10 Amazing Ways to Build Wealth at Any Age

10 Amazing Ways to Build Wealth at Any Age

Use these tools to build wealth, whether you're just starting out in life or trying to grow the money you've earned.

MTN Staff • August 29, 2022

Most of us aren’t born rich. Those of us who didn’t inherit millions can still take steps to build wealth.

We have more options today than our parents ever did. For example, we can get price comparisons in a flash thanks to the Internet – and the money we save can go toward wealth-building.

If we want to diversify our portfolios, there are plenty of creative (and safe) ways to invest. That’s true even if we’re just starting out in life or nearing retirement.

10 Amazing Ways to Build Wealth at Any Age

Use these tools to build wealth, whether you're just starting out in life or trying to grow the money you've earned.

MTN Staff • August 29, 2022

Most of us aren’t born rich. Those of us who didn’t inherit millions can still take steps to build wealth.

We have more options today than our parents ever did. For example, we can get price comparisons in a flash thanks to the Internet – and the money we save can go toward wealth-building.

If we want to diversify our portfolios, there are plenty of creative (and safe) ways to invest. That’s true even if we’re just starting out in life or nearing retirement.

Use the following tools to build your wealth at any age.

1. Diversify your wealth with gold

Putting all your money in one place – stocks, bonds, crypto, whatever – is a recipe for losing wealth, not building it. Diversification is key to financial security. Here’s an easy way to start: Buy gold and/or other precious metals from Goldco.

Gold is an essential ingredient for modern electronics – a pretty secure industry. Silver is, too, and Goldco gives up to $10,000 worth of it to those who open qualified accounts.

Paper currency is highly regulated by law, and more can always be printed without any true backing. But ever since humans first figured out how to turn shiny rocks into valuable commodities, precious metals have represented worldwide value.

Adding them to your investment portfolio is a step toward wealth. Should you need to take some of it back out, Goldco’s “Highest Price Buy-Back Guarantee” means you’ll get top dollar for your holdings.

Goldco is the only precious metals company personally recommended by Fox News personality Sean Hannity. The company also earned an A+ rating from the Better Business Bureau and an AAA rating from the Business Consumers Alliance. Satisfied customers on Trustpilot, Google Reviews, Trustlink and ConsumerAffairs.com give Goldco 5-star ratings.

2. Protect your home from unexpected costly repairs

To continue reading, please go to the original article here:

https://www.moneytalksnews.com/10-amazing-ways-to-build-wealth-at-any-age/

5 Real Reasons You Won't Reach Financial Independence

5 Real Reasons You Won't Reach Financial Independence

Jacob Schroeder May 17, 2021

We are not perfect, and those imperfections often manifest themselves in our finances. But never fall for the illusion that wealth is wholly dependent on your character and behavior.

To explain what I mean, let me ask: Have you met the Welfare Queen?

She is irresponsible and shameless, engaging in behavior counter-productive to financial self-reliance. She is a fraudster, gaming the system any way she can to receive tax-payer money and never work a day in her life. She is everything wrong about government largesse.

5 Real Reasons You Won't Reach Financial Independence

Jacob Schroeder May 17, 2021

We are not perfect, and those imperfections often manifest themselves in our finances. But never fall for the illusion that wealth is wholly dependent on your character and behavior.

To explain what I mean, let me ask: Have you met the Welfare Queen?

She is irresponsible and shameless, engaging in behavior counter-productive to financial self-reliance. She is a fraudster, gaming the system any way she can to receive tax-payer money and never work a day in her life. She is everything wrong about government largesse.

You've never met her and never will. She is not real. She is the fictionalized version of an exaggerated incident. The Welfare Queen is a subversive trope, famously used by Ronald Reagan during his presidential campaign to criticize welfare programs. Do some people take advantage of federal programs? Absolutely. But it is disingenuous to portray some infractions as the norm.

Caricatures, like the Welfare Queen, are a way to tell a simple, clear story. They are also a way to charge the emotions of a desired group of people.

At their best, caricatures can help people easily understand complex topics. At their worst, they can advance harmful, racist ideologies. At their not worst but not good either, they can purposefully exclude important variables and create false impressions. As it is in personal finance.

