Thank you to all the subscribers to our Early Access program…we thank you for your continued support.

We are excited to offer this new service to keep you informed and up-to-date on the latest Dinar and currency news.

The Biggest Winners Of This War Don't Pump A Single Barrel

The Biggest Winners Of This War Don't Pump A Single Barrel

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 28, 2026

How much do you think it would cost to send a supertanker, one of the giant ships that move the world's crude oil, through a narrow stretch of water that is full of mines, where missiles hit two tankers in early July, and where a crew member has already been killed?

Last month, one shipowner agreed to make that run— through the Strait of Hormuz— for nearly $470,000 per day.

The Biggest Winners Of This War Don't Pump A Single Barrel

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 28, 2026

How much do you think it would cost to send a supertanker, one of the giant ships that move the world's crude oil, through a narrow stretch of water that is full of mines, where missiles hit two tankers in early July, and where a crew member has already been killed?

Last month, one shipowner agreed to make that run— through the Strait of Hormuz— for nearly $470,000 per day.

For perspective, in the first few months of last year, before the war, the biggest crude tankers on earth were earning as little as $36,000 a day.

The ships collecting these fortunes don't produce anything at all. They don't pump oil, they don't refine it, and they don't sell it. They just carry it from one place to another.

And that is exactly why they have become the biggest winners of this war.

When Iran effectively closed the Strait of Hormuz in late February, oil spiked to $120 a barrel in March, then calmed as ceasefires came and went. But all the while, tanker rates just kept climbing.

That's because of the arithmetic that drives the shipping business; it’s simple to understand— when the strait became too dangerous to navigate, everything had to be rerouted. So instead of a quick voyage through the strait, cargo had to be transported through far more complicated means... and ships had to sail much longer routes to avoid the danger.

The end result is that oil from the region now crosses far more ocean, and every voyage takes a LOT longer. This means ships are tied up for longer... driving demand higher for shipping.

And it’s not like this problem can be eliminated by simply adding more ships to the global fleet; supertankers take years to build, and shipyards spent the past decade producing very few.

That last part matters, because it is the reason this windfall was visible long before anyone had heard of this war.

One of the largest supertanker owners earned more than $100 million in the first quarter, excluding one-off gains from selling ships, as its fleet was making roughly two and a half times as much per day as a year earlier.

The company paid out every penny of it as a dividend, extending a streak of quarterly payouts stretching back more than fifteen years. And the second quarter will be even better: by early May, it had already booked most of its available days at nearly double its first-quarter rate.

Another major tanker owner reported nearly $200 million in profit for the quarter and declared the largest dividend in its history.

Tankers are not the only winners. One owner of bulk carriers— the ships that haul iron ore, grain, and coal— has become the target of a takeover battle in which a rival has raised its offer again and again, and the board keeps rejecting bids it says still undervalue the fleet.

All three companies are on the research list of Schiff Sovereign's investment newsletter, Strategic Assets.

They were featured in 2023 and 2024, back when shipping was about as unloved as a business can be. That was the point. Shipping moves in long cycles, and the bottom is where the next shortage is easiest to see... because years of terrible rates had stopped owners from ordering ships, and a ship ordered today does not carry cargo for three years.

Counting the ships that would exist in 2026 took no view on Iran— only a public order book.

They met a strict set of criteria: profitable, little or no debt, trading cheap against current cash flow, and operating in an industry with an aging fleet and hardly any new construction on order.

The war revealed that setup; it did not create it. As of early July, one tanker owner had more than doubled since being featured, the other was up more than 90%, and the bulk carrier owner was up more than 50% on a takeover bid rather than a rate spike.

The tankers keep paying quarterly dividends, and one payout alone equals almost 10% of the share price when that company was first featured.

We expect this pattern to repeat across real assets.

The world spent a decade underinvesting in the physical things civilization runs on: ships, mines, oil fields, refineries, smelters. Now geopolitics has turned violent. When there is no spare capacity, every disruption has to be resolved by price, and the companies that own the scarce assets collect the difference.

To be clear, we are not permabulls, and rates like these will not last forever. A durable peace would bring tanker earnings down hard, and shipping has punished euphoric buyers many times before.

Our edge is not predicting wars or commodity prices. It is applying strict criteria to well-run companies, making the case to buy when they meet the bar, and to sell when they no longer do.

That discipline is working. Of the more than twenty companies currently on the research list, six are showing a loss. The companies that we closed out returned an average of 172%.

A silver producer gained more than 950% in under a year, and others returned 540%, 240%, and 150%.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Why They Won't Even Fix the Easy Stuff

Why They Won't Even Fix the Easy Stuff

Notes From the Field By (Simon Black / Sovereign Man) July 27, 2026

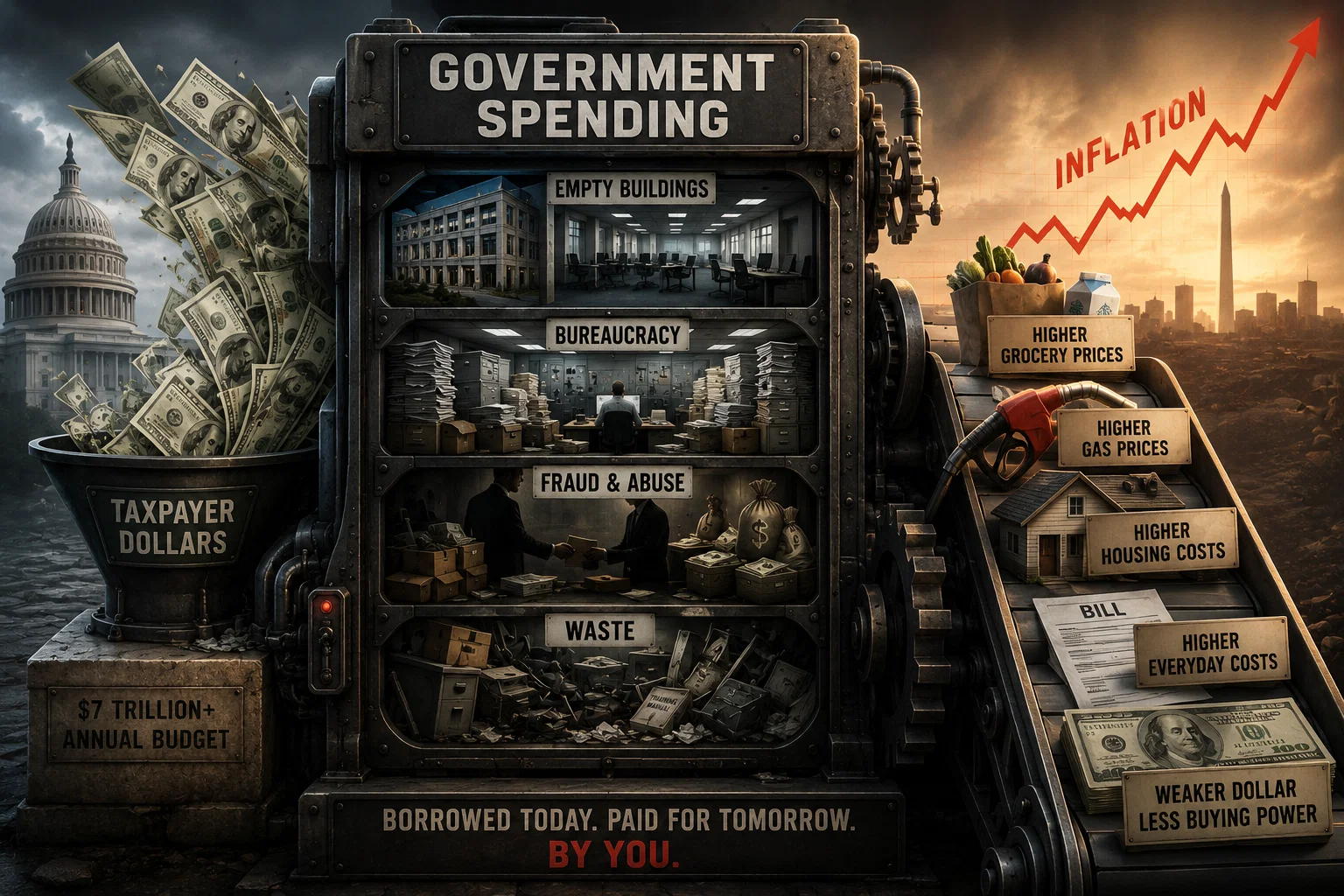

The Department of Transportation's headquarters campus in Washington spans two complexes covering 1.8 million square feet across 11-acre of prime DC real estate. In the private sector, such a trophy office property would fetch north of $1 billion per year in rental income.

