5 Obstacles You Can Expect on Your Journey to Financial Freedom

5 Obstacles You Can Expect on Your Journey to Financial Freedom

By Denise Hill

The road to financial freedom is paved with good intentions — and littered with skid marks from those who started out, but opted for an easier path. It can be a lonely, winding road that has potholes, roadblocks, and detours. The best way to ensure any journey is successful is to properly prepare.

Here are a few pitfalls you can expect to run into on your way to financial freedom, and what you can do to cope.

5 Obstacles You Can Expect on Your Journey to Financial Freedom

By Denise Hill

The road to financial freedom is paved with good intentions — and littered with skid marks from those who started out, but opted for an easier path. It can be a lonely, winding road that has potholes, roadblocks, and detours. The best way to ensure any journey is successful is to properly prepare.

Here are a few pitfalls you can expect to run into on your way to financial freedom, and what you can do to cope.

1. You'll get tired

Living a life of frugality can be exhausting. Always pinching pennies, weighing options, tracking expenses, and telling yourself "no" can get old quick. Your ability to remain on the financial straight and narrow is directly proportional to your level of tolerance.

Some people can go months without new clothes, drive the same hoopty for years, take one vacation every decade, and be perfectly happy. Others cannot. Find a pace and intensity that fits your personality and level of discipline. Give yourself the wiggle room you need to succeed.

A great way to combat the fatigue that will pop up along your journey is to take breaks. Allow yourself the opportunity to relax and enjoy the view from time to time. Set financial goals that secure your future, but also keep you happy.

Plan to take a vacation, save up for a mini shopping spree, and blow a little cash every once in a while just hanging with friends. The key is to pace yourself. This journey is a marathon. (See also: Yes, You Need "Fun Money" in Your Budget)

2. You'll feel lonely

Forging a path toward financial freedom goes against the grain of our current society. You are bombarded with messages that tell you that you deserve the best no matter the cost. You are worth it. And you only live once, so you might as well live it up now. You are encouraged to indulge yourself.

Living a lifestyle contrary to the popular consensus can be extremely lonely. It can be hard to find people who support your money management value system. And not having someone you can talk to and who understands the dilemmas that come with financial freedom can leave you feeling isolated. You may even find yourself tempted to abort your mission and follow the crowd.

Before you give up and join the ranks of the financially irresponsible, consider this — you are not alone. There are others like you out there. If you're surrounded by those who do not share your passion for financial independence, you must look for those who do.

To continue reading, please go to the original article here:

http://www.wisebread.com/5-obstacles-you-can-expect-on-your-journey-to-financial-freedom

How Our Perceptions of Time and Money Change as We Age

How Our Perceptions of Time and Money Change as We Age

BY RETIRE BEFORE DAD

Our perceptions of the value of time and money shift as we age. In early adulthood, time is abundant, while money is scarcer. We want more money and are willing to sacrifice our time to get it.

By middle age, a thriving career helps us earn more, but job and family obligations consume our time. Life is expensive, and working middle-aged people never seem to have enough time or money.

Approaching retirement, we’re more willing to spend money to save time. Why mow the lawn when you could be playing golf or Bridge? And what good is all that wealth if we have no time to enjoy it?

How Our Perceptions of Time and Money Change as We Age

BY RETIRE BEFORE DAD

Our perceptions of the value of time and money shift as we age. In early adulthood, time is abundant, while money is scarcer. We want more money and are willing to sacrifice our time to get it.

By middle age, a thriving career helps us earn more, but job and family obligations consume our time. Life is expensive, and working middle-aged people never seem to have enough time or money.

Approaching retirement, we’re more willing to spend money to save time. Why mow the lawn when you could be playing golf or Bridge? And what good is all that wealth if we have no time to enjoy it?

Time was valuable all along.

But as we age and grow wealth, we learn to appreciate time more because we have less of it to live.

The sooner we learn, the sooner we can shift our focus to what’s most important.

Important of time vs. importance of money chart.

The crossover point — when we fully embrace time as the superior resource and prioritize accordingly — is realized at different stages of life for different people.

It may be gradual or sudden.

The approach to retirement is a typical time when priorities shift.

Does retirement change our perception of the value of money?

The standard path of attaining an expensive education and then working full-time for the next four decades to retire at 65 is still predominant.

But that’s Baby Boomer gold-watch thinking.

We have more options.

Time vs. money purpose?

Maybe when we find our true purpose in life, we modify priorities to elevate the importance of time, relationships, and our impact on the world over income and wealth.

For those with a clearly defined purpose, time spent not fulfilling that purpose is wasted time.

There can be prosperity in purpose. Finding work you love that serves others and makes you wealthy might be the holy grail.

Diagnosis as the cross over point.

A serious health diagnosis, accident, or death of a loved one might change your feelings about time and money too.

Imagine a doctor telling you there are only a few months left to live.

Life’s priorities would shift immediately.