Self-anointed financial gurus like to rail against their own trope: the hapless saver who will never achieve financial independence because of unaddressed character flaws and financially irresponsible behavior. It's almost a form of wealth shaming.

The reason, they say, so many people don't save enough for retirement is personal choices. Coincidentally, the solution for improving your behavior and growing rich is to buy their books, sign up for their courses and dish out loads of money to attend their conferences.

But that's not the real story any more than the Welfare Queen is. Maybe this caricature needs a royal name, too. How about the Wealth Jester? The person who is susceptible to foolish financial gestures that puts their future in jeopardy.

The truth is there are a variety of factors at play when it comes to building wealth. Certainly, personal decisions and habits make a difference. We, however, are also faced with forces that are far beyond our control. To think otherwise is to wrongfully fall for the Wealth Jester narrative.

Here are five bigger reasons people are unable to achieve financial independence.

1. Don't earn enough money

How is it all your fault if wages are set so low you can't save?

The ugly reality is that many people simply do not earn enough to become financially independent. Once the bare necessities are covered, there is little left over.

Less than 40% of American households have the means to cover an unexpected $1,000 expense -- much less build a nest egg.

To continue reading, please go to the original article here:

https://rootofall.substack.com/p/5-real-reasons-you-wont-reach-financial-independence

Financial Steps Proven To Improve Your State Of Mind

Financial Steps Proven To Improve Your State Of Mind

Mood Follows Action Jacob Schroeder Feb 18

What if we have the psychology of money backward? Psychological research from the likes of various Nobel Prize winners has shown how emotions shape our financial behaviors, which has turned our focus toward changing the way we think to make better financial decisions. But the truth may be that changing our mental state starts with changing our actions. Perhaps, money can’t exactly buy happiness, but the way we use it can indeed improve our emotional well-being.

Watch sports on any given night and you’ll hear commentators spew an assortment of cliches to explain the outcome of a game: “They were more motivated.” “They had more passion.” And, my personal favorite: “They wanted it more.” Whatever “it” is.

Financial Steps Proven To Improve Your State Of Mind

Mood Follows Action By Jacob Schroeder Feb 18

What if we have the psychology of money backward? Psychological research from the likes of various Nobel Prize winners has shown how emotions shape our financial behaviors, which has turned our focus toward changing the way we think to make better financial decisions. But the truth may be that changing our mental state starts with changing our actions. Perhaps, money can’t exactly buy happiness, but the way we use it can indeed improve our emotional well-being.

Watch sports on any given night and you’ll hear commentators spew an assortment of cliches to explain the outcome of a game: “They were more motivated.” “They had more passion.” And, my personal favorite: “They wanted it more.” Whatever “it” is.

While such talk can make for a good story, it’s a whole lot of journalistic B.S. As if championships are won on feelings. Athletes don’t play better because they spend more time happily thinking about winning than their opponents. Moods matter; actions matter more.

Yet, we often put the emphasis on our feelings. If only I had the motivation, I’d exercise more. If only I felt inspired, I’d write that novel. If I were more driven, my business idea would take off.

Certainly, mentality plays a role in all we do. Except we can’t control our thoughts or emotions as well as we like to think. For example, do not, I repeat, do not think of the number 23. See what I mean?

We have the calculus all wrong. It’s our actions that shape our emotions. As endurance athlete and wellness advocate Rich Roll puts it: Mood follows action. This maxim was supported by neuroscientist Andrew Huberman, who told Rich Roll on his podcast:

“Our feelings and our thoughts and our memories and all that is very complicated. But our behaviors are very concrete and they are the control panel for the rest of it… when it comes to wanting to shift the way that you function, to get better or to perform better, or to show up better, or to move away from things like addictive behaviors, it’s absolutely foolish for any of us to think that we can do that by changing our thoughts first. It’s behavior first, thoughts, feelings and perceptions follow.”

It works in sports. After making the varsity basketball team, Michael Jordan didn’t set out to prove everyone wrong by thinking of himself as the greatest of all time. Hundreds of practice shots each day convinced him that he was the greatest.

It works in art. What separates successful writers apart isn’t so much a deeper well of creativity but rather consistency. They show up to work whether inspiration strikes or not. As E.B. White said: “A writer who waits for ideal conditions under which to work will die without putting a word on paper.”