Yet for the federal government, two-thirds of the space sits empty according to the Government Accountability Office (GAO), the federal government's own internal watchdog. This is based on real data; the GAO toured the department's buildings last fall and counted the empty desks.

Why They Won't Even Fix the Easy Stuff

Notes From the Field By (Simon Black / Sovereign Man) July 27, 2026

The Department of Transportation's headquarters campus in Washington spans two complexes covering 1.8 million square feet across 11-acre of prime DC real estate. In the private sector, such a trophy office property would fetch north of $1 billion per year in rental income.

Yet for the federal government, two-thirds of the space sits empty according to the Government Accountability Office (GAO), the federal government's own internal watchdog. This is based on real data; the GAO toured the department's buildings last fall and counted the empty desks.

And this is far from an isolated case. Of the 189 government buildings around the country that were analyzed by the GAO, 168 were underutilized— with occupancy averaging just 37%.

One of the worst offenders is One Aviation Plaza in Queens, which sits at 13% occupancy.

Ironically, Congress actually set a MINIMUM standard for all government buildings to be at least 60% occupied. This is the law of the land in the United States, set by the 2023 USE IT Act.

So, Congress was surprisingly trying to make things more efficient and save taxpayer money— potentially billions each year. They passed a law. But the government doesn't follow it.

The big consequence for the government violating its own law so far has been this GAO report. Nobody was fined, nobody was fired, and nothing was sold. Basically we got a PDF.

And all of that is just one category of waste at just one department. The bigger losses are to outright fraud.

In June, the Justice Department announced a record-setting healthcare fraud takedown: 455 defendants, the most ever charged in a single healthcare fraud operation, including 90 doctors and licensed medical professionals, all accused in schemes involving $6.5 billion in fraudulent claims.

Yet federal agents only managed to seize $182 million in cash and assets. No word on what happened to the other $6.3 billion.

By the government's own accounting, federal agencies made close to $200 billion in improper payments in fiscal year 2025 alone... $24 billion more than the year before.

That's money which should never have gone out the door, went out in the wrong amount, or can't be documented. And that was only across 64 programs at 15 agencies... a small fraction of the government's total footprint.

This keeps happening for a simple reason: the federal government's ~$7 trillion annual budget is too vast for anyone to keep track of... and no one is ever held accountable.

Bureaucrats who waste the money never get fired; in fact it is damn near impossible to fire a federal employee. And voters continue electing the same incompetent, crooked politicians to public office.

Even when there's public outcry over obvious fraud, the legacy media closes ranks around their party and insists that voters are racist for criticizing "Learning Centers".

None of this is free. The empty buildings, the stolen billions, the money nobody can track: it all gets paid for with borrowed money. And that deficit spending is what fuels inflation.

June's Consumer Price Index came in at 3.5%. By the Fed's own admission, inflation has now missed its 2% target for five years running.

And after all that failure, few in Washington will name the cause.

A lot of people blame oil, especially after the war with Iran sent crude above $126 a barrel. But oil has been all over the board for the last five years; it was under $60 a barrel just last fall. So why wasn't inflation falling when oil was cheap?

Because, through all of it, there has been exactly one constant: insane levels of government spending. Deficits keep rising, and the more money the government wastes, the more stubborn inflation becomes.

The central bank can't fix that; the Fed doesn't pass spending bills, Congress does. And as long as the spending stays out of control, inflation is not coming down.

And Washington has shown no appetite to bring it under control. They refuse to cut even the easiest, most obvious waste and fraud.

Nothing about this changes on its own. A government that can't bring itself to sell an empty building is not going to take on the spending that actually matters, and inflation is how they'll pay for the difference.

Which is exactly why it makes so much sense to own the real assets that hold their value when the dollar doesn't: gold, silver, and well-managed, productive businesses.

It's definitely time to be thinking about a Plan B.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

P.S. Our flagship service, Plan B Confidential, is built for exactly this: real asset strategies to protect your savings from Washington's spending, and residency options in countries where your money buys far more. It's backed by boots-on-the-ground research from all over the world—

US Taxpayers Subsidized The Greatest Heist Of The Cold War. The Grocery Bill Came Later.

US Taxpayers Subsidized The Greatest Heist Of The Cold War. The Grocery Bill Came Later.

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 23, 2026

In the summer of 1972, a Soviet official named Nikolai Belousov stepped off a plane in New York City with a shopping list.

The Soviet Union had just finished its worst harvest in over a decade and was on the verge of starvation... and Belousov was tasked with the nearly impossible mission of buying enough wheat to feed an entire nation.

US Taxpayers Subsidized The Greatest Heist Of The Cold War. The Grocery Bill Came Later.

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 23, 2026

In the summer of 1972, a Soviet official named Nikolai Belousov stepped off a plane in New York City with a shopping list.

The Soviet Union had just finished its worst harvest in over a decade and was on the verge of starvation... and Belousov was tasked with the nearly impossible mission of buying enough wheat to feed an entire nation.

So he flew to America.

His first meeting was with Michel Fribourg, the head of Continental Grain. The two shook hands and closed a deal for Russia to buy millions of tons of American wheat.

Belousov's next stops were the other biggest grain traders in America: Cargill, Cook, Bunge, Louis Dreyfus, and Garnac.

He worked through every major American grain firm in a matter of weeks— each deal negotiated in complete secrecy... and each firm assumed they were the only American grain house that the Soviets were talking to.

In reality, Belousov was closing deals with all of them.

By the time word got out that the Soviets had been buying from everyone, everywhere, all at once, Belousov had already locked up roughly 440 million bushels of wheat, about a quarter of the entire American crop, for ~$700 million.

And here's the wild part: this was the peak of the Cold War... yet America's staunchest adversary didn't even pay full price for US wheat.

That’s because, for years prior, the US Department of Agriculture had been funding subsidies to make American grain cheaper abroad, covering the gap between the higher domestic price and the lower global price.

So the end result was that the Soviet Union drained American wheat inventory— and that’s when the Law of Supply and Demand kicked in. Wheat prices nearly doubled. Corn prices more than tripled by the following summer. Bread, beef, and eggs all followed.

Yet while Americans were suffering major food inflation at home, the US government was subsidizing the Soviet Union’s wheat purchases to the tune of $300 million in taxpayer funds.

The American taxpayer had financed the largest grain purchase the world had ever seen, for the benefit of its sworn enemy.

Then the second shoe dropped. The following autumn, in October 1973, the Arab oil-producing countries announced an embargo on the United States in response to America backing Israel in the Yom Kippur War.

Consequently, the price of crude oil roughly quadrupled... and it made the food inflation much worse.

Many people don’t realize just how much modern agriculture runs on oil and gas. Nitrogen fertilizer is synthesized from natural gas. Phosphate (another critical fertilizer ingredient) is mined and hauled with diesel. And everything from tractors to grain dryers burns fuel.

Because of the embargo, fertilizer prices more than doubled in 1973 and 1974, and food prices quickly followed. Inflation was eating quite aggressively into consumers’ standards of living.

All of this had a major impact on the stock market; as inflation raged throughout the 1970s, even America’s largest companies suffered. Their earnings shrank (especially when adjusted for inflation) and stock prices went nowhere.

The Dow Jones Industrial Average stock index closed at 1,000 in November 1972... and literally ten years later in November 1982, it was still at 1,000. The market went nowhere over the course of an entire decade.

And adjusted for inflation, of course, most stocks were losers.

