How to Never Run Out of Money in Retirement

How to Never Run Out of Money in Retirement

APRIL 15, 2023 •White Coat Investor

Are you afraid of running out of money in retirement? Use these strategies to ensure this doesn't happen to you.

One of the greatest fears of many investors and retirees is that they will run out of money in retirement. However, there are many strategies available to ensure this doesn't happen to you. By employing one or more of these, you can dramatically decrease those odds.

How to Never Run Out of Money in Retirement

APRIL 15, 2023 •White Coat Investor

Are you afraid of running out of money in retirement? Use these strategies to ensure this doesn't happen to you.

One of the greatest fears of many investors and retirees is that they will run out of money in retirement. However, there are many strategies available to ensure this doesn't happen to you. By employing one or more of these, you can dramatically decrease those odds.

8 Ways to Ensure You Don't Run Out of Money in Retirement

The greatest financial task of your life is to save up enough money for retirement. However, some people don't quite make it. Or barely make it. Or have bad things happen to them. In spite of that, there are at least eight strategies that will still allow you to avoid running out of money. Choose one or more to apply in your life.

#1 Save More

This strategy is employed by many. The 4% “rule” suggests you save up about 25X your annual spending before retiring. However, there is no law that says you can't save up 30X, 33X, 40X, or even 50X. Obviously the more you have in relation to how much you spend, the less likely you are to run out of money.

#2 Spend Less (at Least Sometimes)

Here's another great strategy that works very well. Instead of saving more, you can simply spend less. Maybe you were planning to spend $100,000 per year in retirement, but if you can manage to spend just $80,000, you are far less likely to run out of money.

You can do this by downsizing or by moving to a lower cost of living area, or you can adjust how often you go out to eat, where you go on vacation, or what you drive in retirement. Lots of options.

But you don't actually have to spend less ALL the time. You really only have to spend less when your portfolio is doing poorly. This “variable withdrawal strategy” dramatically increases how much you can spend overall, even if it means sometimes you have to spend a little less. Having spending flexibility in retirement is very valuable.

#3 Only Spend Income

If you never actually touch your principal, you will never run out of money. That doesn't mean your nest egg, your income, and your spending will be stable or that it will even keep up with inflation, but it does mean you won't run out completely. Yet, this strategy can lead to potential errors.

Perhaps the greatest is that you'll end up spending much less than you could have spent—to some people, that just means they worked too long and saved too much. It can also lead someone to inappropriately invest in a high-yielding portfolio. Just because your income is higher doesn't mean your total return is higher or even positive. Often it leads people to work and invest differently.

They might be more interested in entrepreneurship and both direct and indirect real estate investing, for instance. Nothing wrong with that, but it does require a different set of skills and adds some risk, hassle, and (often) leverage.

#4 Spend Your Legacy

To continue reading, please go to the original article here:

https://passiveincomemd.com/how-to-never-run-out-of-money-in-retirement/

Who Do You Trust?

Who Do You Trust?

Casey Snyder | Apr 14, 2023 HumbleDollar

MORE THAN 92,000 people over age 60 reported losses to fraud totaling $1.7 billion in 2021, according to the FBI’s Internet Crime Complaint Center. That represented a 74% increase in losses from the year before.

With the population of older Americans growing, the need to protect this vulnerable population is more critical than ever. Enter the concept of a trusted contact.

Who Do You Trust?

Casey Snyder | Apr 14, 2023 HumbleDollar

MORE THAN 92,000 people over age 60 reported losses to fraud totaling $1.7 billion in 2021, according to the FBI’s Internet Crime Complaint Center. That represented a 74% increase in losses from the year before.

With the population of older Americans growing, the need to protect this vulnerable population is more critical than ever. Enter the concept of a trusted contact.

The trusted contact has its origin in a Financial Industry Regulatory Authority (FINRA) rule issued in March 2020. It urged registered investment advisors to ask clients to name someone the advisor can contact in case of suspicious activity. If you’ve opened a new investment account lately, you’ve probably been asked for a trusted contact.

FINRA defines the role this way: “A trusted contact is an individual authorized by an investor to be contacted by their financial firm in limited circumstances, such as concerns about activity in the investor’s account or if the firm has been unable to reach the investor after numerous attempts.”

Who might be named? It’s most often a family member, but it can also be an attorney, accountant or another reliable third party. Whoever it is, the intent is the same—to provide “another layer of security on the account and puts the financial firm in a better position to help keep the account safe,” in the words of FINRA CEO Robert Cook.