And, it works with money. Warren Buffett doesn’t simply wake up with more knowledge about businesses and markets than yesterday. He goes to bed with more knowledge about businesses and markets than yesterday after having read around 500 pages over six hours.

Thanks to the field of behavioral economics, we know certain mental errors, from confirmation bias to the Dunning-Kruger effect, can cause us to make choices that are not in our best interest. However, many proposed solutions focus on the futile task of changing the way we think. Don’t panic! Think long term! Ignore the noise!

Instead, studies show that the actions we take with money are what ultimately shape our feelings about money. Here are some financial actions that can improve your financial state of mind – and even your overall well-being.

To continue reading, please go to the original article here:

The Relationship Between Money and Marriage

The Relationship Between Money and Marriage

Jacob Schroeder Oct 12, 2021

I love scotch; she hates it.

There are many things my wife and I don't agree on, but money isn't one of them. We are intentional spenders, buying only what mutually aligns with our needs or values. For instance, disinterested in paying for the trappings of an ostentatious wedding, we tied the knot at New York's City Hall; our reception was watching our first son play at a public playground in the East Village on a warm fall afternoon.

We've been happily together for 16 years, which makes me wonder: Does love make the financial side of marriage work, or is it the other way around?

The Relationship Between Money and Marriage

Jacob Schroeder Oct 12, 2021

I love scotch; she hates it.

There are many things my wife and I don't agree on, but money isn't one of them. We are intentional spenders, buying only what mutually aligns with our needs or values. For instance, disinterested in paying for the trappings of an ostentatious wedding, we tied the knot at New York's City Hall; our reception was watching our first son play at a public playground in the East Village on a warm fall afternoon.

We've been happily together for 16 years, which makes me wonder: Does love make the financial side of marriage work, or is it the other way around?

The most important decision you'll ever make

Warren Buffett's financial wealth is only rivaled by his wealth of wisdom. Rarely does a day pass without someone in the finance industry quoting the Oracle of Omaha on social media. Heck, Warren Buffett's influence is so great, people have essentially made careers out of quoting him.

Yet, with all of his knowledge on investing and business, he says the most important decision a person can make has nothing to do with investing and business. At the 2009 Berkshire Hathaway annual meeting, he said:

“Marry the right person. I’m serious about that. It will make more difference in your life. It will change your aspirations, all kinds of things.”

You don't make it to Buffett's level of stature with a track record of being wrong often, and researchers seem to agree with him on this point. Studies show that marrying the right person can significantly improve our health, career success and wealth.

Marriage will change you in many ways. By definition, marriage -- joining two into one -- is disruptive. Often, for the better. It is about pursuing new things while sacrificing others. A major contributor to that disruption though is money.

Although we've long moved on from the ancient practice of marrying for the sake of status, money is an irrevocable part of marriage, at times, for better, and at times, for worse. Here is what research has uncovered about the relationship between money and marriage.

The relationship between money and marriage

Married people are wealthier than single people.

A 2005 study tracking people in their 20s, 30s and 40s found that married people experienced a 77% increase in wealth over single people. In fact, married individuals in the study saw their wealth rise 16% for each year of marriage. This makes sense considering married couples can combine incomes and share expenses.

However, it may not tell the whole story. You can't expect to tie the knot and just start watching the money roll right in. More affluent people are more likelier to get married in the first place. A report by the American Enterprise Institute details the wide gap in marriage rates by income. About a quarter of “poor” adults aged 18 to 55 are currently married, compared to 56% of middle- and upper-class adults.

Wealthier couples are happier.

A study published in the Journal of Happiness Studies suggests that married individuals are generally happier than the unmarried.

What about happiness among married couples?

To continue reading, please go to the original article here:

https://rootofall.substack.com/p/the-relationship-between-money-and-marriage

One Thing to Remember About Improving Your Financial Habits

One Thing to Remember About Improving Your Financial Habits

Jacob Schroeder Nov 23, 2021

Tired hands, young and old; tired hands to assemble each plastic piece and screw every tiny screw; tired hands to pull levers and activate conveyor belts; tired hands to pack cardboard boxes and stack containers on steel ships; tired hands to navigate the weathered steering wheel of a semi-truck; tired hands to deliver it to my doorstep; all of which is jumpstarted by a performative gesture as a consumer with a well-rested index finger on a digital button.