The only real winners were REAL ASSET producers— especially gold and energy companies. Gold went from $35 an ounce in the early 1970s to a peak of $850 within a decade— though there were downturns in between.

Gold miners (and silver miners as well) were the best performers of the decade, with the Barron’s Gold Mining Index returning a phenomenal 1,247% in ten years.

Similarly, oil went from about $3 a barrel to nearly $40, and companies like Exxon completely trounced the S&P 500.

More than fifty years later, similar conditions are building again.

The Strait of Hormuz has been effectively closed since late February, except for the tankers Iran waves through from China and its other friends while everyone else waits outside.

Some oil is moving, for sure. But given that about a quarter of the world's sulfur and roughly 15% of its fertilizer exports normally move through that strait, there are significant implications for the agricultural sector.

Many consequences are already on the books.

Urea, the world's most common nitrogen fertilizer, climbed above $850 a tonne this spring, up roughly 80% since February and the highest price since 2022. Sulfur, an essential input for phosphate fertilizer, has doubled since January to record levels.

And in a recent American Farm Bureau survey, 70% of farmers said they cannot afford all the fertilizer they need this season.

Here's why that matters: spring planting is over. Farmers either paid those high fertilizer prices... or they skimped. And skimping means smaller harvests this fall.

Either way, higher food prices are already locked in. The shock has already happened. The impact just hasn’t been felt yet in the grocery stores because the harvest hasn’t taken place yet.

Meanwhile, agricultural markets are trading as if nothing has changed. Crop prices haven't come close to keeping pace with energy and fertilizer costs, and governments are already hoarding: China has temporarily banned phosphate fertilizer exports to keep supplies at home.

The last time this happened, the people who owned fertilizer production made money. Everyone else just got the grocery bill.

The featured research in Schiff Sovereign's investment newsletter, Strategic Assets, already includes a potash producer, a phosphate producer, and a palm oil grower, and we're watching a fantastic fertilizer company for the right entry point.

Our palm oil grower has nearly doubled since we published the research. The potash producer is up more than 16%... with a lot more room to grow. Our phosphate producer, which we recently featured, is still trading inside our suggested buy range.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Why Britain's New Marxist Leader Suddenly Loves Oil

Why Britain's New Marxist Leader Suddenly Loves Oil

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 21, 2026

On November 27th in the year 176 AD, Marcus Aurelius promoted his 15-year old biological son Commodus to be Co-emperor of Rome. Marcus Aurelius never realized it, but he was sealing Rome’s fate… and essentially marking an end to the Empire’s golden age.

Why Britain's New Marxist Leader Suddenly Loves Oil

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 21, 2026

On November 27th in the year 176 AD, Marcus Aurelius promoted his 15-year old biological son Commodus to be Co-emperor of Rome. Marcus Aurelius never realized it, but he was sealing Rome’s fate… and essentially marking an end to the Empire’s golden age.

Commodus was quite popular in his youth— reportedly handsome, athletic, and gregarious. But after Marcus Aurelius died a few years later, the popularity and support that Commodus had enjoyed for so long began to wane.

It didn’t help that he heavily debased Rome’s currency, contributing to widespread inflation and economic decline. He spent lavishly at taxpayer expense, ignored even the most basic affairs of imperial administration, and murdered his enemies.

Finally, on New Year’s Eve in 192 AD, Commodus was assassinated, kicking off a period of political instability in which five different men would sit on the throne in a single year; in fact 193 AD became known as the Year of the Five Emperors.

Eventually Rome landed on Septimius Severus, who ruled for nearly two decades with an iron fist. His reign— though stable— is regarded as one of the cruelest in Roman history. And he, too, contributed immensely to inflation and rising taxes.

His successor, Caracalla, ruled briefly and incompetently. Soon came Elagabalus— history’s first transgender emperor who promised to give away half of the empire to any physician who could turn him into a woman.

Along the way the infamous “Crisis of the Third Century” became worse and worse: migrant invasions, economic depression, hyperinflation, plague, and unprecedented political instability— including the year 238 AD in which six different men claimed the title of Emperor.

It was as if Rome lost the ability to produce a decent, capable leader anymore.

I thought of this historical lesson yesterday morning watching Andy Burnham, the former mayor of Greater Manchester, become Britain's seventh prime minister in a decade.

That’s an unprecedented level of instability for a modern, major power. Even worse, Britain’s leaders have become more incompetent over time, each one chipping away at the country’s economy and social stability.

Liz Truss lasted just 49 days, the shortest tenure of any prime minister in British history. Her plan for £45 billion in unfunded tax cuts set off a panic in the bond market, launching the pound into freefall.

And government borrowing costs spiked so violently as a result of Ms. Truss that the Bank of England had to step in to prevent British pension funds from collapsing.

Prior to Truss was Boris Johnson— a one-man scandal machine who was fined for quite hypocritically throwing big parties in Downing Street during his own COVID lockdowns.

Then came Rishi Sunak, who threw Britain's doors wide open to immigration. Sunak seemingly woke up every morning and said: Give me more Somalis. Give me more Islamic terrorists.

Along the way, Britain imported some of the worst ideas of the American Left and made them its own.

Britain is now the wokest place on the planet, and to an Orwellian standard; British police arrest people over tweets, and the England flag itself is now treated as a symbol of racism.

To cap it all off, Sunak was succeeded by Keir Starmer, probably the worst leader of a major power in modern history— and that includes Joe Biden.

When Parliament took up a national inquiry into the grooming gangs that had raped thousands of English girls over decades while local officials looked away, Starmer's party voted it down, and Starmer dismissed the calls as "the bandwagon [of] the far right."

Starmer spent his tenure finishing off the oil industry, taking the headline tax rate on North Sea producers to 78% and banning new exploration licenses.

By the time Starmer resigned last month, the UK had a tax burden heading to its highest level since records began in 1948. Borrowing costs are higher than any other major economy, with 10-year government bond yields well above those in the US, France, Germany, and Japan.

Plus, wealthy Brits are heading for the exits in record numbers after Starmer abolished the centuries-old non-dom tax regime.

Starmer was so widely despised that his own party finally threw him out. Their solution? A slightly younger, slightly less vapid version of Starmer.

His name is Andy Burnham, and all of his ideas come straight from the Communist Manifesto.

In his opening remarks as prime minister, Burnham said not one word about the national debt or Britain's borrowing costs. Nothing about the migration crisis. Nothing about justice for the grooming gang victims. Nothing about turning the economy around.

His first order of business, Burnham announced, was taking care of homeless/migrants with a new £340 million benefit program.

To his credit, Burnham has sense enough to know that he cannot throw around that kind of money without a way to pay for it. Borrowing more money is out; in fact he spent the past year complaining that Britain must get beyond "being in hock to the bond markets."

That only means one thing: higher taxes.

So, days before taking office, his team began preparing approvals for two North Sea oil and gas fields— the same ones that his own party spent years trying to shut down.

This is not because Burnham suddenly cares about energy security. He’s just looking for more money to steal.

All of those homeless migrants need handouts, so Burnham needs a new revenue stream, i.e. something else to tax.

So he’s allowing two new North Sea fields— with the existing 78% rate in place.

In short, Burnham did not decide that energy matters. He decided it hasn’t been milked entirely dry yet.

This is a cannibalist mentality. Britain is sliding into its own Crisis of the 21st Century, and the "conservative" politicians who presided over the first half of the decline were anything but. Starmer and now Burnham are straight-up Marxists.

We wrote about Argentina just yesterday, where nearly every asset in the country is surging. It’s not hard to understand why: Argentina hit rock bottom, threw out the people who destroyed the country, and started climbing under new leadership.

Britain can reverse its fortunes the same way. Unfortunately, it is probably going to have to hit rock bottom first. And we can already see the shape of how this ends.

First the money will run out, the benefits will be cut, and the people who came for free stuff will go home.

Then, with markets in the dumps, this highly educated and productive country will eventually reverse all of its idiotic policies from the past and one day become among the most interesting places in the world to invest.

