laden with rich history and bold decision-making, reflects the nation’s steadfast commitment to restoring economic stability.

This article outlines the multifaceted past and present events surrounding the evolution of the Zimbabwe single currency, what this transformation signifies, and provides insight into Zimbabwe’s dynamic financial landscape.

“We agreed that for us to survive we had to create a basket of currencies and allow our currency to die. It could have been a wrong decision but that is what happened in 2009. However, as a country, we must have a currency which we call our own.”

Zimbabwe President Mnangagwa

A Historical Perspective

From Hyperinflation to Multi-currency Basket

Zimbabwe’s financial saga was turbulent, characterized by hyperinflation and economic instability.

It was in 2009 that the country took the pivotal step of introducing a basket of foreign currencies, marking the transition from a period of hyperinflation to relative stability.

The necessity of a local currency became apparent, serving as the cornerstone for future endeavors

Government Action in 2009

In 2009, a committee was convened under the chairmanship of President Mnangagwa by former President Mugabe to address the financial crisis.

This committee concluded that adopting a basket of currencies was a vital strategy for survival. The decision to create this unique financial framework marked a turning point in Zimbabwe’s economic landscape.

The “Basket of Currencies” Arrangement

The current financial arrangement allows the use of a mixture of foreign currencies alongside the local currency. Under Statutory Instrument 118A of 2022, this arrangement is secured until December 2025.

While the current setup has stabilized the economy to an extent, Zimbabwe now sets its sights on establishing a Zimbabwe single currency.

The Path to a Zimbabwe Single Currency

Presidential Vision

President Mnangagwa’s vision for Zimbabwe’s financial future is clear: the nation needs its own single currency.

He strongly emphasizes the importance of this, viewing it as a foundation for achieving sustainable economic growth and development. In his words, “There is no country that can grow without its own currency.”

Benefits of a Single Currency

A single national currency grants the government greater autonomy in monetary policy, enabling more effective management of capital flows, and ensuring the protection of the nation’s interests.

This approach is crucial for economic autonomy and sovereignty. President Mnangagwa underscores the significance, stating, “We must bite the bullet, whether it gives us some suffering for a period, we shall proceed to have our own currency.”

The Road Ahead for a Zimbabwe Single Currency

“We want a single currency, and we are going there.”

Zimbabwe President Mnangagwa

As Zimbabwe moves steadily towards the realization of a Zimbabwe single currency, it faces a series of challenges.

However, the commitment and cooperation of stakeholders, the government, and the financial sector ensure a deliberate and organized transition.

Stakeholder Concerns

During the Zimbabwe Economic Development Conference (ZEDCON), stakeholders articulated their need for a well-defined currency reform roadmap.

The approaching 2025 deadline for the multicurrency regime has triggered caution within financial institutions concerning the extension of long-term foreign currency loans. In the words of President Mnangagwa, “We want a single currency, and we are going there.”

Economic Autonomy

Zimbabwe’s transition towards a single currency reflects its unwavering determination to regain economic autonomy and strengthen its monetary policy.

Relying on a foreign currency for local and international transactions can create vulnerabilities and limit the country’s ability to pursue its unique economic policies.

This enhanced autonomy enables the nation to respond effectively to economic challenges and tailor its policies to specific domestic needs, ultimately fostering sustainable development and inclusive growth.

What it All Means

The commitment to pursue a Zimbabwe single currency is not merely a financial transformation; it’s a testament to the nation’s commitment to economic growth and development.

The journey from hyperinflation to a multi-currency system and, now, towards a single currency signifies a remarkable transformation.

Zimbabwe’s economic landscape is undergoing a significant shift, and stakeholders eagerly await the fulfillment of this ongoing financial evolution.

As President Mnangagwa reiterates, “We want a single currency, and we are going there.”

SUPPORTING ARTICLES

The Chronicle: Zimbabwe to revert to local currency

The South African: Zimbabwe to reintroduce local currency

© Awake-In-3D | GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/breaking-news-a-zimbabwe-single-currency-is-now-on-track/

The Implications and Outcomes of an RV/GCR on the World: Awake-In-3D

Awake-In-3D: The Implications and Outcomes of an RV/GCR on the Entire World

The final chapter in the “The End of the Fiat Currency Debt System and the Financial Reset – A Complete Guide”

Now, we turn our attention toward gaining a clear view on the potential implications and outcomes of the transformative shift an RV/GCR would have in the global financial landscape.

“On a geopolitical scale, the adoption of a tangible asset-backed currency system will re-calibrate international power dynamics.

Nations with significant reserves of tangible assets will assume greater influence in the global financial arena, challenging the supremacy of traditional economic superpowers.”