It is the cycle of a normal holiday shopping season. The only way to break it is to individually not participate.

One Thing to Remember About Improving Your Financial Habits

Jacob Schroeder Nov 23, 2021

Tired hands, young and old; tired hands to assemble each plastic piece and screw every tiny screw; tired hands to pull levers and activate conveyor belts; tired hands to pack cardboard boxes and stack containers on steel ships; tired hands to navigate the weathered steering wheel of a semi-truck; tired hands to deliver it to my doorstep; all of which is jumpstarted by a performative gesture as a consumer with a well-rested index finger on a digital button.

It is the cycle of a normal holiday shopping season. The only way to break it is to individually not participate.

Often, what is most effective in changing our habits for the better isn't a stroke of good luck but a nice, serious crisis. But whether or not it does greatly depends on single decisions, which are what make up our virtues. Habits and virtues, after all, can't be turned on and off; they take practice.

As we near the end of year two of COVID, perhaps the pandemic hasn't changed our financial behaviors as much as we first thought.

I have never shopped on Black Friday. I just would rather feel as if my head has been stomped on because of too much wine during Thanksgiving dinner than actually have my head stomped on for a flat screen TV. Though I certainly don't look down upon those who do.

Except this year, it may be an opportunity to recommit to the financial habits we adopted at the peak of the pandemic. Because it also is a decision to make for the better, and you never want to let a Black Friday go to waste.

Barack Obama's reward for winning the 2008 presidential election was responsibility over the worst economic crisis since the Great Depression. At the time, his chief of staff, Rahm Emanuel, said, "You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before."

To view a crisis as an opportunity is a tenet rooted ancient philosophy, as echoed by Roman emperor and Stoic philosopher Marcus Aurelius: "Just as nature takes every obstacle, every impediment, and works around it...so, too, a rational being can turn each setback into raw material and use it to achieve its goal."

To continue reading, please go to the original article here:

https://rootofall.substack.com/p/one-thing-to-remember-about-improving-your-financial-habits

7 Nice Ways to Tell Your Spendy Friends You're Staying on Budget

7 Nice Ways to Tell Your Spendy Friends You're Staying on Budget

By Mikey Rox

Unless you're invited to hang out at a friend's house, social invitations typically require spending money — going to the movies, grabbing a bite to eat, hitting an amusement park.

Ignoring an invite or saying that you're busy can get you off the hook, but friends might get suspicious if you pull the same excuse over and over. (See also: Is Peer Pressure Keeping You Poor?)

You don't have to justify your reasons for not spending. But if you don't want friends or relatives to get the wrong idea or think that you're avoiding them, a simple explanation goes a long way. Whether you're on a financial fast or have other plans for your money, there are friendly ways to tell someone you don't want to spend money.

7 Nice Ways to Tell Your Spendy Friends You're Staying on Budget

By Mikey Rox

Unless you're invited to hang out at a friend's house, social invitations typically require spending money — going to the movies, grabbing a bite to eat, hitting an amusement park.

Ignoring an invite or saying that you're busy can get you off the hook, but friends might get suspicious if you pull the same excuse over and over. (See also: Is Peer Pressure Keeping You Poor?)

You don't have to justify your reasons for not spending. But if you don't want friends or relatives to get the wrong idea or think that you're avoiding them, a simple explanation goes a long way. Whether you're on a financial fast or have other plans for your money, there are friendly ways to tell someone you don't want to spend money.

1. I'm Saving Up for the Holidays

It doesn't matter if you're buying gifts for family or taking a vacation, planning for the holiday season is a good reason (and good excuse) to scale back on spending. And since many people feel the pinch during the holidays, those in your social circle will likely understand your reasoning, and won't give you a hard time for turning down pricey invitations.

2. I'm Trying to Stick to My Budget

Saying, "I'm on a budget" is one way to say you're broke without actually uttering the word. But even when you have extra money, budgeting can prevent overspending.

If you receive an invitation to join friends at a restaurant, or if you're invited to a network marketing sales party, be honest and let the host know that extra spending isn't in the budget right now. This doesn't necessarily suggest that you don't have money, but that you're careful with how you spend your pennies. Your willpower might rub off on others.