There’s an old saying credited to a Rothschild about investing when there’s “blood in the streets.” He may turn out to be right. But he probably wasn't picturing London when he said it.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Why Central Banks Love a Gold Sell-Off

Why Central Banks Love a Gold Sell-Off

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 14, 2026

On July 7, Bloomberg published an article with the headline: "Gold's Bull Market Has Ended and Now All Eyes Are on Bears," explaining how many retail investors have headed for the exits.

Why Central Banks Love a Gold Sell-Off

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 14, 2026

On July 7, Bloomberg published an article with the headline: "Gold's Bull Market Has Ended and Now All Eyes Are on Bears," explaining how many retail investors have headed for the exits.

That same day, the People's Bank of China, the country's central bank, reported its largest monthly gold purchase since 2023.

Of course, June marked its twentieth consecutive month of adding gold to its reserves. Central banks are relatively price insensitive. They buy gold as a long term hedge to preserve value, not to trade back for more paper.

But they aren’t stupid either, and this shows they are buying the dip.

Gold peaked at $5,589 per ounce on January 28 and trades around $4,000 today, roughly 28% below the high. The second quarter was gold's worst since 2013. Investors have pulled about $18 billion out of gold ETFs since the peak, much of it late money that piled in during last year's frenzy and bolted the moment momentum broke.

But the price is not the story. The story is what central banks are doing.

Central banks have been the dominant force in gold since 2022, when Russia invaded Ukraine, the US froze $300 billion of Russia's central bank reserves, and every finance ministry on earth learned that dollar assets were not the safe havens they’d believed.

In 2024, central banks bought 1,090 tons of gold, close to an all-time record.

That massive demand made gold expensive. The price nearly doubled from its 2025 low, and central bank buying slowed to 863 tons. That was still higher than historical averages, but down 21% from the year before.

The slowdown was not fading interest; it was price discipline. Central banks are not traders chasing momentum. They are savers accumulating a reserve asset, and like any sensible saver, they buy less when the thing they are saving in gets expensive.

And they speed back up when it goes on sale. In the first quarter of this year central banks bought 244 tons, more than the previous quarter and above the five-year average. China alone has added about 40 tons in the first six months of 2026, compared to just 27 tons in all of 2025. The People's Bank of China bought more gold last month, with the price down nearly 30% from its high, than in any single month of the entire run-up.

The Reason Is Simple: Nothing Has Changed About Why They Buy

The World Gold Council, the industry group that tracks official gold demand, surveyed 76 central banks this year. Seventy-four percent said they expect the dollar's share of global reserves to be lower five years from now.

These are the institutions that actually hold the world's reserves, and they are telling you, on the record, that they plan to keep moving away from the dollar.

None of their reasons went away when the price fell. The US national debt keeps growing by trillions, Congress has no plan beyond borrowing more, and Washington keeps proving it will continue to weaponize the dollar.

A central bank holding dollars is holding the liability of a government that is both overextended and unpredictable. Gold sitting in its own vault carries neither risk.

That calculus was true at $5,589, and it is just as true at $4,000.

A trader who is down 28% has a problem if they are trying to quickly turn a profit, and accumulate more paper dollars.

But a saver who plans to accumulate gold for the next decade just got a better price. That is why the sell-off did not scare away the biggest buyers in the market.

It may be exactly what they were waiting for.

We made this argument to our subscribers of our investment research newsletter, Strategic Assets, in January.

With gold near its all-time high, we said that this was no longer the early stage of a bull market, that a major drawdown was a real possibility, and that it was time to take some profits.

In fact, subscribers who took action on our research locked in gains of more than 950% on a small silver producer and 540% on a gold and silver producer, both in under a year.

Now the sell-off has come for the miners too. Even solid, debt-free producers are trading as much as 50% below their highs from earlier this year.

But again, as nothing had changed about the long term gold thesis, little has changed about the profitability of these companies. They are still wildly profitable at $4,000 gold, which is far above projections they had planned for.

Some of these companies are still pulling gold out of the ground at a cost of just $1,000 an ounce, which is an amazing margin.

So We Are Starting To Buy Again.

It is the same discipline the central banks just demonstrated: slow down when the asset is expensive, step up when it gets cheap, and never confuse a price correction with a change in the story.

Nobody knows where gold trades next month. But the biggest buyers on earth just showed you what they do when gold gets cheaper. They buy more.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

The Latest Flashing Exit Sign for the US Dollar

The Latest Flashing Exit Sign for the US Dollar

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 13, 2026

Washington has a comforting story about Social Security: yes, the trust fund is running out of money, but not until 2032. That leaves six more years to form the commissions, schedule the hearings, and study a problem that has been obvious for decades.

But last week, a man who used to run the numbers for Social Security itself explained why even a measly six years is optimistic.

The Latest Flashing Exit Sign for the US Dollar

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 13, 2026

Washington has a comforting story about Social Security: yes, the trust fund is running out of money, but not until 2032. That leaves six more years to form the commissions, schedule the hearings, and study a problem that has been obvious for decades.

But last week, a man who used to run the numbers for Social Security itself explained why even a measly six years is optimistic.

Jason Fichtner is the former chief economist of the Social Security Administration, which means he spent years inside the building watching the program's finances deteriorate.

According to the latest annual report from Social Security's own trustees, the program's main trust fund will be empty by late 2032. From that moment, incoming payroll taxes cover only 78% of scheduled benefits, which means an automatic 22% cut for every retiree in America.

But Fichtner recently told CNBC that the real deadline has nothing to do with 2032, because the bond market will move first.

He said that well before 2032, “the bond market looks and says, ’Well, you guys have 12 months to get your act in order; you’re going to be looking for another $600-plus billion a year,” which is why, “Fiscal strain could come earlier than trust fund depletion.”

Cutting grandma's check by 22% overnight is the closest thing to guaranteed electoral suicide that exists in American politics. So they'll do what they always do and borrow the difference. Fichtner and economist Veronique de Rugy calculate that filling the gap means roughly $600 billion in new borrowing in the first year, growing to about $700 billion a year by 2036.

And that money doesn't appear out of thin air. The Treasury borrows from the same pool of savings that everyone else uses, the pool that funds mortgages, car loans, and business investment. When the world's largest borrower suddenly demands another $600 billion a year from that pool, the price of money goes up for everybody.

Markets are forward-looking. An investor buying a 10-year Treasury today is holding paper that matures years after the trust fund runs dry, so the question of whether Congress will fix Social Security is already priced into that bond, every single day. Investors won't wait politely until the checks shrink in 2032. They will reprice the moment congressional inaction looks locked in, a year or more ahead of the deadline, exactly as Fichtner describes.

And inaction is the base case. Nine months into fiscal year 2026, the federal deficit has already reached $1.4 trillion according to the Congressional Budget Office, running ahead of last year's pace. This is happening with no major crisis draining the coffers, with the economy growing and unemployment low.

Meanwhile, the lenders who would have to fund all this new borrowing are backing away.

The dollar has fallen roughly 8% from its early 2025 peak. In March alone, foreign holdings of US Treasuries fell by about $240 billion, with Japan selling nearly $48 billion and China unloading another $41 billion. China's holdings now sit at their lowest level since 2008. The single largest pools of foreign capital on the planet are quietly reducing their exposure to the very asset Washington needs them to buy more of.

Worse, they are actively looking for the exits.

And on July 9, the European Parliament voted 416 to 169 to push the digital euro into final negotiations, and the stated goal is to reduce Europe's dependence on non-EU payment providers like Visa and Mastercard, which currently handle 61% of card payments in the eurozone.

That is a bureaucratic way to say: Europe no longer wants its money to be forced to move through American companies.

Consider how deep the dollar's dominance runs today: when France-based Airbus sells a jet to Air France, the price tag is in US dollars. A French company selling to a French airline, and the invoice is still written in Washington's currency.

That is the system Europe's political class just voted, by a two-to-one margin, to start engineering its way out of. Every step in that direction shrinks the pool of foreigners who need dollars, and fewer people who need dollars means fewer natural buyers for US government debt.

The real deadline for the fallout from Social Security’s 2032 depletion is whenever the bond market decides Congress won't act. And every lender heading for the exit moves that date closer, because a thinner pool of buyers means the repricing, when it comes, will be sharper.