Awake-In-3D: The Implications and Outcomes of an RV/GCR on the Entire World

The final chapter in the “The End of the Fiat Currency Debt System and the Financial Reset – A Complete Guide”

Now, we turn our attention toward gaining a clear view on the potential implications and outcomes of the transformative shift an RV/GCR would have in the global financial landscape.

“On a geopolitical scale, the adoption of a tangible asset-backed currency system will re-calibrate international power dynamics.

Nations with significant reserves of tangible assets will assume greater influence in the global financial arena, challenging the supremacy of traditional economic superpowers.”

The Implications and Outcomes of an RV/GCR on the World

On October 10, 2023 By Awake-In-3D

In GCR Roadmap: Level 3 Events, RV/GCR

Chapter 5 of The End of the Fiat Financial System and the Global Financial Reset – A Complete Guide

Now, we turn our attention toward gaining a clear view on the potential implications and outcomes of the transformative shift an RV/GCR would have in the global financial landscape.

In the preceding chapters, we have explored the rationale for a global financial reset and the practical aspects of transitioning to a tangible asset-backed currency system while safeguarding personal freedoms, financial privacy, and individual financial sovereignty.

On a geopolitical scale, the adoption of a tangible asset-backed currency system could re-calibrate international power dynamics. Nations with significant reserves of tangible assets will assume greater influence in the global financial arena, challenging the supremacy of traditional economic superpowers.

5.1 The Potential Benefits of Tangible Asset-Backed Currencies

Transitioning from fiat currencies to tangible asset-backed currencies holds the promise of several significant advantages for both individuals and nations.

These benefits underscore the importance of embracing a new financial paradigm.

5.1.1 Stability and Confidence

One of the primary benefits is enhanced stability and confidence in the financial system. Tangible assets, such as gold, have historically served as reliable stores of value.

By anchoring currencies in such assets, individuals and nations can have greater trust in the value and stability of their money.

Individuals and nations gain greater financial sovereignty in a tangible asset-backed currency system. The reliance on central banks for currency issuance and management diminishes, allowing for more control over financial matters while upholding individual financial privacy.

5.1.2 Protection Against Inflation

Tangible asset-backed currencies provide a hedge against inflation.

Unlike fiat currencies, which can be devalued through excessive printing, the intrinsic worth of tangible assets remains stable. This protection can safeguard the purchasing power of individuals and promote economic stability.

5.1.3 Financial Sovereignty

Individuals and nations gain greater financial sovereignty in a tangible asset-backed currency system.

The reliance on central banks for currency issuance and management diminishes, allowing for more control over financial matters while upholding individual financial privacy.

5.1.4 Equitable Global Trade

The transition promotes equitable global trade by leveling the playing field for nations with varying degrees of tangible assets.

Trade imbalances are reduced as exchange rates more accurately reflect the economic fundamentals of countries. This fosters fairer and more balanced international trade relationships.

5.2 Potential Concerns and Challenges

While the advantages are compelling, the transition to a tangible asset-backed currency system is not without its challenges and potential concerns.

Recognizing and addressing these issues is crucial to the success of this transformative shift.

The RV/GCR must strike the right balance between privacy rights and regulatory frameworks within the decentralized ledger system is essential.

5.2.1 Valuation and Asset Management

Determining the value of tangible assets, especially gold, can be complex and subject to market fluctuations in and RV/GCR landscape.

Ensuring accurate valuation and effective asset management within the Quantum Financial Network System (QFS) is a critical challenge.

5.2.2 Privacy and Oversight

Balancing the need for individual financial privacy with international oversight and accountability is a delicate task.

The RV/GCR must strike the right balance between privacy rights and regulatory frameworks within the decentralized ledger system is essential.

5.3 Conclusion

This chapter has provided insights into the potential benefits, concerns, and challenges associated with transitioning to a tangible asset-backed currency system or the RV/GCR.

On a geopolitical scale, the adoption of a tangible asset-backed currency system could re-calibrate international power dynamics. Nations with significant reserves of tangible assets will assume greater influence in the global financial arena, challenging the supremacy of traditional economic superpowers.

This change could lead to diplomatic realignments, the renegotiation of trade agreements, and a restructuring of international alliances.The geopolitical implications are multifaceted, with the potential to redefine the global economic order.

Final Thoughts on this RV/GCR Thesis: “The End of the Fiat Currency Debt System and the Financial Reset”

In this comprehensive thesis, we have explored the compelling case for a global financial reset and the revaluation of currencies backed by tangible assets.

Our journey has taken us through the inherent flaws and vulnerabilities of the existing fiat currency debt system, highlighting the urgent need for a fundamental shift.

We began by examining the logical conclusion of the fiat currency debt system, revealing unsustainable debt levels, inflationary pressures, market volatility, and central bank interventions. These factors collectively signal the system’s failure and necessitate a fresh approach.