To continue reading, please go to the original article here:

Type I and Type II Charlatans

Type I and Type II Charlatans

Posted December 27, 2020 by Ben Carlson

Pockets of the market are flirting with silly territory.

SPACs, IPOs, and electric vehicle companies are all sprouting up like weeds.

I’m not intelligent enough to sort through the winners and losers in these areas but the fact that there are currently winners means there will be a flood of losers to follow. That’s how these things work. When speculative investments are in demand, the supply ramps up to meet it.

And many of those losers will be pushed relentlessly by hucksters and charlatans who flock to rising markets like me to a new Tom Cruise movie.

Type I and Type II Charlatans

Posted December 27, 2020 by Ben Carlson

Pockets of the market are flirting with silly territory.

SPACs, IPOs, and electric vehicle companies are all sprouting up like weeds.

I’m not intelligent enough to sort through the winners and losers in these areas but the fact that there are currently winners means there will be a flood of losers to follow. That’s how these things work. When speculative investments are in demand, the supply ramps up to meet it.

And many of those losers will be pushed relentlessly by hucksters and charlatans who flock to rising markets like me to a new Tom Cruise movie.

Charlatans tend to flourish when some or all of the following characteristics are present:

When there’s an “expert” with a good story

When greed is abundant

When capital becomes blind to risk

When individuals begin taking their cues from the crowd

When markets are rocking

When innovation runs rampant

There are two types of charlatans you need to watch out for when trying to avoid getting taken advantage of during these types of market environments.

When testing a hypothesis using statistics, there are two types of errors a statistician can make. A type I error is when you reject a null hypothesis that is actually true. A type II error is when you accept a null hypothesis that is actually false.

This meme is the best explanation of this concept I seen:

Type I charlatans are the visionaries who are more or less sincere but wind up ruining their investors anyway because they take their ideas to the extreme or fail to account for the unintended consequences of their ideas.

These false-positive charlatans are so passionate that it becomes difficult for their victims to see any downside. When you combine intellect, passion, and people in search of money and/or power, it’s easy to become blinded to potential risks.

And once a Type I charlatan gets a taste of success, it’s tough to pull in the reins when things go wrong.

To continue reading, please go to the original article here:

https://awealthofcommonsense.com/2020/12/type-i-and-type-ii-charlatans/

The Golden Age of Fraud is Upon Us

.The Golden Age of Fraud is Upon Us

Posted April 27, 2021 by Ben Carlson

A 30-something low-level actor created a business plan that would buy the rights to cheap movies and turn around and sell those rights to HBO for audiences in Latin America. The investors backing the project were promised returns of 15% in just 6 months. No bad in an era of 0.25% savings account yields. Investors forked over more than $690 million to bankroll the rights to these films.

So what’s the catch? The movie contracts with HBO were fakes, the business plan was a hoax and the entire ordeal was a Ponzi scheme where new money paid off previous investors. The money was used to provide a lavish lifestyle for the architect of the fraud, Zachary Horowitz.1

The Golden Age of Fraud is Upon Us

Posted April 27, 2021 by Ben Carlson

A 30-something low-level actor created a business plan that would buy the rights to cheap movies and turn around and sell those rights to HBO for audiences in Latin America. The investors backing the project were promised returns of 15% in just 6 months. No bad in an era of 0.25% savings account yields. Investors forked over more than $690 million to bankroll the rights to these films.

So what’s the catch? The movie contracts with HBO were fakes, the business plan was a hoax and the entire ordeal was a Ponzi scheme where new money paid off previous investors. The money was used to provide a lavish lifestyle for the architect of the fraud, Zachary Horowitz.1

One investor claimed to have “99% of his and his family’s money” invested in Horowitz’s scheme.

*******

Thodex is a cryptocurrency trading platform in Turkey. Last week it was reported the 27-year-old founder of the exchange took a flight to Albania.

He took with him $2 billion from more than 30k clients.

Last month the company brought in hoards of new clients by offering free dogecoin to anyone that signed up.

Whoops.

*******

I don’t know if this SCAMcoin actually happened or if it’s just a social media thing but it wouldn’t surprise me if it’s real: https://twitter.com/i/status/1385365742506364929

If Charles Ponzi were alive today, I have no doubt that he would be able to raise capital from investors, probably in the form of a SPAC. Many investors would laud him for being a genius as he bilked investors out of millions of dollars.

When I was researching the history of financial scams for Don’t Fall For It the one thing that jumped out above all else is how similar financial frauds are across time and place. They typically involve new technologies, people with extraordinary sales skills and the insatiable human desire for get-rich quick schemes.

Despite the fact that people have been getting duped by hucksters and charlatans for centuries, there was one period that kept coming up over and over again in my research — the 1920s.

It was the golden age of financial fraud.

The Roaring 20s had everything a con-artist looking to dupe people out of their money could ask for — innovation, new financial products, a booming economy, rising markets, new and exciting technologies, loose lending standards, new communication tools and people getting rich all over the place.