Financial industry veteran Ron Long said the trusted contact concept arose from numerous experiences in which advisors had clients who were requesting funds from their accounts to pay for obvious financial scams.

“Scammers often rely on victims succumbing to pressure to act fast and to avoid discussing the money disbursement with anyone,” said Long, a principal at Long Life Consulting of Seattle, who was previously the head of Aging Client Services at Wells Fargo.

“When an advisor is able to involve a trusted family member, often a son or daughter, they are able to speak with that loved one and successfully break the trance which the bad guy has over their parent,” Long said. “In other instances, the trusted contact acts as an ‘in case of emergency’ resource where an advisor observes signs of diminished capacity or has difficulty contacting an elder client.”

While the concept of a trusted contact is a step in the right direction, it’s not a substitute for a more comprehensive approach to safeguarding elders and their money. For one thing, the circumstances under which a financial firm is authorized to contact the trusted contact are limited, and don’t cover all the possible scenarios in which elder fraud might occur.

As demographics shift, and the demands on clients and their advisors expand, we need to evolve our approach to prevent elder fraud. This is especially important given the increasing rates of cognitive impairment among older Americans.

Here are five steps the public and financial professionals can take to defend those most vulnerable.

To continue reading, please go to the original article here:

Lessons From A Legend

Lessons From A Legend

13 Apr By The Financial Bodyguard

The investment management industry loves its legends and there is none bigger than the nonagenarian ‘Oracle of Omaha’ Warren Buffett, CEO of the US-listed firm Berkshire Hathaway. Over the years in that role Buffett has built a portfolio of directly held companies alongside a portfolio of listed stocks. Today, he is worth over US$100 billion and is the world’s fifth wealthiest person. In anyone’s eyes, he is a highly successful investor and is often held up as a beacon in support of an active, judgmental approach to investing.

Lessons From A Legend

13 Apr By The Financial Bodyguard

The investment management industry loves its legends and there is none bigger than the nonagenarian ‘Oracle of Omaha’ Warren Buffett, CEO of the US-listed firm Berkshire Hathaway. Over the years in that role Buffett has built a portfolio of directly held companies alongside a portfolio of listed stocks. Today, he is worth over US$100 billion and is the world’s fifth wealthiest person. In anyone’s eyes, he is a highly successful investor and is often held up as a beacon in support of an active, judgmental approach to investing.

Paradoxically, Warren Buffett’s legendary status as an active investor provides some useful lessons in support of adopting a systematic, low-cost approach to investing.

Lesson 1: Believe In The Power Of Capitalism And Compounding Over Time

Buffet understands capitalism and the powerful wealth generation that it can bring. He started investing in 1941 when he was 11 years old, and now at 92 years old, has over 80 years of compounding returns from the predominantly US companies he has owned. By the age of 39 he was worth US$25 million. His life story is fascinating[1].

‘The genius of the American economy, our emphasis on a meritocracy and a market system and a rule of law has enabled generation after generation to live better than their parents did.’

Lesson 2: Patience And Emotional Fortitude Are Key

Buffett expects to hold the companies for the long-term, much like an index fund.

‘Our favorite holding period is forever.’

He strives to avoid making decisions driven by emotions in response to short-term market pressures, such as the poor relative performance of value stocks from 2018-20 or equity market falls.

‘The most important quality for an investor is temperament, not intellect.’

Lesson 3: Active Management Is Not Easy

Despite his incredible business acumen, and consequent track record, it is not easy to continue to beat the market over time. He has always been a value oriented investor and was notorious in the run up to the tech crash of 2000-3, stating that he did not get it. He was to some extent proved right.

As Berkshire has grown, finding deals that will make a material difference to performance has become harder. His early years were spent trawling for individual investment opportunities. In those post-war years, information was scarce, professional investors represented a far lower part of the investor base, and markets were probably less efficient. If he was starting out again, would he be as successful? Who knows? And there’s the rub.

Take a look at the chart below, which illustrates 20-year rolling windows of Berkshire’s performance relative to a US equity index fund. It is evident that the huge success of the early days, has given way to far more trying times. Over the past 20 years, you could have achieved virtually the same return by investing in an S&P 500 index fund.