3. I Have New Responsibilities

Social invitations can go beyond dinner and a movie, and your friends might plan a vacation together or suggest a shopping trip in the city. A responsible adult counts the cost before any large purchase.

And if you have new responsibilities or financial obligations (such as you've started a family or recently purchased a home), now may not be the best time to spend money on an expensive adventure.

If you're the first one in your group to have children or buy a house, you might need to kindly remind your friends how these changes impact personal finances. And remember: specifics count here. So if you feel comfortable, feel free to go into detail about said new responsibilities.

To continue reading, please go to the original article here:

http://www.wisebread.com/7-nice-ways-to-tell-your-spendy-friends-youre-staying-on-budget?ref=seealso

Is Peer Pressure Keeping You Poor?

Is Peer Pressure Keeping You Poor?

By Max Wong

Like every other Wise Bread writer, I hate debt. Although my debt doesn’t keep me awake at night, it is one of the things I think about while brushing my teeth every morning. “What will I do today (brush-brush) that will help me pay down (brush) my home mortgage ahead of (brush) schedule?”

The idea that “many people would rather struggle to pay off a large credit card bill than utter the phrase 'I can’t afford it,'” tests the limits of my financial imagination like a velociraptor tests an electric fence.

Is Peer Pressure Keeping You Poor?

By Max Wong

Like every other Wise Bread writer, I hate debt. Although my debt doesn’t keep me awake at night, it is one of the things I think about while brushing my teeth every morning. “What will I do today (brush-brush) that will help me pay down (brush) my home mortgage ahead of (brush) schedule?”

The idea that “many people would rather struggle to pay off a large credit card bill than utter the phrase 'I can’t afford it,'” tests the limits of my financial imagination like a velociraptor tests an electric fence.

It’s so painful, yet I can’t stop thinking about it. Spending money that you don’t have is a type of self-harm that often goes undetected and can have lifelong consequences. (See also: The Enemies of Frugality)

The Positive Power of "I Can't Afford That"

I am grateful that I figured out early on that people who judged me for saying “I can’t afford that” were the same people who were secretly living with crushing amounts of credit debt and didn’t own anything.

I think most emotionally mature people realize that friends and family who make you feel bad about how much money you have are not nice people, but even armed with that knowledge, there is still so much peer pressure to spend.

One of the hardest things about not having financial parity with the people around you is turning down invitations to events that are out of your budget range. Being in debt can be isolating.

In addition to missing out on weddings, nights on the town, or even schooling, friends who get turned down repeatedly might take your reluctance to spend money you don’t have as a personal rejection.

So, how do you talk about debt without losing all your friends? There must be at least a dozen ways that people manage their public spending vs. private debt, but I have four strategies that have worked for me personally.

Be Your Own Financial Cruise Director

Your debt is not your friends' problem to solve.

While your truly good friends will always listen to you complain about your financial woes, it’s not really up to them to make your life without money work. If you want to spend time with people you care about, suggest alternate, inexpensive ways of spending time with them:

If you can’t afford to go to a $10 gym class, suggest a morning hike or a run through the park to your sporty friends.

If you can’t afford dinner, ask to meet with your friends after dinner for a drink instead.

When I was really poor, I became the master social planner for everyone in my life because I would comb the weekly alternative newspaper for free concerts, book readings, art openings, and other events that I could invite my friends to.

Even if you live in a tiny town with no nightlife, there are plenty of free ways to spend time with your friends. For example, offer to go with them when they have to run all their boring errands. Or, hang out with them at school events for their kids. Do yourselves both a favor and schedule a cleaning day where you switch off helping each other clean your houses. Chores go faster when you have a friend to talk to.

Be Honest

To continue reading, please go to the original article here:

http://www.wisebread.com/is-peer-pressure-keeping-you-poor?ref=seealso

8 Money Lessons You Must Teach Your Children and Grandchildren

8 Money Lessons You Must Teach Your Children and Grandchildren

If you know and love a young person, pass on these life-changing lessons that can put anyone on the road to prosperity.

Kentin Waits • May 30, 2018

Around the nation, young people are graduating from high school and college and preparing to take charge of their financial lives.

If you listen closely, you can hear wallets groaning from coast to coast.