To continue reading, please go to the original article here:

https://awealthofcommonsense.com/2021/04/the-golden-age-of-fraud-is-upon-us/

The Art of Money - Turning Financial Success Into A Creative Pursuit

.The Art of Money - Turning Financial Success Into A Creative Pursuit

Jacob Schroeder

What do you consider the act of ‘making money’? Is it an act of accounting and measuring? Or, is it an act of imagining and contemplating? Our finances involve numbers and data, but they’re intractably tied to our personal ideas, experiences, feelings and behaviors – intangible things you can’t formulate in a spreadsheet. Therefore, to manage the human side of money, it’s better to think more like an artist than a scientist. It’s a shame many famous artists had financial troubles.

Johannes Vermeer is said to have left behind 10 young children, a house full of paintings no one wanted and enormous debts, causing his wife to declare bankruptcy.

The Art of Money - Turning Financial Success Into A Creative Pursuit

Jacob Schroeder

What do you consider the act of ‘making money’? Is it an act of accounting and measuring? Or, is it an act of imagining and contemplating? Our finances involve numbers and data, but they’re intractably tied to our personal ideas, experiences, feelings and behaviors – intangible things you can’t formulate in a spreadsheet. Therefore, to manage the human side of money, it’s better to think more like an artist than a scientist. It’s a shame many famous artists had financial troubles.

Johannes Vermeer is said to have left behind 10 young children, a house full of paintings no one wanted and enormous debts, causing his wife to declare bankruptcy.

Mozart wracked up massive amounts of debt, too, to feed an extravagant lifestyle. Not to be out done, Oscar Wilde lived far beyond his means, until he eventually fell into poverty and supposedly spent his last bit of money on booze. When he took his own life, Vincent van Gogh was poor and destitute.

It’s a shame, because some principles great artists follow to make art could also apply to making money.

Art and money share more similarities than we like to think. Money, like art, is a means of self-expression; it helps you turn the life you imagine into reality. They’re both deeply personal. There is no one right way to sculpt a Greek goddess or invest in stocks. Most of all, money offers a lot of insights into human behaviors and sensations.

It is often those human elements that lead to financial problems, but that also give our financial decisions meaning. Therefore, when trying to create a financially successful future, we may need a little more right-brain than left-brain thinking.

Take it from Andy Warhol, an artist who loved to blur the lines of commerce and culture, who declared:

“Making money is art and working is art and good business is the best art.” Andy Warhol

Why it helps to think of money as more art than science

Is personal finance an art or a science?

The juncture of art and money has gotten most attention as it relates to investing. Investor Howard Marks said: “Investing, like economics, is more art than science.”

Why?

Investing encapsulates the vagaries of human nature in the face of uncertainty. There is an element of personal intuition that guides the algorithms. That element of variance and uncertainty is what Barry Ritholtz expands upon in his definition:

“Investing is the art of using imperfect information to make probabilistic assessments about an inherently unknowable future.”

To continue reading, please go to the original article here:

How to Prepare For a Recession

How to Prepare For a Recession

Posted March 17, 2022 by Ben Carlson

A reader asks: What are some moves you’re making to prepare for the recession?

There seems to be a growing consensus among smart people I follow right now:

Inflation was already high and is only going to get worse because of the war. We could easily see a 10% inflation print this year.

The war is going to cause massive food shortages in the next year since so many agricultural commodities come from Ukraine and Russia.

Supply shocks were already bad and are only going to get worse. Tack on China’s Covid outbreak that’s shutting down entire cities and the supply chain is in trouble yet again.

Therefore, a recession is now inevitable.

How to Prepare For a Recession

Posted March 17, 2022 by Ben Carlson

A reader asks: What are some moves you’re making to prepare for the recession?

There seems to be a growing consensus among smart people I follow right now:

Inflation was already high and is only going to get worse because of the war. We could easily see a 10% inflation print this year.

The war is going to cause massive food shortages in the next year since so many agricultural commodities come from Ukraine and Russia.

Supply shocks were already bad and are only going to get worse. Tack on China’s Covid outbreak that’s shutting down entire cities and the supply chain is in trouble yet again.

Therefore, a recession is now inevitable.

Last week I even hopped on this bandwagon by showing how a recession is the only way we’ve seen high inflation fall in the past.

I do believe the probability of a recession is higher now than it was a month ago.

However, when dealing with probabilities, you have to look at both sides of the argument. Nothing is 100% certain in the markets or the economy.

Let’s look at the other side of this argument to show what could keep us out of a recession for a while longer.

There is a ton of pent-up demand.

Delta’s CEO said the airline just had its busiest two days in history in terms of sales. Travel spending is booming right now.

I was at Disney last month. The parks were packed every single day. My Disney insiders tell me they think sometime in March could see the busiest week ever for their theme parks. And I know from experience — Disney is not cheap. Inflation is not holding back spending at the parks.