Higher interest rates arriving years ahead of schedule would hit an economy that runs entirely on cheap debt. The government's interest bill, corporate borrowing, mortgages, the whole structure assumes money stays affordable. And the foreign lenders who could soften that blow by absorbing the new supply are already leaving.

Congress, in other words, is planning around a deadline that exists only on paper.

The bond market keeps its own calendar. And nobody in Washington seems to have asked what happens if the market's calendar runs faster than theirs.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

America Turns 250 At 125, It Looked Like the End

America Turns 250 At 125, It Looked Like the End

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 3, 2026

On the afternoon of September 6, 1901, President William McKinley stood in a receiving line at the Pan-American Exposition in Buffalo, New York, shaking hands with a crowd of well-wishers.

One of the people in the crowd was a young man named Leon Czolgosz... who was patiently waiting with a revolver wrapped in a handkerchief. When he reached the front, he fired twice into the president's abdomen.

America Turns 250 At 125, It Looked Like the End

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 3, 2026

On the afternoon of September 6, 1901, President William McKinley stood in a receiving line at the Pan-American Exposition in Buffalo, New York, shaking hands with a crowd of well-wishers.

One of the people in the crowd was a young man named Leon Czolgosz... who was patiently waiting with a revolver wrapped in a handkerchief. When he reached the front, he fired twice into the president's abdomen.

McKinley died eight days later, and, Czolgosz, an unemployed factory worker, went to the electric chair without a trace of remorse. He insisted it was his duty to strike down a symbol of oppression.

Czolgosz wasn’t a crazed madman, but rather a product of his time. The America of 1901 was 125 years into its history— the exact midpoint between the Declaration of Independence and today.

And despite the US economy already being the largest in the world at that point, the year 1901 did not feel like a nation striding confidently into the American Century.

The US financial system lurched from panic to panic, and to a great many observers, the young republic looked less like a rising power and more like a country unraveling.

The rich versus poor divide was growing, and violent socialist movements spread. Political assassinations, terrorism, and bombings became a recurring feature of public life.

The political violence did not end with McKinley’s assassination, either. Followers of the Italian anarchist Luigi Galleani waged a years-long bombing campaign against judges, politicians, and businessmen.

It peaked at noon on September 16, 1920, when a horse-drawn wagon packed with explosives detonated in front of the headquarters of J.P. Morgan on Wall Street, killing thirty people and wounding hundreds more. The case was never solved.

Many of these anarcho-socialists were immigrants, which poured gasoline on the raging blaze of backlash against widespread immigration.

In 1907 alone, more than a million people passed through Ellis Island. Immigrants were arriving faster than anyone knew how to absorb them, and people were getting tired of it.

Congress passed legislation that imposed a literacy test on immigrants, then banned entire countries. At first, people from Asia and the Middle East were shut out. Subsequent legislation set strict quotas, slamming the door on the southern and eastern Europeans who were considered undesirable.

Yet the instability continued... as did the government’s push to consolidate power.

After the Panic of 1907 nearly brought down the financial system, Congress used the scare to establish the Federal Reserve in 1913. This was the first step toward money that could be printed at will.

Also in 1913, the Constitution was amended, giving Congress the power to tax income.

The income tax (16th Amendment) was sold to the American people as a tax on the very rich that would only affect the top 2% of US households. Idiotic socialists at the time believed the lie and supported the amendment; after all, the rich should pay their fair share.

Within decades, three quarters of Americans were paying income tax.

With a new central bank and tax power in place, Washington then raced to join World War I (despite being an ocean away), and borrowed on an unimaginable scale to do it.

Frankly it all looked pretty bleak.

And yet, while all the bad news and turmoil was ongoing, America was simultaneously producing miracles.

Henry Ford put the country on wheels with the Model T and the moving assembly line. Motion pictures went from novelty to industry. Radio turned from a tinkerer's hobby into a machine that could broadcast to every home in the nation.

These were American breakthroughs that rewired the entire global economy and powered better times ahead.

Seventy-five years later, America's 200th birthday looked little better. In 1976, the economy was mired in stagflation that “experts” had previously sworn was impossible.

Oil shocks had humiliated the country at the gas pump. American dominance looked spent in the wreckage of Vietnam, and the nation had watched President Richard Nixon resign in disgrace.

Terrorism was back. Plane hijackings were somewhat commonplace. Crime rampaged across the cities.

And yet what followed was the personal computer, the Internet, the longest peacetime expansion in the country's history, and a comeback almost nobody standing in a gas line in 1976 would have believed.

Which brings us to the 250th birthday, today.

Political violence is back in American life. Immigration is once again a major issue. Fraud and corruption are rampant (and hardly anyone pays the price). And Washington's finances are in worse shape than at any point in the country's history, with the national debt larger than the entire economy.

Yet at the same time, American companies are building artificial intelligence, next-generation nuclear power, robotics, and biotech breakthroughs that could rewire the global economy even more than the assembly line and the Internet did. Chaos and invention have always lived side by side in the US, and they still do.

America was born out of revolution, and it has endured a civil war, two world wars, a depression, a decade of stagflation, and repeated financial panics.

Every one of those episodes brought years of real pain, but every time, the country that looked terminally ill came back stronger than ever.

There is an old saying in politics (usually credited to Winston Churchill, though apparently first quipped by an Israeli diplomat): Americans will always do the right thing... after exhausting all the alternatives.

Apocryphal or not, that is the pattern: the right thing comes eventually, but the pain comes first.

America is not just a country; it is an idea, and it may be the most extraordinary idea human beings have ever assembled. It stands on the shoulders of giants— Greek thought, Roman law, Judeo-Christian values, and free-market capitalism, fused with a conviction about individual liberty balanced by personal responsibility.

Betting against that idea has been the worst trade of the past 250 years.

To be clear, having a Plan B is not a bet against America either. The concept is not to hide in a bunker with canned food and guns because the end is near.

The point of a Plan B is to be honest about the road between here and the recovery: more inflation, higher taxes, and a stretch of instability, and to make sure you have the options available to come at it from a position of strength.

At 250 years, I truly believe the best days are still ahead. But there will be some rough ones in between.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

Why China Just Overtook The US With The Most Powerful Supercomputer

Why China Just Overtook The US With The Most Powerful Supercomputer

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 1, 2026

Yao Tongbin was one of the most important scientists in Maoist China. He had earned a doctorate in metallurgy in England, spent three years at a research institute in West Germany, and left it all to return to China in 1957.

He spent he next 11 years building China’s first-ever modern missile program, with unparalleled knowledge and experience he had accumulated in the West.

Why China Just Overtook The US With The Most Powerful Supercomputer

Notes From the Field By James Hickman (Simon Black / Sovereign Man) July 1, 2026

Yao Tongbin was one of the most important scientists in Maoist China. He had earned a doctorate in metallurgy in England, spent three years at a research institute in West Germany, and left it all to return to China in 1957.

He spent he next 11 years building China’s first-ever modern missile program, with unparalleled knowledge and experience he had accumulated in the West.

But when he came home for lunch on the afternoon of June 8, 1968, a gang of thugs from a rival political faction was waiting for him. They beat him to death in his own apartment. He was forty-five years old.

Yao’s crime was that he was educated, expert, and Western-trained— exactly the kind of man that Mao’s Cultural Revolution had taught the country to hate.

From 1966 to 1976, Mao turned China against its own educated class, rooting out political opposition and handing a the power to young revolutionaries.

Professors were dragged before their students in dunce caps and beaten mercilessly. Universities shut their doors. Millions of educated young people were shipped off to work camps. And engineers were ranked near the bottom of the social order.

China spent ten years treating intelligence as a crime, and the country paid the price for a generation.

Meanwhile, over in the West at the same time that Mao's Red Guards were beating engineers to death, American technological geniuses developed the world's first microprocessor and lit up the first nodes of the internet... effectively giving birth to the digital age.

It was a night-and-day difference between the US and China. China was actively, stupidly making itself worse off, while the US was developing the technology that would change the world forever.