Figure 1: Buffet’s alpha – it is not so easy to win anymore

https://thefinancialbodyguard.com/wp-content/uploads/2023/04/Picture1-768x392.png

Source: Berkshire Hathaway Inc Class A, Vanguard 500 Index Investor Fund (VFINX) USD. Morningstar Direct ©

To continue reading, please go to the original article here:

How Much Money Does a Baby Need to Invest to Become a Millionaire?

How Much Money Does a Baby Need to Invest to Become a Millionaire?

APRIL 13, 2023 Financial Pilgrimage

Compound interest may be the most powerful personal finance-related topic out there. By combining time and money, a little bit today can be worth a whole lot more tomorrow. Most of us have heard about compound interest, but for me, when I sit down and run through the numbers, the power of compound interest blows my mind. In this post, we are going to look at a few examples that stress the importance of starting early, even really early. For example, what if these compound interest examples were taken to the extreme and we started investing for retirement at birth? Let’s take a look.

How Much Money Does a Baby Need to Invest to Become a Millionaire?

APRIL 13, 2023 Financial Pilgrimage

Compound interest may be the most powerful personal finance-related topic out there. By combining time and money, a little bit today can be worth a whole lot more tomorrow. Most of us have heard about compound interest, but for me, when I sit down and run through the numbers, the power of compound interest blows my mind. In this post, we are going to look at a few examples that stress the importance of starting early, even really early. For example, what if these compound interest examples were taken to the extreme and we started investing for retirement at birth? Let’s take a look.

Compound Interest Examples from Bill, Susan, and Chris

Before we get into the power of investing as a baby, let’s look at a few more realistic compound interest examples. The three individuals below are all in different stages of life.

Susan is a college professor who invests $5,000 per year in a stock-heavy retirement account for 10 years total between the ages of 25 and 35. In total, she invests $50,000 during this period. After age 35, Susan decides to begin investing in other assets and does not put any additional money into her retirement account.

Bill is a dietician who also invests $5,000 per year in an account similar to Susan’s but does so over a 30 year time period. Unlike Susan, Bill got a late start to investing and didn’t begin until age 35. He invested $150,000 total until the age of 65-years-old.

Chris is a lab technician who gets the best of both worlds by investing his $5,000 over the full 40 year period, beginning at age 25 and stopping at 65. In total, Chris invests $200,000.

Who do you think will end up with the most money? It’s pretty obvious that Chris will consider that he has the best of both worlds. But what about Susan and Bill?

Compound Interest Examples

CHART ASSUMES 7% GROWTH RATE. SOUCE: BUSINESS INSIDER VIA JPMORGAN.COM

https://financialpilgrimage.com/wp-content/uploads/2018/01/compound-interest-blog-post-9-768x577.png

The main takeaway from the chart is Susan ($602,070) ends up with more money than Bill ($540,741) even though she only invests for a period of 10 years while he invests for 30 years. They invest the same amount of money annually yet the difference is Susan starts investing at the age of 25 (and then stops after 10 years) and Bill starts at the age of 35 and invests until retirement. So, Susan’s 10 years of investing beats Bill’s 30 years since she started at 25 and Bill started at 35.

This is an oversimplified example. In a real-life situation, investments would likely change from year-to-year, hopefully increasing over time. The interest rate of 7% would fluctuate annually, especially with a portfolio heavily invested in stocks. However, the point here is to observe the power of compound interest over time.

To continue reading, please go to the original article here:

When Being Cautious Can Lead To More Risk

When Being Cautious Can Lead To More Risk

10 FEB Financial Bodyguard.com

Financial planning, as the name rather implies, is mostly about the future. Yes, sometimes it can help to identify things which we should do now to make a positive change in our financial circumstances immediately but mostly it is about doing things, whether now or in the future, to help create a better future for ourselves.

In order to work out what these should be and when we should do them, we generally need to project forwards from our current circumstances. This will provide some insights into how feasible our goals are and also highlight where potential roadblocks might occur.

When Being Cautious Can Lead To More Risk

10 FEB Financial Bodyguard.com

Financial planning, as the name rather implies, is mostly about the future. Yes, sometimes it can help to identify things which we should do now to make a positive change in our financial circumstances immediately but mostly it is about doing things, whether now or in the future, to help create a better future for ourselves.

In order to work out what these should be and when we should do them, we generally need to project forwards from our current circumstances. This will provide some insights into how feasible our goals are and also highlight where potential roadblocks might occur.