The housing market remains scalding hot, even in the face of rising mortgage rates. Logan Motashami posted this picture of people lined up down the street waiting to see a new listing in California last weekend:

This is not exactly recessionary behavior.

To be fair, these are just anecdotes. How about some data?

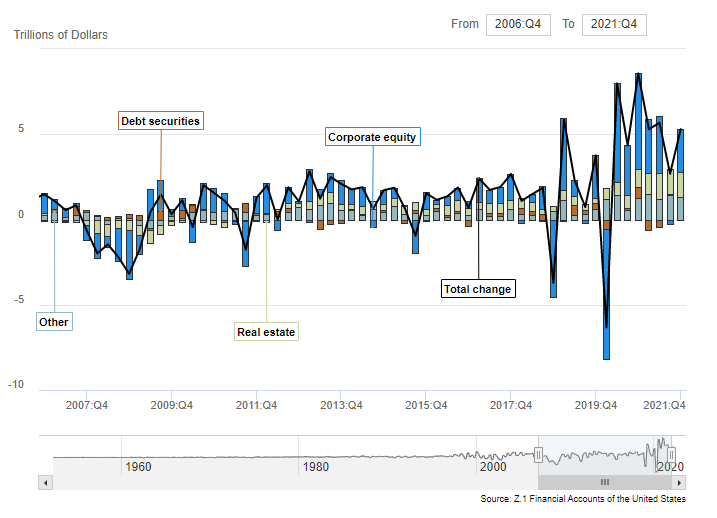

Each quarter, the Federal Reserve releases a report on household wealth. Last year saw the largest increase in household net worth ever: LINK

U.S. household net worth surged almost $19 trillion in 2021. Real estate alone accounted for more than $5 trillion of gains.

Households have never been wealthier.

So on the one hand, rising prices could cause consumers to rein in their spending on certain products and services.

On the other hand, inflation has only been above trend since last April. Consumers have been saving and paying down debt for two years. It’s certainly possible U.S. households will complain about inflation but then go into debt and spend down their savings to make up for higher prices.

That could certainly extend the expansion.

Both arguments have their merits.

So we could go into a recession this year or next year or four years from now.

I honestly have no idea.

All I know is we will have a recession at some point.

Since World War II, we’ve had 13 recessions in the United States:

{kind=link}

This means that over the past 80 years or so, a recession has occurred once every 5.9 years on average.

Now, recessions don’t run on a train schedule. Sometimes they happen in quick succession (like the 1950s or early-1980s) and sometimes they are few and far between (like the 1990s or 2010s).

The way I look at it is you’re not preparing for THE recession but a recession. There is a difference.

To continue reading, please go to the original article here:

https://awealthofcommonsense.com/2022/03/how-to-prepare-for-a-recession/

How to Create Wealth During a Recession

How to Create Wealth During a Recession

July 2022 Financial Imaginer

There’s no time like the present to create wealth. Most wealthy people know that it’s during difficult times when possibilities for building wealth abound. So if you’re looking to create some serious financial stability for yourself and your loved ones, don’t wait – don’t let this crisis go to waste – start now. Learn how to create wealth during a recession with the following 8 tips.

1. Never let a Crisis go to Waste.

How to Create Wealth during a Recession

July 2022 Financial Imaginer

There’s no time like the present to create wealth. Most wealthy people know that it’s during difficult times when possibilities for building wealth abound. So if you’re looking to create some serious financial stability for yourself and your loved ones, don’t wait – don’t let this crisis go to waste – start now. Learn how to create wealth during a recession with the following 8 tips.

1. Never let a Crisis go to Waste.

When it comes to creating wealth, there’s no such thing as a bad time – only good opportunities disguised as bad times. So instead of being afraid of a recession, use it as an opportunity to create wealth. Change your goggles, instead of using your fear glasses, look for opportunities!

Adapt your mindset, and understand Mad Wallstreet.

2. Get Creative with Your Investments

Wealth creation is all about thinking outside the box. If you want to create wealth during a recession, you have to be creative and think differently than “the rest of us“.

The building blocks of your [financial] life.

But don’t worry, there are plenty of ways to create wealth without putting your life savings at risk. For example, you could start a business or invest in real estate, another way is by investing in distressed assets. This could be anything from a house that’s in foreclosure to a business that’s about to go bankrupt. Of course, you need to be careful with these kinds of investments, but if you do your homework, you could see some serious opportunities during a recession.

You can also get creative with more traditional investments, like stocks and bonds. For example, you could invest in companies that are doing well despite the recession. The high percentage of passive investing results in more generic sell-offs of everything and stock pickers might find stocks at undeservedly low levels.

Another option is to start your own business. Many people lose their jobs during a recession, but if you have an entrepreneurial spirit, this could be the perfect time to turn your ideas into reality and pivor into a new life altogether. There are many resources available to help you get started, so there’s no excuse not to at least try.