The Global Currency Reset (GCR) emerged as the proposed solution, promising to replace the collapsed fiat currency system.

Underpinning the GCR is the Quantum Financial Network System (QFS), a technological marvel that leverages quantum computing, decentralized ledgers, blockchain technology, smart contracts, quantum encryption, global accessibility, and scalability.

Together, these elements form a financial infrastructure that prioritizes personal freedoms, financial privacy, and individual sovereignty.

Furthermore, we examined the revaluation of currencies (RV) within the GCR framework, emphasizing the need for purchasing power parity among global currencies.

A currency revaluation aims to address trade imbalances, correct unfair exchange rates, spur economic growth and development, and foster international collaboration.

As we embrace the voyage towards a global financial reset, it becomes evident that the QFS stands at the forefront of this transformative endeavor. Its innovative technologies and principles offer a pathway to a more transparent, secure, and efficient financial ecosystem.

The case for a global financial reset and a revaluation of currencies backed by tangible assets is rooted in the necessity to rectify the shortcomings of the existing system.

By embracing technological advancements like the QFS and prioritizing principles of fairness and transparency, we pave the way for a more equitable and prosperous global financial landscape.

An RV/GCR Thesis: The End of the Fiat Currency Debt System and the Financial Reset – A Complete Guide

GO TO CHAPTER 1: The Stage is Set for Our RV/GCR

GO TO CHAPTER 2: The Imperative for a Global Financial Reset (GCR)

GO TO CHAPTER 3: A Currency Revaluation (RV) with Tangible Asset Backing

GO TO CHAPTER 4: How Asset-backed Currencies will be Implemented on the QFS

GO TO THE SUPPLEMENT: A Technical Overview of the Quantum Financial Network System (QFS)

GO TO CHAPTER 5: The Implications and Outcomes of the RV/GCR

My primary thesis is that the Global Fiat Currency Debt System must come to its logical conclusion before Our GCR will be introduced – which includes the release of the “General Redemptions” funding for RV/GCR exchanges.

But how do you track the connected events and progress of the logical conclusion of the Fiat Financial System?

It’s easy when you follow my unique RV/GCR Roadmap right here at GCR Real-Time News

© Awake-In-3D | GCR Real-Time News

Ai3D Website: Ai3D.blog

Ai3D on Telegram: GCR_RealTimeNews

Ai3D on Twitter: @Real_AwakeIn3D

https://ai3d.blog/the-implications-and-outcomes-of-an-rv-gcr-on-the-world/

The QFS: An Overview of the Quantum Financial Network System

The QFS: An Overview of the Quantum Financial Network System

On October 10, 2023 By Awake-In-3D

A Supplement to The End of the Fiat Financial System and the Global Financial Reset – A Complete Guide

The Quantum Financial Network System (QFS) stands at the forefront of the proposed global financial reset, offering a quantum leap in financial technology. This sidebar provides a technical glimpse into the QFS, highlighting its core components and functionalities.

The QFS adopts a decentralized ledger system, which is fundamentally different from traditional centralized systems. Instead of relying on a single central authority to maintain and validate transactions, decentralized ledgers distribute this responsibility across a network of nodes.

The QFS: An Overview of the Quantum Financial Network System

On October 10, 2023 By Awake-In-3D

A Supplement to The End of the Fiat Financial System and the Global Financial Reset – A Complete Guide

The Quantum Financial Network System (QFS) stands at the forefront of the proposed global financial reset, offering a quantum leap in financial technology. This sidebar provides a technical glimpse into the QFS, highlighting its core components and functionalities.

The QFS adopts a decentralized ledger system, which is fundamentally different from traditional centralized systems. Instead of relying on a single central authority to maintain and validate transactions, decentralized ledgers distribute this responsibility across a network of nodes.

Quantum Computing Technology

At the heart of the QFS lies quantum computing, a groundbreaking technology that harnesses the principles of quantum mechanics.

Unlike classical computers that use binary bits (0s and 1s), quantum computers employ quantum bits or qubits.

This enables quantum computers to process vast amounts of data at unprecedented speeds, making them ideal for complex financial calculations and cryptographic operations.

Related article: Quantum computing networks for finance are real and being used today.

Decentralized Ledger System

The QFS adopts a decentralized ledger system, which is fundamentally different from traditional centralized systems.

Instead of relying on a single central authority to maintain and validate transactions, decentralized ledgers distribute this responsibility across a network of nodes.

This ensures transparency, security, and resilience, as no single entity can control or manipulate the system.

The Quantum Financial Network System represents a technological paradigm shift in the world of finance.

Blockchain Technology

Within the QFS, secure blockchain nodes facilitate transactions and record-keeping.

Blockchain technology ensures the integrity and immutability of financial data by storing information in interconnected blocks, cryptographically linked together.