For example, it is all well and good to see that our resources are projected to be sufficient to meet all our objectives over the next 40 years but if we are likely to run out of liquid assets in the next five years then we might need to change something to avoid that happening.

There are essentially two elements to such a projection – the knowledge of our existing assets, liabilities, income and expenditure and the extent to which these are expected to change over our desired time horizon; in most cases this will be our lifetime.

For those of us not fortunate enough to be able to see the future with perfect clarity, the latter element will require some degree of assumption about how things are likely to develop over time.

How to derive these assumptions and what they should be are issues which absorb the attention of professionals involved in the field because, particularly over long periods, they can have a huge impact on the projected outcome even where the rates are apparently small.

For example, projecting an expenditure of £10,000 at an annual rate of 4.5% rather than 5% results in a difference of more than £12,000 a year after 40 years.

In reality, we have no idea how accurate our assumptions will be as the future is, as ever, unknowable. How many forecasters predicted the timing or impact of either a global pandemic in 2020 or a war in Ukraine in 2022?

Given the impact of getting such assumptions wrong, of which the worst could be running out of resources unexpectedly, it is not hard to see the temptation to adjust our assumptions with a view to being ‘cautious’. This might entail increasing incrementally the assumed rate at which expenditure increases and/or reducing the assumed return earned on invested assets.

However,

To continue reading, please go to the original article here:

https://thefinancialbodyguard.com/when-being-cautious-can-lead-to-more-risk/

Statistical Sobriety

Statistical Sobriety

January 11, 2023 by Anthony Isola

If your financial plan relies on winning the lottery or day trading – It’s time to find a new plan. Why do people count on the improbable regarding wealth creation?

Putting human emotion aside (Easier said than done), ignoring probability and statistics tops the list.

In 1986 the American Physical Society, the primary organization of our nation’s physicists, encountered a scheduling conflict.

Initially scheduled for San Diego, their convention event was switched to Las Vegas. Four thousand physicists piled into the MGM Grand Marina.

Statistical Sobriety

January 11, 2023 by Anthony Isola

If your financial plan relies on winning the lottery or day trading – It’s time to find a new plan. Why do people count on the improbable regarding wealth creation?

Putting human emotion aside (Easier said than done), ignoring probability and statistics tops the list.

In 1986 the American Physical Society, the primary organization of our nation’s physicists, encountered a scheduling conflict.

Initially scheduled for San Diego, their convention event was switched to Las Vegas. Four thousand physicists piled into the MGM Grand Marina.

That’s when things got interesting. During the physicist’s siege, MGM had its worst week – ever. Many would guess that these brainiacs were expert poker, roulette, or craps players due to their stratospheric I.Q.s.

That wasn’t the case. Mathematics kept their wallets full. They knew the odds and refused to play. By American standards, this is a Black Swan; in 2021, Casino revenue reached an all-time high of $45 Billion!

Likely, this group doesn’t partake in another of America’s favorite pastimes, playing the lottery. We spend $100 Billion yearly in this doomed quest to become rich and famous.

Advertisers know our Kryptonite. It’s not in their playbook to display their product’s effectiveness statistics. Celebrity endorsements provide the bait. During last year’s Super Bowl, Crypto Ads were all the rage.

Matt Damon insulted the manhood of millions by mocking their fear of uncertainty and the potential wealth of digital coins. We know how this turned out for the Crypto Bros.

Stock investors fall for the same fallacies. Ignoring probabilities shouldn’t be a part of anyone’s financial portfolio.

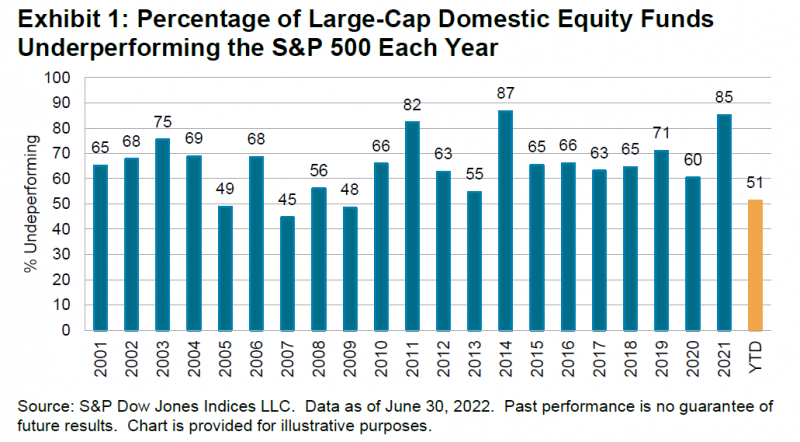

Even the so-called experts fall prey to a lottery mentality. Ignore index funds at your peril.