This is not another rant against millennials and other whippersnappers. Americans of all ages are hopelessly behind the curve when it comes to handling their money responsibly. Unless they have astute parents — or a natural interest in personal finance — young people are at a high risk of making financial mistakes that lead to chronic debt.

8 Money Lessons You Must Teach Your Children and Grandchildren

If you know and love a young person, pass on these life-changing lessons that can put anyone on the road to prosperity.

Kentin Waits • May 30, 2018

Around the nation, young people are graduating from high school and college and preparing to take charge of their financial lives.

If you listen closely, you can hear wallets groaning from coast to coast.

This is not another rant against millennials and other whippersnappers. Americans of all ages are hopelessly behind the curve when it comes to handling their money responsibly. Unless they have astute parents — or a natural interest in personal finance — young people are at a high risk of making financial mistakes that lead to chronic debt.

Money Talks News is all about providing the financial education lacking in too many schools and families. So, pass on the following 8 lessons to a young person in your life — or read these tips yourself if you’re fortunate enough to be a young adult just starting out on your own.

1. Debt is a form of slavery

In the first quarter of 2018, household debt reached a record $13.21 trillion, according to the Federal Reserve Bank of New York. Household debt is now 18 percent higher than it was in the second quarter of 2013.

Imagine how all that debt might impact the life of the average debtor. What will happen if there is a job loss or an illness that health insurance does not cover? How much stress would you feel in that situation?

Debt, especially unsecured consumer debt, is a form of slavery. The debtor is beholden to the creditor because each day that the debt remains unpaid, interest charges pile up. Over time, it’s easy to see how the unchecked use of credit can erode wealth and foreclose opportunities.

2. Financially successful people live below their means

Financial success is usually the result of years of self-control, and a big part of that discipline involves living within or below your means. If every dollar that comes into your life has to go out, there’s little hope for getting ahead.

Work to keep your overhead lower than your income, pocket the difference and don’t let every bump in income mean a boost in lifestyle.

3. Pay yourself first

Learning to pay yourself first is an important part of financial security. Direct a healthy portion of your income into an IRA, a 401(k) plan or a savings account before your paycheck even hits your account. Otherwise, you’ll have to constantly fight the temptation to spend every dollar.

When you automate your savings and make that an unwavering part of your routine, it puts the twin forces of time and compounding interest on your side.

4. Forget about impressing the Joneses

To continue reading, please go to the original article here:

Why Aren’t Rich People Happier?

Why Aren’t Rich People Happier?

Posted April 22, 2022 by Ben Carlson

William “Bud” Post lived a hard life.

His mother died when he was young and his father later dropped him off at an orphanage. Post was a drifter for most of his life, doing odd jobs to stay afloat. When he purchased a lottery ticket in 1988, he had just $2.46 in his bank account. Lo and behold, it was a winning ticket — Post walked away with $16.2 million. That’s a life-changing amount of money but it didn’t have the desired effect.

Just five years later Post proclaimed, “Everybody dreams of winning money, but nobody realizes the nightmares that come out of the woodwork, or the problems.”

Why Aren’t Rich People Happier?

Posted April 22, 2022 by Ben Carlson

William “Bud” Post lived a hard life.

His mother died when he was young and his father later dropped him off at an orphanage. Post was a drifter for most of his life, doing odd jobs to stay afloat. When he purchased a lottery ticket in 1988, he had just $2.46 in his bank account. Lo and behold, it was a winning ticket — Post walked away with $16.2 million. That’s a life-changing amount of money but it didn’t have the desired effect.

Just five years later Post proclaimed, “Everybody dreams of winning money, but nobody realizes the nightmares that come out of the woodwork, or the problems.”

Post blew through the money with some investments in a restaurant and a fleet of used cars. He also purchased a plane even though he didn’t know how to fly it. A handful of ex-wives sued him. His own brother even hired a hitman to kill him so he could inherit the winnings (he was unsuccessful).

In a matter of months he was forced to file for bankruptcy, surviving on Social Security and food stamps until he died broke in 2006.

When asked about hitting the jackpot after it all went up in smoke, Post later admitted, “I wish it never happened. It was totally a nightmare. I was much happier when I was broke.”

Studies show lottery winners have been shown to be more susceptible to drug and alcohol abuse, depression, divorce, suicide, or estrangement from their family.

I was reminded of Post’s story after reading a recent Conor Sen take on tech billionaires:

I’m not saying these people are all going to blow through their money but it does seem like many of the tech elite who have seemingly “won” the game are increasingly unhappy or unsatisfied.

They spend their time on social media getting into squabbles with one another, complaining about politics or offering cynical takes on the state of the world.

It’s possible I’m reading too much into the Twitter personas of these billionaires but it makes sense.

Having that much money can solve a lot of problems but it also creates a new set of complications, especially when it happens so young.

Buffett didn’t become a billionaire until he was 56 years old. Many of today’s tech titans strike it rich when they’re in their 20s.

To continue reading, please go to the original article here:

https://awealthofcommonsense.com/2022/04/why-arent-rich-people-happier/

Who Wants to Be a Billionaire?

Who Wants to Be a Billionaire?

November 18, 2022 by Ben Carlson

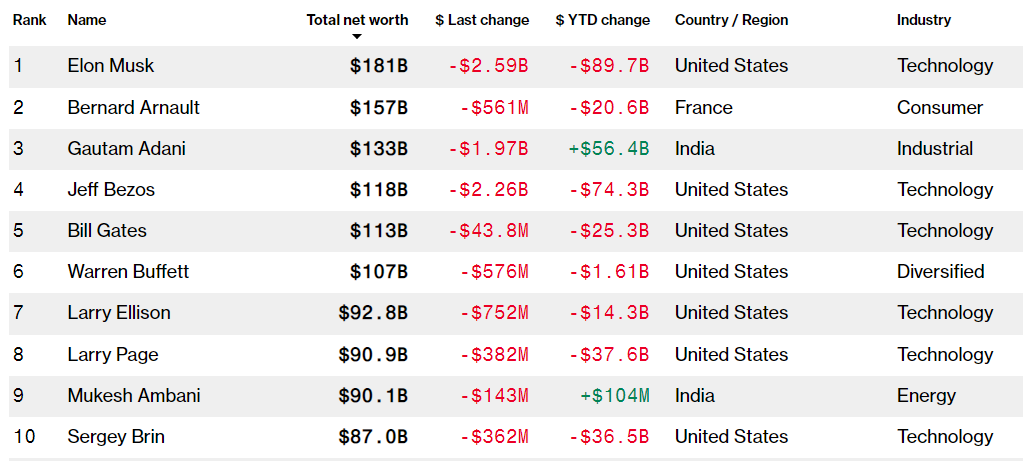

Scott Galloway once said, “It’s never been easier to become a billionaire, or harder to become a millionaire.” I’m not sure I agree but it does seem like more people want to become a billionaire these days. I honestly don’t think it’s worth it. More money in your life is obviously better than less money but only up to a certain point. Once you’re comfortable enough, more money these days seems to be more of a burden than a blessing. Just look at the list of the 10 richest people in the world right now:

Who Wants to Be a Billionaire?

November 18, 2022 by Ben Carlson

Scott Galloway once said, “It’s never been easier to become a billionaire, or harder to become a millionaire.” I’m not sure I agree but it does seem like more people want to become a billionaire these days. I honestly don’t think it’s worth it. More money in your life is obviously better than less money but only up to a certain point. Once you’re comfortable enough, more money these days seems to be more of a burden than a blessing. Just look at the list of the 10 richest people in the world right now:

Elon Musk has been divorced three times. Jeff Bezos is divorced. So in Bernard Arnault. And Bill Gates. And Sergey Brin. Warren Buffett split from his wife in an unusual arrangement where she left him and he took on a new partner. Larry Ellison has been divorced four times.

The 10 richest men in the world have a combined 12 divorces between them.

Even billions of dollars can’t buy you more stable relationships.

In fact, the opposite is probably true. More money and success likely make it harder to have healthy relationships because there is always more work to do and wealth to build.

The richest man in the world has admitted as much on a number of different occasions.

This week Elon Musk talked about the fact that he works from morning until night 7 days a week.2 He shared that being the richest person on the planet isn’t all it’s cracked up to be:

I’d be careful what you wish for. I’m not sure how many people would actually like to be me. They would like to be what they imagine being me, which is not the same thing as actually being me. The amount that I torture myself is next level, frankly.