What’s the worst that could happen?

To continue reading, please go to the original article here:

https://www.financial-imagineer.com/how-to-create-wealth-during-a-recession/

Based on a True Story

Based on a True Story

Notes From the Field By Simon Black November 11, 2022

More than 3,000 years ago, between the 12th and 13th centuries BC, the legendary king of Ithaca, Odysseus, set sail from the ancient city of Troy to begin the journey home.

The stories of the Trojan War, and of Odysseus’s voyage home, have been passed down to us in the form of epic poetry from Homer. Most of it is pure fiction. But like modern film, TV, and ‘true crime’ podcasts that abuse dramatic license to entertain their audiences, Homer’s epics may in fact be “based on a true story”.

Based on a True Story

Notes From the Field By Simon Black November 11, 2022

More than 3,000 years ago, between the 12th and 13th centuries BC, the legendary king of Ithaca, Odysseus, set sail from the ancient city of Troy to begin the journey home.

The stories of the Trojan War, and of Odysseus’s voyage home, have been passed down to us in the form of epic poetry from Homer. Most of it is pure fiction. But like modern film, TV, and ‘true crime’ podcasts that abuse dramatic license to entertain their audiences, Homer’s epics may in fact be “based on a true story”.

The Trojan War, for example, likely happened. The bit about the horse, on the other hand, probably didn’t.

It’s certainly possible (and even probably) that one of the key leaders in the war had an arduous journey back home to Greece, spurring ancient entertainers to weave elaborate tales of sirens and sea monsters.

One of the most important parables in Homer’s tale of the long journey home for Odysseus is the story of Scylla and Charybdis.

Odysseus’s journey took him through a particularly narrow stretch of sea; on one side of the strait was a small, rocky island where a six-headed monster named Scylla lay waiting to destroy any ship that dared to pass.

According to Homer, Scylla was such a dreadful monster that “no one-- not even a god-- could face her without being terror-struck.”

But on the other side of the narrow strait was the deadly whirlpool of Charybdis, which would swallow up the entire vessel and all the men on it.

Odysseus’s impossible task, of course, was to swiftly and stealthily sail right down the middle… to just barely avoid the whirlpool of Charybdis, while somehow managing to avoid the long grasp of Scylla.

For a while, Odysseus refused to believe the situation was hopeless; he was convinced that he would be able to sail, unscathed, between Scylla and Charybdis without a single loss.

After all, he was a king. And an unparalleled expert when it came to sailing. Surely he would be able to succeed.

And yet everyone who had ever come before Odysseus had believed the same thing. But no one had ever succeeded. Literally every ship that ever tried to sail between Scylla and Charybdis had been destroyed by one of the two evils.

Eventually reality set in, and Odysseus knew that had would have to choose between the lesser of the two evils.

He chose the monster Scylla.

Odyssesus realized that sailing too close to the whirlpool would mean losing his entire ship and everyone on it. Sailing too close to the 6-headed monster would mean losing, at most, six men.

Odysseus concluded that it was better to lose six men was than to lose everyone.

And that’s precisely what happened; as his ship sailed through the strait, just barely avoiding the whirlpool, “Scylla pounced down suddenly upon us and snatched up six of my best men.”

But the rest of the crew (and the ship) survived the challenge and passed through the strait.

This story is one of the best allegories of the state of the global economy today.

Central bankers and economic policymakers are like Odysseus. They have managed to sail the global economy into a very narrow strait.

On one side of today’s economic strait is the evil inflation monster. And this monster is guaranteed to chew up and spit out incalculable quantities of unsuspecting, unprepared people.

Yet on the other side of the economic strait is the full-blown collapse of the sovereign bond markets… and by extension, collapse of the global financial system.

Like Odysseus, central bankers were at first in denial. They didn’t want to believe they were even in such dire economic straits. They infamously rejected the notion that inflation existed at all. Then they claimed it was transitory.

Then they finally started trying to do something about it-- to turn the ship around. But it was too little, too late.

Now they find themselves squarely in the middle of these evils-- inflation, and collapse of the sovereign bond market. And they’ll be forced to choose between the lesser of the two evils.

Inflation is, by far, the lesser evil.

The US national debt has doubled in the past decade, to $31 trillion. It will almost certainly double in the next decade, especially considering the massive $15+ trillion Social Security bailout that will be necessary by 2032.

The US government already spent $680 billion last fiscal year just to pay interest. And that was with record low interest rates.

Central bankers have been raising rates rapidly this year. But continuing to do so will bankrupt the Treasury.

Remember that the US government has to refinance roughly 20% of its debt every year. Now that interest rates are so much higher, the government’s total interest payments will soon soar past $1 trillion, then $2 trillion annually.

This would be devastating to national finances and potentially force a default. Central bankers know this, which is why they prefer to let inflation reign rather than risk a sovereign default.