SPIVA data confirm these findings.

What’s the solution to this madness?

To continue reading, please go to the original article here:

Seven Alternative Facts about your Money

Seven Alternative Facts about your Money

by Anthony Isola

People love to use words and expressions to cloud their real intentions. Often these expressions can cloak lies and make you feel better about doing something that is just plain awful.

George Orwell wrote about how governments can mask some pretty nasty stuff with word tricks.

In our time, political speech and writing are largely the defense of the indefensible. Defenseless villages are bombarded from the air; the inhabitants, driven out into the countryside; the cattle machine gunned; the huts set on fire with incendiary bullets. This is called pacification.

Seven Alternative Facts about your Money

by Anthony Isola

People love to use words and expressions to cloud their real intentions. Often these expressions can cloak lies and make you feel better about doing something that is just plain awful.

George Orwell wrote about how governments can mask some pretty nasty stuff with word tricks.

In our time, political speech and writing are largely the defense of the indefensible. Defenseless villages are bombarded from the air; the inhabitants, driven out into the countryside; the cattle machine gunned; the huts set on fire with incendiary bullets. This is called pacification.

People are imprisoned for years without trial, or shot in the back of the neck or sent to die of scurvy in Arctic lumber camps. This is called the elimination of unreliable elements.

Euphemisms can be very dangerous. They have the ability to confuse and mislead people who are unfamiliar with a situation. They can make something very bad look very good.

Money is a prime breeding ground for all manners of psychoses. Euphemisms often serve as a form of financial camouflage for our worst desires. They work silently to give us the feeling we are doing something productive when in reality the opposite is occurring.

Here are some common examples:

“I did a lot of research on this stock.”- Scientists do research using data. Choosing an investment because you saw some person you don’t know talk about it on T.V. for two minutes does not make you Marconi.

“I don’t have time to learn about my finances.” – No, you choose to do other things with your time. You may choose to spend your time watching T.V. for seven hours a day or mindlessly playing Candy Crush. Don’t confuse doing what you want to do, over doing what you don’t want to, as a lack of time.

“My house is a financial investment.” – Actually, things that pay YOU are considered to be an investment. When you have a mortgage, property taxes, and large upkeep costs, you are paying someone else. There is nothing wrong with home ownership, but don’t confuse it with something that is designed to beat inflation over long periods of time.

“I saved money because this was on sale.”- Buying something that you did not need is not saving money. You simply cut down your unnecessary spending by a small amount. Not exactly the best way to build up your savings account.

To continue reading, please go to the original article here:

https://tonyisola.com/2017/07/seven-alternative-facts-about-your-money/

How To Unlock Your Financial Creativity

How To Unlock Your Financial Creativity

April 12, 2023 by Anthony Isola

Exemplary financial advice springs from the least likely sources.

A case in point is music producer Rick Rubin. His book, The Creative Act, discusses unlocking creativity and maximizing productivity by applying easy-to-follow practical steps. Who would’ve thought the producer of artists ranging from Johnny Cash to the Beastie Boys may have a second career as a personal finance guru? There’s one verb that doesn’t apply to Rubin – Boring.

The same cannot be said for most verbiage written concerning personal finance. Jargon like Fixed Income, Equities, Duration, and others are a snooze/confuse fest waiting to happen.

How To Unlock Your Financial Creativity

April 12, 2023 by Anthony Isola

Exemplary financial advice springs from the least likely sources.

A case in point is music producer Rick Rubin. His book, The Creative Act, discusses unlocking creativity and maximizing productivity by applying easy-to-follow practical steps. Who would’ve thought the producer of artists ranging from Johnny Cash to the Beastie Boys may have a second career as a personal finance guru? There’s one verb that doesn’t apply to Rubin – Boring.

The same cannot be said for most verbiage written concerning personal finance. Jargon like Fixed Income, Equities, Duration, and others are a snooze/confuse fest waiting to happen.

https://tonyisola.com/wp-content/uploads/2023/04/image-52.png

Source: S.E.C.

Many of Rubins’s principles perfectly match managing money.