America remained the epicenter of technological innovation for decades; in fact, the unofficial ‘scoreboard’ of the world’s most technologically advanced nation was whoever could build the fastest supercomputer.

And the answer was obviously the United States... until Japan shocked the world in 1995 and beat the fastest US supercomputer. America quickly reclaimed the top spot, only to be bested by Japan again in 2002.

The two great technological powers jostled for #1 for the next several years until the unthinkable happened in 2010: China developed the world’s fastest supercomputer.

For the past sixteen years, those three powers— America, Japan, and China, have traded the trophy. And China just retook it from the US again last week.

This is a symbolic, albeit critical competition— especially now as there are so many challenges to America’s economic, military, and geopolitical leadership.

Why is America falling behind? Because of its own soft “Cultural Revolution” driving out competence and rewarding the people who build nothing.

During COVID, the government and media conspired to destroy the careers of anyone who questioned Tony Fauci.

Shortly thereafter, the DEI cult took over. From transgender Bud Light influencers to absurdly woke Disney movies to mandatory diversity quotas in corporate boardrooms... and it went all the way to the most powerful institutions in America.

Joe Biden promised a female running mate as his Vice President, and a black woman as a Supreme Court justice. His obsession with diversity over merit resulted in two extremely unqualified people in some of the nation’s highest offices.

The end result has been predictable across the military, public health, medicine, and the media, institutions that increasingly selected for ideology over competence.

Mao destroyed his most capable people on purpose, and it cost China a generation. America is now doing the same thing to itself in a softer way.

But regardless of the tactics, any country that pushes out people who can design the chips, fly the planes, run the labs, and keep the lights on, is shooting itself in the foot.

Here’s another interesting example—

On a recent, private call for our top-tier Total Access members, we spoke with a really unique American entrepreneur based in Africa who sees this DEI rot every single day.

China, he told us, runs a "full court press" in Africa. The Chinese government fights for its businesses and helps them invest aggressively in the strategic resources that China needs back home. Food production. Energy. Water. Minerals.

Meanwhile, as China rapidly scoops up critical resources and builds relationships on the continent, the US-funded Western NGOs are busy with DEI and climate change initiatives.

He told us about one particular NGO, a group that pulled out of a critical agricultural investment over concerns that there weren’t enough women involved and too much CO2.

The difference in priorities between China and the West could not be more obvious.

Now, none of this means that China takes over the world. America has faced down a rising manufacturing rival before. It absorbed Japan's challenge in the 1980s, and it out-produced and out-innovated the Soviet Union as well.

The United States still commands the deepest capital markets on earth, enormous pools of talent, and a genius for inventing and building that no rival has ever matched.

China's problems, by contrast, are far greater.

It shares borders with fourteen countries, including North Korea, Pakistan, India, and Afghanistan. It doesn’t have trusted relations with a single one of them.

China is the largest oil importer in the world by a wide margin and has astonishingly thin per-capita reserves. It is lean on water and quality farmland. Its regional governments are buried under mountains of debt.

And it is, quite bizarrely, facing a massive demographic crisis of its own making (from years of its idiotic one child policy) while simultaneously and precariously trying to keep a population of 1.4 billion people under strict authoritarian control.

Plus, let’s be honest— a centrally planned economy will not deliver maximum innovation. Yes, America has its own idiots in office. But for every Lizzie Warren and AOC, China has plenty of its own morons in government service who make painfully idiotic decisions.

America’s problems are gargantuan, yes. But at their core, they are completely fixable. Three simple approaches would dramatically move the needle. Quickly.

Cut the federal deficit by reducing obvious fraud and exercising common sense restraint.

Boost economic productivity by eliminating pointless federal and state regulations.

Focus exclusively on merit rather than DEI credentials.

Those three are very simple and straightforward, and they would dramatically move the needle. And that’s before tackling other challenges like Social Security, immigration, and election reform.

China might have temporarily taken the top spot in supercomputing. But this is still America’s race to lose.

The plan is maddeningly simple. Unfortunately, if history is any guide, Congress will probably do nothing until there’s a bad-enough crisis to force them to act. And that’s why it makes so much sense to have a Plan B.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

PS: That conversation with the investor in Africa came from a private call for our Total Access members. Total Access is the top tier of Schiff Sovereign membership, built for those who value global networks of like-minded people.

Members get all of our research — Plan B Confidential, Strategic Assets, along with the deepest second-passport discounts we can negotiate, events, boots-on-the-ground explorations, and a network of people quietly building their own Plan B.

The World's Gold Is Quietly Leaving London and New York

The World's Gold Is Quietly Leaving London and New York

Notes From the Field By James Hickman (Simon Black) June 29, 2026

In December 1916, with German and Austro-Hungarian armies closing in on Bucharest, the Romanian government made a decision that must have felt entirely sensible at the time.

Romania had gambled its way into the Great War a few months earlier, sending its army across the Carpathian Mountains to grab Austro-Hungarian Transylvania, believing that Germany and Austria-Hungary were too exhausted to stop them.

The World's Gold Is Quietly Leaving London and New York

Notes From the Field By James Hickman (Simon Black) June 29, 2026

In December 1916, with German and Austro-Hungarian armies closing in on Bucharest, the Romanian government made a decision that must have felt entirely sensible at the time.

Romania had gambled its way into the Great War a few months earlier, sending its army across the Carpathian Mountains to grab Austro-Hungarian Transylvania, believing that Germany and Austria-Hungary were too exhausted to stop them.

But Romania’s gamble fell apart in weeks. German and Austro-Hungarian were exhausted. But not so exhausted to allow Romania to waltz across the border and grab territory uncontested.

The Central Powers quickly reacted, beat the Romanian army all the way back to Bucharest, and then converged on the capital. The King of Romania and his court fled the country just before it fell.

Just before surrendering, however, Romania’s Prime Minister Ion Brătianu made a bold decision to seal up the country’s gold reserves. He ordered more than 90 tonnes of gold to be loaded in over 1,700 crates onto seventeen railcars, and had it shipped to the one ally Romania was certain it could trust: Russia.

The arrangement made sense on paper. Tsar Nicholas II was Romania's wartime partner, and an overland route to ship the national gold reserves to Moscow seemed far safer than risking German submarines on the sea route to London.

Fortunately the crates arrived safely; Russian officials locked the gold securely inside the Kremlin and provided a written guarantee that the gold remained Romanian property.

But the Russian Revolution broke out only months later. The Bolsheviks seized power, arrested the Tsar, and eventually murdered him and his family. In January 1918, Leon Trotsky severed ties with Romania and declared its gold "untouchable for the Romanian oligarchy."

It’s been more than a century, and Romania is still asking for its gold back from Russia. The gold is worth about $12 billion today and has never been returned.

For most of human history, a king kept his gold where he could see it. It sat behind his own walls, in his own keep, guarded by his own men. The idea of loading your treasure onto a ship and sending it to a rival capital for safekeeping would have struck any medieval monarch as total insanity.

The King of France did not store his gold in London. You did not hand a rival your treasury to seize the moment relations soured.

What changed first was London. By the nineteenth century, Britain ruled an empire that spanned the globe. Its navy went unchallenged. And the British pound was redeemable for gold.

The City of London sat at the center of world finance and ran the deepest gold market on earth.

For foreign governments, keeping gold in the Bank of England's vaults was not a surrender but an upgrade. The metal was safer behind Britain's guns than behind its own, and given the advances of British finance, the gold could be sold, lent, or borrowed against in an afternoon.

The gravity of financial power shifted to New York a century later as Nazi forces conquered Europe. Allowing your national gold reserves to be confiscated by Hitler became a much greater risk than shipping everything to America.

So country after country scrambled to move their gold before German tanks crossed the border.

America was the safest vault on earth: a nation with an ocean on either side, an economy the war had only strengthened, and a bright future ahead of it.

After the war, the 1944 Bretton Woods agreement pinned the dollar to gold— and pegged every global currency to the US dollar. And from then on New York (and London to a lesser degree) were the obvious places for foreign governments to hold their gold reserves.

A country could settle international debts without moving a single ounce, just by having a clerk slide its bars from one stack to another within the same vault.