The government announced earlier this week that inflation had decreased to ‘only’ 7.7%. Don’t be fooled; inflation is still very much the major economic story of our time.

This is the story of our podcast today-- how central bankers find themselves between Scylla and Charybdis.

This podcast was actually a live recording, taken today at our Total Access event in Mexico City.

We’ll discuss why there are many forces that will continue to push prices higher for years to come, why the central banks are powerless to do anything about it, and how you can still take back control.

You can listen in here.

To your freedom, Simon Black, Founder Sovereign Research & Advisory

https://www.sovereignman.com/podcast/based-on-a-true-story-144241/

Three Global Cities Where You Can Still Beat Inflation

Three Global Cities Where You Can Still Beat Inflation

Notes From the Field By Simon Black November 8, 2022

Inflation is undoubtedly one of the biggest stories of our time.

It’s a story of abject failure — of how the ‘experts’ who have been entrusted to pull the giant levers of the economy were asleep at the wheel. The ‘experts’ failed to anticipate how their irresponsible spree of spending and monetary expansion would create inflation. They failed to notice it. They failed to do anything about it in a timely manner.

And now that central bankers have switched to this new HAIR ON FIRE, ULTRA-PANICKY monetary policy, they’re failing to instill even a modicum of confidence in the future.

Three Global Cities Where You Can Still Beat Inflation

Notes From the Field By Simon Black November 8, 2022

Inflation is undoubtedly one of the biggest stories of our time.

It’s a story of abject failure — of how the ‘experts’ who have been entrusted to pull the giant levers of the economy were asleep at the wheel. The ‘experts’ failed to anticipate how their irresponsible spree of spending and monetary expansion would create inflation. They failed to notice it. They failed to do anything about it in a timely manner.

And now that central bankers have switched to this new HAIR ON FIRE, ULTRA-PANICKY monetary policy, they’re failing to instill even a modicum of confidence in the future.

These people don’t have any real solutions. The central bankers themselves have admitted publicly that their maniacal interest rate hikes will have zero impact on bringing down food prices, gasoline prices, or fixing supply chain challenges.

Meanwhile the politicians who helped light this inflation blaze by dumping trillions of dollars into the economy want to ‘fix’ the problem by... dumping more money into the economy. It’s genius!

Certainly a lot of people are holding out hope that today’s election results will help arrest the destruction.

And hope is great. But it’s not a Plan B, let alone a Plan A.

There are different ways of dealing with inflation, ranging from smarter places to park your savings, moving your investment allocation to real assets, small-scale food production, and much more.

Another way, at least for people who have the ability to do so, is living in a place where your money goes much, much further than back in your home country.

And today I asked my team to outline a few picks — cities that are still bargains in terms of cost of living and have the added benefit of being major global travel hubs. This works great for digital nomads, or semi-retirees who are still on the go.

Mexico City, Mexico

Juarez International Airport (MEX) is the most connected airport in the world outside of the US in 2022, according to OAG, a global travel data firm.

It offers direct flights as far away as Seoul, Korea, and Tokyo, Japan. In Europe, it offers flights directly to London, Paris, Madrid, Barcelona, Amsterdam, Frankfurt, and Munich.

And of course it offers direct flights to destinations all across the United States, and into South America, including Santiago, Chile, São Paulo, Brazil, and Buenos Aires, Argentina.

Mexico City is becoming popular among digital nomads and remote workers because it offers all the amenities of the world-class mega-city it is, for a fraction of the cost of Paris, Tokyo, or New York City.

Mexico has not seen the same supply chain problems as most of the rest of the world. It didn’t destroy its economy during COVID, and the Mexican peso has remained relatively strong.

Still, Mexico is a very inexpensive place to live. Even in Mexico City, one of the most expensive places in Mexico, a single person could live comfortably on about $1,900 per month (for everything — rent, food, entertainment, etc.).

And once you visit Mexico City, you realize what incredible value it offers. It is beautiful, bursting with parks, and overflowing with cultural attractions, museums, and events.

In Polanco, one of the nicest neighborhoods that is also popular with expats, there is free public WiFi throughout the entire community.

The median download internet speed in Mexico City is about 60 Mbps, according to speedtest.net. That speed can easily handle streaming and online gaming.

BUT Mexico City is huge, and this median speed doesn’t tell the whole story...

For example, Sovereign Research CEO Viktorija, who lives in Mexico City, reports download speeds of 1000 Mbps on fiber optic internet. But she pays close to $80 per month (including phone/TV too), which is considered expensive for Mexico City.

Mexico City in general has an easy-going, laid back vibe. You won’t find rabid, woke mobsters accosting you outside of restaurants here.

Mexico also has an easy residency process. You only have to earn about $2,500 per month, OR have about $35,000 in savings to show sufficient financial independence for temporary residency.

Retirees can skip right to permanent residency, which is truly permanent; it never has to be renewed.