Simplicity is the key to brilliance. Rubin refers to himself as a reducer, not a producer. Ten tracks are better than thirty. Nothing is more hazardous to a financial plan than bringing in complicated and expensive investment products.

As my colleague Barry Ritholtz likes to say, Come for the underperformance and stay for the high fees. Constructing a straightforward budget and savings plan may not win any Grammy Awards, but it will finance your retirement.

Collaboration is essential, and the best ideas come from unexpected places. Rubin launched many artists’ careers into the stratosphere. Working as a team and accepting constructive criticism are prerequisites. Too many investors overestimate their risk tolerance and behavior management skills.

Finding the right financial planner, insurance, estate, and tax specialists accelerates wealth creation.

The biggest lesson I’ve learned in my career is to embrace failure and accept it as a part of the creative process. The music business is a microcosm of life. The only way to learn is through trial and error. Rubin is a supercharged audience member, not a musician. His failure to make it as a Rock Star turbocharged his producing career. Making mistakes is part of learning, but constantly repeating them is not.

Losing money on cockamamie investments or delaying a savings program are ubiquitous investing errors. Doubling down or giving up gets you nowhere. Learning and regrouping is the right path.

The greatest rewards come from taking risks.

To continue reading, please go to the original article here:

https://tonyisola.com/2023/04/how-to-unlock-your-financial-creativity/

Here’s How to Make Filing Easier

Here’s How to Make Filing Easier

Jail, Jury Duty & 4 Other Things People Would Rather Do Than Taxes: Here’s How to Make Filing Easier

Heather Taylor Mon, April 10, 2023 GoBankingRates

You may not enjoy filing your taxes, but do you dislike the process so much that you’d go to great lengths to get out of it?

In a GOBankingRates’ 2023 tax survey of 1,002 Americans, there were six activities overall that respondents said they would rather do than file their taxes. These include spending the weekend with their in-laws (25%), jury duty (14%), taking the ACT or SAT exam (13%), experiencing a canceled flight leading to a missed trip (11%), undergoing a root canal (11%) and spending the night in jail (8%).

Here’s How to Make Filing Easier

Jail, Jury Duty & 4 Other Things People Would Rather Do Than Taxes: Here’s How to Make Filing Easier

Heather Taylor Mon, April 10, 2023 GoBankingRates

You may not enjoy filing your taxes, but do you dislike the process so much that you’d go to great lengths to get out of it?

In a GOBankingRates’ 2023 tax survey of 1,002 Americans, there were six activities overall that respondents said they would rather do than file their taxes. These include spending the weekend with their in-laws (25%), jury duty (14%), taking the ACT or SAT exam (13%), experiencing a canceled flight leading to a missed trip (11%), undergoing a root canal (11%) and spending the night in jail (8%).

What has led this many Americans to choose root canals and jury duty over filing their taxes? Let’s look at why so many feel hate doing their taxes and what can be done to make the tax filing process easier.

What Makes Filing Taxes Scary?

If you’ve ever felt scared or nervous about filing your taxes, you might wonder what is causing you to feel this way. You could be filing a simple return and still experience some anxiety surrounding the process.

Robert Persichitte is a CPA and CFA at Delagify Financial. Taxes, Persichitte said, combine boredom with fear. While it’s not hard to understand the boredom aspect, there are two specific reasons why we’re scared of taxes:

If you make a mistake, you could suffer a significant consequence.

It’s easy to make mistakes.

Most people have a story to share about a relative, friend or someone who knows someone who received a surprise bill from the IRS. If you forget something or do something wrong, you may face serious financial consequences.

And of course, it’s fairly easy and common to make mistakes. Persichitte said most people don’t learn in school how to prepare their taxes. Most Americans only think about it once a year, widening the gap between filing periods and making the experience of filing even a simple return troublesome.

How To Make Filing Taxes Easier

To continue reading, please go to the original article here:

https://finance.yahoo.com/news/jail-jury-duty-4-other-170016486.html

Can A Bank Seize Funds From My Checking For My Credit Card Payment?

Can A Bank Seize Funds From My Checking For My Credit Card Payment?

April 11, 2023 by Poonkulali Thangavelu Bankrate

A bank cannot typically take money from your checking account to pay off your credit card debt

There are exceptions to this protection. For one, if the bank gets a court judgment against you that doesn’t rule out this offset, it could take your deposited money;In case you risk falling behind on card payments, negotiate with the issuer and look into other financial options so your credit score doesn’t take a hit”

Can A Bank Seize Funds From My Checking For My Credit Card Payment?