The arrangement held for eighty years because the US remained the most powerful, most trusted government in the world. But now that trust is vanishing quickly.

According to a recent report published by the World Gold Council, the number of foreign central banks storing gold in New York or London slipped 17% and 11% respectively. And that’s just in a single year.

And the number of central banks bringing their gold home (or at least moving it to neutral third-party vaults) nearly tripled. Gold, for the most part, is going home.

They’re also buying more of it, with central bank gold purchases running at roughly double the historic rate for the third year in a row.

To fund those purchases, central banks are selling US Treasuries... or letting them mature without reinvesting.

Over the past year, gold passed both US Treasuries and the euro to become the single largest reserve asset on earth. And for the first time since 1996, central banks now hold more gold than US Treasuries.

Central banks almost never sell gold. On the rare occasion that some country does sell, it’s usually because they’re in a genuine crisis (like Turkey selling gold to defend a collapsing currency).

Or, as was the case with the British government in the late 1990s, they’re the dumbest people alive.

Absent that kind of emergency or stupidity, governments and central banks “hodl” their gold.

Bottom line, these countries are not shipping their gold out of London and New York to sell it. Just the opposite. It is proof they intend to hold the metal for a very long time, and that they are willing to give up using it as a financial instrument.

None of this is about the gold price on any given morning.

Over the last few weeks, gold slipped below $4,000 an ounce for the first time since November.

Since last fall, as retail investors entered the market driving the price of gold sharply higher, we warned that a pullback like this was likely.

But we also said that nothing about the thesis was changing. The US was still spending far beyond its means and weaponizing the dollar. Washington was still dysfunctional— full of AOCs and Elizabeth Warrens. Therefore global central banks were continuing to diversify their reserves.

We’re not fanatical about gold. But it’s clear that the long-term catalysts to drive prices higher are not going away anytime soon.

The world is more fractured than it was even a few years ago, and dollar dominance is slipping.

So what does everyone own instead? China is pushing for international use of its yuan... and you can see a flicker of it in the payments data. But it is not a real alternative.

The one asset every central bank on earth can hold without worrying who controls it is gold. Plus they all have confidence that gold will still have strategic value 5, 10, 20+ years from now.

That’s why these central banks view $4,000 gold as a reasonable entry point to accumulate more, and they likely will not miss the chance to do so.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

P.S. The same opportunity is open to everyone else. As gold sold off, so did shares in the companies that dig it out of the ground. Even at gold's all-time highs, many of these producers traded at low multiples while selling their gold for far more than their projections ever assumed.

Their costs stayed roughly fixed, so margins exploded, and some have started paying dividends or raised the ones they had. At $4,000 gold they are still enormously profitable, yet fickle investors are dumping them as if the gold story is over.

It is not. Nothing has changed about why central banks buy, and so far they have moved only a small share of their reserves into gold.

If you want to learn more about these gold companies, and other real assets we research in our newsletter, Strategic Assets, click here.

Get Ready for “Business Friendly Socialism”

Get Ready for “Business Friendly Socialism”

Notes From the Field By James Hickman (Simon Black / Sovereign Man) June 22, 2026

On New Year's Day in the year 1829, a 29-year-old young lady from Washington DC named Peggy Timberlake married John Eaton— a powerful senator from Tennessee. Eaton was also close friends with the incoming president Andrew Jackson.

Peggy, on the other hand, was rumored to be somewhat of a harlot. She was openly flirtatious and allegedly promiscuous, and her wedding to Sen. Eaton came only a few months after the mysterious death of her first husband.

Get Ready for “Business Friendly Socialism”

Notes From the Field By James Hickman (Simon Black / Sovereign Man) June 22, 2026

On New Year's Day in the year 1829, a 29-year-old young lady from Washington DC named Peggy Timberlake married John Eaton— a powerful senator from Tennessee. Eaton was also close friends with the incoming president Andrew Jackson.

Peggy, on the other hand, was rumored to be somewhat of a harlot. She was openly flirtatious and allegedly promiscuous, and her wedding to Sen. Eaton came only a few months after the mysterious death of her first husband.

The elite “power wives” of Washington DC considered Peggy scandalous and immoral, and so they simply refused to engage with her. They would not attend any event where Peggy would be present. They would not invite her to their parties. They spoke ill of her behind her back.

So when Andrew Jackson made Sen. Eaton his Secretary of War in March of 1829, the snub against Peggy became a federal problem.

President Jackson, whose own late wife had been savaged by similar gossip during the brutal 1828 campaign, took the shunning of Peggy as a personal insult. And he actually demanded that his cabinet bring their wives into line and accept her.

Jackson’s cabinet could not (or would not) demand this of their wives. And for more than two years, the so-called “Petticoat Affair” consumed federal attention.

It finally ended in the spring of 1831 with something America had never seen: Jackson’s entire cabinet resigned except for the Postmaster General. The Secretaries of State, Treasury, etc. all left. Even Eaton as Secretary of War resigned.

In short, a dispute over whether the power wives of Washington were willing to invite another lady to dinner had resulted in the effective dissolution of the executive branch.

Nearly two centuries later, that remains almost unimaginable. High-level resignation is something the American government simply does not do.

In its entire history exactly one president has resigned— Richard Nixon, in 1974, and only to avoid impeachment.

Only two vice presidents have resigned, including Spiro Agnew in 1973 due to pending criminal charges.

American politicians only give up power under extreme duress— likely a family emergency... or the imminent arrival of a criminal indictment. It is a “from-my-cold-dead-hands” political culture. We even treat a President declining to seek reelection as a major event.

In Britain, by contrast, prime ministers resign all the time. When they lose the confidence of their party, they step down... and the machine produces another.

I used to think that was a genuine strength— that American politics might be healthier if resigning were less taboo.

Keir Starmer is the perfect illustration. By this spring his net approval had collapsed to the lowest rating recorded for any prime minister since Ipsos began measuring in 1977.

Failure didn’t bother him. In fact Starmer’s government kept criminalizing criticism— Britain now jails its own citizens for anti-migrant posts while the actual migrant criminals walk free and receive taxpayer assistance.

Even last month, with dozens in his own party urging him to resign, Starmer remained defiant: "The country expects us to get on with governing. That is what I am doing and what we must do as a cabinet."

What finally forced him out was not voters. Yes, his own party helped push him out after disastrous local elections cost Labour more than a thousand races last month.

But underneath that sat the bond market.

Investors had been dumping British government debt for weeks, and in early May the yield on the 30-year gilt spiked to the highest level in decades.

Bond investors want fiscal restraint. And they had concluded that Starmer would respond to his electoral beating by spending even more money.

So naturally, investors sold their UK government bonds... and the British government’s borrowing costs soared.

This is nothing new; less than four years ago, then Prime Minister Liz Truss resigned after just 44 days because the bond market didn’t like her economic plan. Bond yields surged and the British pound went into free fall.

Calm returned only after Truss resigned in disgrace.

The sad irony is that Starmer's likely successor is worse. Andy Burnham— the longtime mayor of Greater Manchester— campaigns on what he calls "business friendly socialism", which makes as much sense as “vegan wolf”.

He also wants more borrowing, higher taxes, and bringing utilities and "public essentials" back under state control.

Bizarrely, Burnham has complained that Britain is "in hock to the bond markets," as though the people lending to the government should simply hand over their capital with no questions asked.

(Given Mr. Burnham’s penchant for nationalization, he may in fact get his way. I wouldn’t be surprised to see more wealth tax proposals in the UK.)

The actual solution is embarrassingly simple. You are only “in hock to the bond market” if you borrow. Balance the budget, live within your means, and the bond market gets no vote at all.

Yet basic fiscal responsibility is an impossible idea— and it tells you everything about the modern Western politician. This most certainly will not improve under a "business friendly" socialist.

Ultimately, the last institution still imposing any discipline on government is not the voter— it's the creditor. And the United States, with its own debt arithmetic getting worse every year, is approaching that the same line.

One day the bond market will start calling the shots in Washington too, voters' wishes be damned, and it will do it through higher yields and a weaker dollar.

To your freedom, James Hickman Co-Founder, Schiff Sovereign LLC

P.S. In the US, the bond market is already voting, with higher yields and a weaker dollar. And the bill lands on anyone holding those dollars.

The sensible hedge is to own real assets no government can print.

Real assets are tangible things with intrinsic worth— gold and silver, energy, productive land, and the companies that own them— and because no central bank can conjure them into existence, they hold their purchasing power while paper currencies lose theirs.

That's what Schiff Sovereign's investment research newsletter, Strategic Assets, is built to find: companies trading at low multiples of current free cash flow, carrying little or no debt, with strong earnings and a catalyst the market hasn't priced yet.

You Weren't Crazy 17 Years Ago You Were Early

You Weren't Crazy 17 Years Ago. You Were Early

Notes From the Field By James Hickman (Simon Black / Sovereign Man) June 19, 2026

20 years ago, if you recognized how deep America's problems were, it was easy to feel like you were the crazy one.

Banks were handing out mortgages to people who plainly couldn't afford them. Wall Street bundled those mortgages by the millions and sold them on as some of the safest investments around. And the whole structure rested on the assumption that home prices would never fall, so a bank could simply sell the home for more in case of a default.

You Weren't Crazy 17 Years Ago. You Were Early

Notes From the Field By James Hickman (Simon Black / Sovereign Man) June 19, 2026

20 years ago, if you recognized how deep America's problems were, it was easy to feel like you were the crazy one.

Banks were handing out mortgages to people who plainly couldn't afford them. Wall Street bundled those mortgages by the millions and sold them on as some of the safest investments around. And the whole structure rested on the assumption that home prices would never fall, so a bank could simply sell the home for more in case of a default.

Chief among the “experts” selling this fiction was Ben Bernanke, then chairman of the White House Council of Economic Advisers, who said in 2005, "We've never had a decline in house prices on a nationwide basis."

In March 2007, with subprime loans already going bad, Bernanke, by then Fed Chairman, told Congress the damage "seems likely to be contained."

That May he said he didn't expect "significant spillovers… to the rest of the economy."

As late as July 2008, weeks before the two mortgage giants collapsed into government hands, he called Fannie Mae and Freddie Mac adequately capitalized and in no danger of failing.

Then on September 15, 2008, Lehman Brothers filed the largest bankruptcy in US history, and the structure came down. Prices fell, those homes were suddenly worth less than the loans against them, and the safest investments around turned toxic.

By 2009, Washington was spending, bailing out, and printing at record scale, and the obvious question was how long it could possibly go on.

That was the world the very first Sovereign Man letter dropped into, in June 2009, exactly 17 years ago.

We wrote about a real man named William "Bud" Post who had gone flat broke, on food stamps, with lawsuits, jail time, and bankruptcy behind him. What made it strange was that in 1988 he'd won $16.2 million in the Pennsylvania lottery.

Bud, we wrote, is the United States of America.

America hit its own lottery after World War II, coming out the only major economy left standing, the dollar enthroned as the world's reserve currency. And like Bud, it spent the next several decades certain the money would never run out.

LBJ got bogged down in Vietnam while building the Great Society. George W. Bush entered two wars and told Americans to go shopping, and Obama, fresh off the bailouts, was promising universal healthcare.

It was the steady avoidance of every hard choice. We called it winner's syndrome: "we've been winners for so long we don't know any other reality."

In 2009, that was an unpopular thing to say.

The consensus treated the crisis as a stumble the economy would walk off, and calling America structurally broke got you labeled a crank.

We didn't say it was a death sentence, though. We argued the opposite, that clear thinking could still save America: take the hit, let failing businesses fail, restructure, and come out stronger.

"Unfortunately," we wrote, "there are no near-term indications of rationality in Washington."

17 years later, that is more true than ever. If anything, Washington has gone backwards.

For example, Social Security's own trustees now project the main retirement trust fund runs dry in 2032, after which scheduled benefits get cut by roughly 22% automatically.

That’s not some distant future where maybe at some point someone will have to start thinking about a solution. It is 6 years away.

And the fixes are no secret; the trustees themselves lay out the options, from higher payroll taxes to benefit cuts.

But they've ignored it for so long that simply hearing a few members of Congress acknowledge the scale of the problem now feels like progress, even though acknowledging it is a long way from fixing it.

We were early; the reckoning we kept warning about has taken longer to arrive than we thought.

But early isn't wrong: everything that first letter described is more true today than it was in 2009. Washington could still choose to fix it, exactly as it could have back then. It simply has to want to, and seventeen years of evidence says it doesn't.

Your Plan B, fortunately, doesn't require Congress to find its courage.

And that was the entire reason this company was founded.

That was the promise at the end of that first letter: while the country may be on a slide, clear thinking could still save you, "and that's where we come in."

That's still exactly what we do.

Sovereign Man grew into Schiff Sovereign, and one daily letter became a full body of research.

Every month, our co-founder James Hickman gives his in-depth view of the world in the Macro Brief, mapping where the debt, the dollar, and global events are heading. He points to specific real assets that can protect your savings; the gold, energy, and resource businesses that hold their value as the dollar slips.

It’s available to members of Premium

Members of our flagship membership, Plan B Confidential, get even more.

This is the original idea the first letter was built on: don't put all your eggs in one basket, and don't hand one government the keys to your entire life. Plan B Confidential is the playbook for second citizenship so you always have another way out, foreign residency so you always have another place to live, offshore banking so your savings aren't trapped in one banking system, and the legal tax strategy that lets you keep as much of your money as possible.

It's built on boots-on-the-ground research across more than 120 countries.

And because so much of the threat from a bankrupt government printing money and draining the value of your savings is financial, we've zeroed in on real assets through our investment research newsletter, Strategic Assets.

A real asset is something with worth of its own, the kind of thing people need no matter what the dollar is doing: gold as a store of value, energy, the metals that build everything. A government can print money by the trillion, but it can't print an ounce of gold or a barrel of oil, so real assets tend to hold their value, and often climb, exactly when paper money is falling apart.

And for readers who want it all, we offer Total Access.

Members get everything we publish, from the macro analysis to the investment research, and all the international strategies in between.

But Total Access members also get the community: other members who they meet at in-person events, conferences, dinners, and most recently, small group boots-on-the-ground trips around the world.

From a superyacht along the Croatian coast to a trek through the Patagonian Andes, members explore the world together, and finally find their tribe in each other.

That's the part we could never have planned 17 years ago.

Back then, we wrote to a handful of people willing to question what everyone else accepted as obvious. You were one of them, or you found your way here since, because you see the world through that same lens.

That's what built this. Not us. You.

Here's to the next chapter.

The Schiff Sovereign Team

Congress Passed 133 Broadband Programs. Its Big Idea Is A 134th

Congress Passed 133 Broadband Programs. Its Big Idea Is A 134th

Notes from the Field By James Hickman (Simon Black / Sovereign Man) June 15, 2026

There are things that a free market will never do, and it’s usually for very good reasons. Running fiber-optic cable down a twelve-mile dirt road costs a fortune, and the handful of households scattered along that road will never pay enough in monthly bills to justify the cost of laying the cable.

That’s why private companies don't bother laying fiber in rural areas: the math doesn't work.

Congress Passed 133 Broadband Programs. Its Big Idea Is A 134th

Notes from the Field By James Hickman (Simon Black / Sovereign Man) June 15, 2026

There are things that a free market will never do, and it’s usually for very good reasons. Running fiber-optic cable down a twelve-mile dirt road costs a fortune, and the handful of households scattered along that road will never pay enough in monthly bills to justify the cost of laying the cable.

That’s why private companies don't bother laying fiber in rural areas: the math doesn't work.

But living out in the country is a choice— one that plenty of people gladly make. Some people value the space, the quiet, and the empty horizon far more than same-day Amazon delivery or 1 gigabit Internet.

And most people typically know about these trade-offs before they move out to the country. Urban and suburban conveniences are just that— conveniences. They are not inalienable “rights”. No one is entitled to fast internet.

Yet Congress has decided at least 133 times that fast Internet, is, in fact, a right. And one that they have decided to provide with your money.