They must show investments or bank balances of about $145,000 OR a pension equivalent to about $3,600 per month.

Cancun also deserves an honorable mention.

Its international airport (CUN) offers flights direct to more US and European cities than MEX, and can take you directly as far as Istanbul.

Cancun is not just for tourists. It is an incredibly affordable place to live on amazing beaches.

Very nice rentals start at about $2,000 per month for houses, and about $1,500 for spacious condos.

For example, one 2-bedroom 3-bathroom waterfront condo near the desirable Hotel Zone is asking just $1,650 per month.

Istanbul, Turkey

Istanbul International Airport (IST) offers direct flights to over 300 cities around the globe.

Istanbul, in many ways, is truly at the center of the world. From there you can fly direct to any continent except Australia and Antarctica.

This includes destinations as far away as Los Angeles, Mexico City, São Paulo, Tokyo, and Singapore.

And of course, Turkey is extremely well connected to Europe.

Istanbul is even less expensive than Mexico City. A single person could live comfortably on $1,200 per month.

But in addition, the dollar is currently very strong against the rapidly inflating Turkish lira. That means you can get even more for your money.

Istanbul’s median internet download speed is around 37 Mbps, and the city provides free WiFi hotspots in certain areas.

Another major benefit of Turkey is its economic citizenship program. You can buy citizenship and a second passport for a $400,000 investment in real estate.

For the right person, this is quite compelling. While other citizenship by investment programs require you to buy specific real estate which is generally overpriced, ANY property over $400,000 in Turkey qualifies.

That could, for example, land you a 3-bed 2-bath private villa with a pool and ocean views less than an hour from the airport. Or a sleek, modern 3-bed 2-bath condo in the city center.

Istanbul could become your base of operation to travel the world. And when you aren’t there, you could rent out your real estate to generate income.

Bangkok, Thailand

Suvarnabhumi Airport (BKK) on the outskirts of Bangkok offers direct flights to 108 destinations.

You won’t find many direct flights to the Americas. But its a great option to connect directly to Asia, Australia, and most of Europe.

Bangkok’s internet is excellent, with median download speeds around 218 Mbps.

While Bangkok is a bit more expensive than Mexico City and Istanbul, a single person could still live well on less than $2,200 per month.

And in addition to the low cost of living, Bangkok offers access to high quality inexpensive healthcare.

Any medical process you could want is available in Thailand, from an executive exam checkup to heart bypass surgery (which generally costs about one fifth of the $100,000 US price tag).

Bumrungrad International Hospital feels more like going to a luxury hotel than a hospital. Plus the majority of its doctors have received training in the US.

These are some of the best connected global travel hubs with a low cost of living. But that doesn’t mean they are your only options to stay connected.

Are you willing to endure one more leg to Lisbon, for example, in order to have the benefits of Portugal?

That is for you to decide. You can explore all your options, with various criteria, in one place with our Global Explorer map.

To your freedom, Simon Black, Founder Sovereign Research & Advisory

https://www.sovereignman.com/trends/three-global-cities-where-you-can-still-beat-inflation-144095/

Lottery Win Fail

Lottery Win Fail

March 2022 Matt Financial Imaginer

What started as an attempt to teach my kids a financial lesson about why playing the lottery is a bad idea backfired soon – we experienced a lottery win fail! While shopping we saw a huge digital billboard promoting how “nobody makes more millionaires” than the lottery company. Of course, I couldn’t let that sit with the kids and started to explain how most people lose their money attempting to get rich. Then the billboard went to show how the jackpot swelled to almost 40 million dollars.

A very tempting number indeed.

Lottery Win Fail

March 2022 Matt Financial Imaginer

What started as an attempt to teach my kids a financial lesson about why playing the lottery is a bad idea backfired soon – we experienced a lottery win fail! While shopping we saw a huge digital billboard promoting how “nobody makes more millionaires” than the lottery company. Of course, I couldn’t let that sit with the kids and started to explain how most people lose their money attempting to get rich. Then the billboard went to show how the jackpot swelled to almost 40 million dollars.

A very tempting number indeed.

As you can imagine, before any further conversation could happen, we got ourselves covered and played. I kept talking about how we will leave empty-handed from this experience. My daughter, age 8, played two sets of numbers for around $5. This seemed to be a reasonable price to let her experience “the feeling of losing”.

Or so I thought…

…this endeavour ended in a so-called lottery-win-fail!

I wanted to teach her the following lessons:

Get-rich-quick schemes are for the lazy and unambitious.

Respect your dreams enough to pay the full price for them.

What happened next was crazy.

For the first time in decades, we watched the lottery number drawing live on TV together. Since I didn’t expect anything particular to happen at that moment, my focus was not really on the TV at first. However, to my amazement, my daughter seemed to have three numbers out of six correctly, plus she got the extra number right which should pay her around $30.