April 11, 2023 by Poonkulali Thangavelu Bankrate

A bank cannot typically take money from your checking account to pay off your credit card debt

There are exceptions to this protection. For one, if the bank gets a court judgment against you that doesn’t rule out this offset, it could take your deposited money;In case you risk falling behind on card payments, negotiate with the issuer and look into other financial options so your credit score doesn’t take a hit”

If you owe your friend money, you could pay for their meal at a restaurant. This is called offsetting and is another way of canceling out the debt. But what if you bank with an institution that is also the issuer of your credit card and owe the bank money on the card? Can the bank offset this debt by helping itself to the money you deposit in your account?

Banks Cannot Use Offset For Credit Card Payments

The Fair Credit Billing Act (FCBA), which protects consumers from unfair credit card billing practices, rules that banks cannot typically seize funds deposited into a consumer’s bank account to pay off their credit card. According to the FCBA, a “card issuer may not take any action to offset a cardholder’s indebtedness arising in connection with a consumer credit transaction under the relevant credit card plan against funds of the cardholder held on deposit with the card issuer.” The law recognizes that using an offset provision to go after your credit card debt would give the bank some leverage against you.

However, there are some exemptions to this rule that would allow a bank to take funds deposited to make your credit card payment. For one, you may have authorized your bank to pay off your credit card debt using the money in your checking account. For instance, you might have signed up for an automatic bill payment arrangement.

In spite of any such arrangement, though, if you dispute a credit card payment and ask the bank not to take the payment from your monies deposited, it would have to heed your request.

Court Order Could Allow Bank To Offset

There are other circumstances in which a bank could take money from your bank account to offset credit card debt. For one, the bank could go to court and get a judgment against you. If the judgment doesn’t rule out the offset approach, and there are no state or other laws that prohibit this action, the bank could take your money for the credit card debt.

And in case “the terms of a security agreement permitted the card issuer to place a hold on the funds,” that would also mean the bank can take your money to offset the credit card debt. However, a card issuer cannot routinely include terms in its credit card agreement that give it a security interest in a credit card consumer’s bank accounts.

To continue reading, please go to the original article here:

https://finance.yahoo.com/news/bank-seize-funds-checking-credit-110029387.html

Humanity Is On The Cusp Of A Giant (6x) Leap Forward

Humanity Is On The Cusp Of A Giant (6x) Leap Forward

April 11, 2023 Simon Black Sovereign Man.Com

On March 11, 2011, an earthquake in the Pacific Ocean caused a tsunami to strike Japan. You probably remember seeing this in the news, because, directly in the path of the tsunami sat the Fukushima nuclear power plant.

As the waves crashed into the reactors, the plant’s cooling systems lost power and the nuclear reactors overheated. Pressure built until explosions spewed radioactive materials into the environment.

Humanity Is On The Cusp Of A Giant (6x) Leap Forward

April 11, 2023 Simon Black Sovereign Man.Com

On March 11, 2011, an earthquake in the Pacific Ocean caused a tsunami to strike Japan. You probably remember seeing this in the news, because, directly in the path of the tsunami sat the Fukushima nuclear power plant.

As the waves crashed into the reactors, the plant’s cooling systems lost power and the nuclear reactors overheated. Pressure built until explosions spewed radioactive materials into the environment.

Now, Japan realized that the Fukishma nuclear accident was a major anomaly... and that the historical data clearly show that nuclear power is safe. So they moved on and continued investing in nuclear.

Yet half a world away, Germany decided to shut down its own nuclear power plants because of what happened in Fukishima... even though Germany is obviously not prone to tsunamis and rarely experiences severe earthquakes.

It was a knee jerk reaction— not at all based on “science”. And instead of investing in nuclear, Germany spent tens of billions of euros on far less efficient renewable power.

One key problem, of course, is that Germany didn’t plan on having a fully renewable energy grid unil more than 25 years later in 2038.

So in the meantime while they would be building wind and solar energy plants across Germany, they planned on filling their energy void by importing natural gas... from Russia.

You can obviously see where this is going.

Germany made an emotional decision to shut off its nuclear plants and instead opted to import natural gas from a known adversary.

And now that the Russian gas is no longer flowing, today Germany relies on burning coal to generate enough electricity.

Rather than admit they were completely wrong to phase out nuclear power, Germany has turned the clock back to the early 1900s when the skies were clouded with thick black smoke from coal-fuel power plants.

But in reality the German government is trying to take its people back into the Dark Ages.

Let me explain.

I’ve talked about the importance of energy for a society’s economic prosperity. Lack of abundant “cheap” energy is one of the major forces of civilization decline.

And when I say “cheap” energy, I’m talking about the “Energy Returned on Energy Invested”, or EROEI.

Prior to the Industrial Revolution, when wood was the world’s primary energy source, the EROEI was 5:1.

In other words, the amount of energy generated from burning wood was FIVE times as much as the energy required to gather the wood in the first place, i.e. to chop down trees, cut them up into logs, transport the wood, etc.

But eventually people discovered that coal was a far more efficient source of energy, with an EROEI of at least 10:1. So the same amount of effort to mine coal, transport it, burn it, etc. produced twice as much energy as wood.

Obviously being able to obtain twice as much energy from the same amount of effort creates a LOT of social benefit; it means that there are a lot of excess resources available to invest in growth and development.

It’s no accident that the discovery of more energy efficient fuel sources, coupled with the invention of machines that relied on those efficient fuel sources, launched a steady, upward trajectory in human prosperity.

And with the discovery of oil as a source of energy (with an EROEI of 30:1 or more), growth and development really started to take off.

But now governments want to take us backward, to less efficient energy sources.

When they talk about renewable and “clean” energy, they often forget that solar panels and windmills don’t just appear out of thin air. Massive amounts of resources go into mining and processing the rare metals and minerals required to build solar panels, windmills, and batteries.

And in the end, renewable sources of energy typically have an EROEI of 5:1 – about the same as burning wood.

So in a mathematical sense, the climate fanatics’ “solution” is to take us back to a Medieval-era level of energy efficiency.

This is a pretty big deal if you understand the clear link between energy efficiency and human prosperity. Inefficient energy means that a society has to use up the preponderance of its resources simply to sustain itself. There’s very little surplus or growth. And that’s largely the way human civilization subsisted for thousands of years.

Don’t get me wrong, I have nothing against clean energy. I am, however, against going back to the Dark Ages... which is essentially the “solution” that Germany and other advanced nations are proposing.

The obvious solution is nuclear power, which has a whopping 180:1 Energy Return on Energy Invested.

If the 2X increase in efficiency from transitioning from wood to coal set in motion the greatest growth of prosperity in human history, what do you think the 6X jump from fossil fuels to nuclear power would do?

And yet, because Greta Thunberg scowls at nuclear, governments want to cast society back to the stone age.

It’s crazy. Last November, the United Nations hosted a Climate Change Conference known as COP27. They talked about gender identity and taxing meat consumption. But they barely mentioned nuclear, which has lower carbon emissions than wind and solar, while delivering 36X more energy return

And this is why I call climate change the new ‘human sacrifice’.. Their policies are guaranteed to decrease efficiency, cost more money, stunt productivity, and trap more people in poverty...

... unless leaders finally get on board with nuclear.

The good news is that nuclear is inevitable. And we’re starting to see a shifting tide towards this obvious solution.

For example, when acclaimed Hollywood director Oliver Stone (who is a hard core leftist) was interviewed at the World Economic Forum last year, he slammed the climate elites for ignoring nuclear.

Stone is releasing a documentary called Nuclear Now arguing that nuclear energy is the best way to promote a cleaner environment without sacrificing productivity and quality of life.

Again, it’s obvious. There aren't enough resources to fully switch the world to inconsistent energy like wind and solar, to create the necessary batteries for storage.

Eventually people are going to wake up to that reality. And when they do, there is going to be a mad rush into nuclear energy.

That creates some very fertile ground for investing in the resources required for nuclear, such as uranium mining and refining.

Right now, the uranium industry is not receiving a ton of capital because of exaggerated fears of its dangers. When that changes, early investors in productive uranium companies with good leadership should do quite well.

I’m an optimist. I don’t think the future is going to be cold and dark with humans cast back into the Dark Ages.

I think when the world confronts the economic realities of energy scarcity, it will usher in a new renaissance in energy. We’ll all benefit. And the people who saw it coming will make a killing.

To your freedom, Simon Black, Founder Sovereign Man

https://www.sovereignman.com/trends/humanity-is-on-the-cusp-of-a-giant-6x-leap-forward-146739/