Sure, the money sounds great, but would you actually want the richest man on the planet’s life?

I wouldn’t.

In a profile from the New York Times a few years ago, Musk shared that his work nearly made him miss his own brother’s wedding (where he was the best man). Running multiple companies makes it difficult to spend time with his children or take any days off:

Two days later, he was scheduled to be the best man at the wedding of his brother, Kimbal, in Catalonia. Mr. Musk said he flew directly there from the factory, arriving just two hours before the ceremony. Immediately afterward, he got back on the plane and returned straight to Tesla headquarters, where work on the mass-market Model 3 has been all consuming.

He said he had been working up to 120 hours a week recently — echoing the reason he cited in a recent public apology to an analyst whom he had berated. In the interview, Mr. Musk said he had not taken more than a week off since 2001, when he was bedridden with malaria.

“There were times when I didn’t leave the factory for three or four days — days when I didn’t go outside,” he said. “This has really come at the expense of seeing my kids. And seeing friends.”

The billions he’s made from those companies sound great until you realize all of the baggage that comes with it.

Listen, I am glad people like Elon Musk exist — people who create potentially life-altering companies like Tesla and SpaceX. I just can’t imagine wrecking my personal life in the process.

Money, power and fame can amplify who you are but they can also change you as a person.

To continue reading, please go to the original article here:

https://awealthofcommonsense.com/2022/11/who-wants-to-be-a-billionaire/

10 Types of Neighbors That Are Costing You Money

10 Types of Neighbors That Are Costing You Money

By Tim Lemke

I really like my nextdoor neighbor, Dave. He's quiet, friendly, and always willing to lend me his leaf blower. He also keeps his property in good shape Not everyone is so fortunate to have great neighbors like him. And that's a shame, because bad neighbors can not only make your life uncomfortable, they can cost you money. For your sake, I hope that none of your neighbors fit these descriptions.

The Slob

The grass and weeds are up to your knees. The house hasn't been painted in decades. There are rusted out cars on the front yard and trash all over the place. These types of neighbors can make your house less valuable, potentially costing you tens of thousands of dollars when the time comes to sell your home.

10 Types of Neighbors That Are Costing You Money

By Tim Lemke

I really like my nextdoor neighbor, Dave. He's quiet, friendly, and always willing to lend me his leaf blower. He also keeps his property in good shape Not everyone is so fortunate to have great neighbors like him. And that's a shame, because bad neighbors can not only make your life uncomfortable, they can cost you money. For your sake, I hope that none of your neighbors fit these descriptions.

The Slob

The grass and weeds are up to your knees. The house hasn't been painted in decades. There are rusted out cars on the front yard and trash all over the place. These types of neighbors can make your house less valuable, potentially costing you tens of thousands of dollars when the time comes to sell your home.

The Bad Borrower

It's certainly neighborly to let a person borrow your casserole dish or a pair of hedge clippers from time to time. But it's important to not let the borrowing become too one-sided. It's tough living next door to the people who are always asking for stuff, but rarely offering. It's also problematic when a neighbor returns items in bad condition — or not at all.

The HOA Cop

Many neighborhoods have rules that govern everything from the color of your balcony railing to whether you can hang laundry on a clothesline. Often, these rules are enforced by a homeowner's association or zoning department that can levy fines.

You should always try your best to keep your house and yard up to code, but no one wants a neighbor that rats you out every time your grass gets a millimeter too high or some leaves fill up your gutters, costing you money in the form of fines and repairs.

Mr. and Mrs. Litigious

Everyone has a right to protect themselves if they believe their legal or civil rights have been violated by a neighbor. But no one wants to live next to the person who calls up a lawyer every time a tree branch falls from your yard to theirs.

Unless there's truly illegal activity going on, the best neighbors try to resolve disputes by talking things out first. Maybe your dog chewed up your neighbor's flower beds. Maybe their faulty downspout led to a stream of water flooding into your backyard. Stuff happens, and more often than not these issues can be resolved without much rancor or legal fees involved.

The Party Animal

To continue reading, please go to the original article here:

http://www.wisebread.com/10-types-of-neighbors-that-are-costing-you-money?ref=seealso