Oh yay! Oh joy!

But now what happened to my lesson about how playing the lottery is a bad idea?

Well, wait for it.

The next day we went back to the shop to cash-in our gain.

While handing the lottery slip to the cashier, I said in a happy voice my daughter, who was next to me, seemed to have won $30.

The cashier denied it.

She explained: “Your daughter did NOT win $30.”

Our faces paled out.

Then she continued: “Actually she almost won $200 Sir! Your daugher got four numbers plus the extra one correct.”

My daughter looked puzzled. So did I. But then I realized my focus was truly not on playing the lottery and the cashier was right, we did have 4 plus 1 correct. And the cashiers’ screen showed “amount to be paid CHF 189.30”.

She was so excited and kept repeating how we were going to be even richer now as we figured out how to win the lottery. I quickly realized that it would take more than just a short conversation to explain the whole range of emotions and implications further to my daughter.

I realized this has been coined a “memory for life experience” and I’ve lost my original lesson about “playing the lottery is bad and useless”.

What a lottery-win-fail!!!

Next, I had to quickly deliver some new take-aways and teachables to keep the value of this financial excursion as originally intended.

On the way home, we started talking about what playing the lottery does to people. How lottery tickets are granting permission to dream of another, maybe a better life, how they enlighten hope, positive and negative emotions, joy and disappointment, we went through all these “stages” in the past 24 hours together.

My next thought was, how to teach her wealth from get-rich-quick schemes usually quickly disappears while wealth from hard work grows over time!

To continue reading, please go to the original article here:

Playing the Game of Life: Comparing Life to Video Games

Playing the Game of Life: Comparing Life to Video Games

November 2022 Financial Imaginer Matt

In life, we all want to win. We all want to achieve our goals and be successful. But what does it take to win the game of life? In this blog post, we will explore the concept of how to play the game of life like a video game!

Just like in video games, in life, you can become whoever you want to be, look however you want, and upgrade yourself as you see fit. The beauty of playing video games is that you can play as many lives as you want, and enter into as many different worlds as you please. In real life, you just got 1 Up!

“Video game players are artists who create their own reality within the game.”― Shigeru Miyamoto

Who says you can’t do so in your own life?

Playing the Game of Life: Comparing Life to Video Games

November 2022 Financial Imaginer Matt

In life, we all want to win. We all want to achieve our goals and be successful. But what does it take to win the game of life? In this blog post, we will explore the concept of how to play the game of life like a video game!

Just like in video games, in life, you can become whoever you want to be, look however you want, and upgrade yourself as you see fit. The beauty of playing video games is that you can play as many lives as you want, and enter into as many different worlds as you please. In real life, you just got 1 Up!

“Video game players are artists who create their own reality within the game.”― Shigeru Miyamoto

Who says you can’t do so in your own life?

Take a break, watch and listen to this awesome track! Have fun and let’s gooo!

https://www.youtube.com/watch?v=SK4Di2o-D54

Start thinking of life as a game – you’ll become fearless and start leveling up!

Join me [financially] imagineering your own life!

Are you Ready Player One?

“My friend Kira always said that life is like an extremely difficult, horribly unbalanced videogame. When you’re born, you’re given a randomly generated character, with a randomly determined name, race, face, and social class. Your body is your avatar, and you spawn in a random geographic location, at a random moment in human history, surrounded by a random group of people, and then you have to try to survive for as long as you can. Sometimes the game might seem easy. Even fun. Other times it might be so difficult you want to give up and quit.

But unfortunately, in this game you only get one life. When your body grows too hungry or thirsty or ill or injured or old, your health meter runs out and then it’s Game Over. Some people play the game for a hundred years without ever figuring out that it’s a game, or that there is a way to win it.

To win the videogame of life, you just have to try to make the experience of being forced to play it as pleasant as possible, for yourself, and for all of the other players you encounter in your travels. Kira says that if everyone played the game to win, it’d be a lot more fun for everyone.”

― Anorak’s Almanac, Chapter 77, Verses 11-20, Ready Player One

Let's play the game of life like a video game!

The Game of Life – Level 1: The Trial Run

To win the game of life, you must level up. Just like in any video game, to progress to the next level, you must complete certain tasks and challenges and grow stronger with experience.

Level 1: Let's go!

Let’s a gooo!

You must first learn and experience as much as possible. Growing up and school is a great place to start – it’s like the tutorial level of the game of life. Here, you familiarize yourself with the game, get to know the main character (yes, that would be your good self), and learn how to jump, run, survive, collect coin and hopefully how to learn!

“I think that inside every adult is the heart of a child. We just gradually convince ourselves that we have to act more like adults.” ― Shigeru Miyamoto

Learn how to navigate different environments, other characters, your surroundings, and what your superpowers are.

Embrace this trial run, learn fast, and grow!

Play the game of life like a video game.

Are you ready for the next level?

To continue reading, please go to the original article here: