How The IRS Operates Is About To Undergo A Major Change

How The IRS Operates Is About To Undergo A Major Change. Here's what it means for you

Russ Wiles, Arizona Republic Sun, April 23, 2023 a

With the 2022 income-tax filing season mostly in the books, attention turns to the future. Next year’s filing season, and those beyond, could look and feel much different.

Following the passage of the Inflation Reduction Act in 2022, the Internal Revenue Service will receive nearly $80 billion in added funding from now through fiscal year 2031 to catch up with backlogs, hire more employees, implement 21st-century technology, go after increasingly sophisticated tax cheats and, in short, reinvent itself.

How The IRS Operates Is About To Undergo A Major Change. Here's what it means for you

Russ Wiles, Arizona Republic Sun, April 23, 2023 a

With the 2022 income-tax filing season mostly in the books, attention turns to the future. Next year’s filing season, and those beyond, could look and feel much different.

Following the passage of the Inflation Reduction Act in 2022, the Internal Revenue Service will receive nearly $80 billion in added funding from now through fiscal year 2031 to catch up with backlogs, hire more employees, implement 21st-century technology, go after increasingly sophisticated tax cheats and, in short, reinvent itself.

The agency released a Strategic Operating Plan in late March. It envisions significant change to improve taxpayer services, quickly resolve problems, use technology to operate more effectively, expand the workforce, improve its culture and collect a lot more money from corporations, partnerships and wealthy individuals.

If some of the proposals come to fruition, taxpayers could:

Receive real-time help from the IRS to identify potential mistakes and alerts for claiming overlooked deductions, before filing their returns.

Reach live IRS representatives quickly by phone or easily arrange meetings in local IRS offices.

Access their personal information more easily from the IRS website, including balances, payments and notices.

Get real-time updates on return processing, refunds, audits and personal interactions.

Find it easier to resolve past-due tax bills and arrange payments on balances owed.

Interact with the IRS with greater confidence that personal information and refund money will be protected.

Those are just a sampling of the more visible changes that taxpayers might see in coming years. It's a rare opportunity to modernize the IRS and make it more effective and efficient.

More money for a range of initiatives

The vision is to create “world-class customer service where taxpayers can engage with the IRS in a fully digital manner if they choose,” wrote new IRS Commissioner Daniel Werfel in a letter to Treasury Secretary Janet Yellen.

Helpful tools will better enable taxpayers to navigate the complexity of the tax system and interact, if necessary, with a customer-service staff that will be “maintained at the right size and with the right resources and training to always be ready to meet the taxpayer demand for assistance," he added.

To continue reading, please go to the original article here:

https://news.yahoo.com/irs-operates-undergo-major-change-140032742.html

The Worst Money Advice That Keeps Going Around

The Worst Money Advice That Keeps Going Around, According to Experts

Andrew Lisa Mon, April 24, 2023 GoBankingRates

Some of the most popular money advice is as unreliable as it is common. From social media drivel to well-intentioned counsel from industry professionals, money misinformation can come from anywhere.

Sometimes it's bad investment advice. Other times, it's misguided suggestions about saving, spending, borrowing or building credit. No matter the subject, all misleading money guidance has one thing in common -- it never helps the person on the receiving end.

The Worst Money Advice That Keeps Going Around, According to Experts

Andrew Lisa Mon, April 24, 2023 GoBankingRates

Some of the most popular money advice is as unreliable as it is common. From social media drivel to well-intentioned counsel from industry professionals, money misinformation can come from anywhere.

Sometimes it's bad investment advice. Other times, it's misguided suggestions about saving, spending, borrowing or building credit. No matter the subject, all misleading money guidance has one thing in common -- it never helps the person on the receiving end.

GOBankingRates asked a variety of experts to share the unsound financial advice they would most like to see go away. Their answers span all topics and categories, but they come to the same conclusion -- a lot of what you've been hearing about managing your finances is wrong.

Avoid the following bad money advice at all costs.

Carry a Balance To Improve Your Credit Score

You can improve your credit score by using credit cards responsibly, and the first rule of responsible credit card use is to pay your balance in full every month to avoid compounding finance charges. Some people, however, make the mistake of believing that you have to carry a revolving balance in order to reap the benefits -- which is exactly what you don't want to do.

"My boss proudly explained to me that she carries a credit card balance and pays interest on it in order to increase her credit score," said Martin Lassen, founder and CEO of GrammarHow. "She received this recommendation from her mortgage broker. It was suggested that she keep the balance between 40% and 50% of her credit limit. It's the worst financial advice I have ever received."

You Have Plenty of Time To Worry About Retirement

Credit card debt is so troublesome because of the snowball effect of compound interest. When you're saving instead of spending, however, compounding works in your favor by converting small contributions into a big retirement nest egg -- but only if you give it time to work its magic.

"When I was young, one of my friends advised me to stop worrying about retirement," said James Crawford, co-founder of Deal Drop. "He said I would have plenty of time to think about it later."

It's hardly unusual. People often hear that they should put off retirement planning to invest in something more immediate like a business. That's bad advice that will force them to save much more as their timeline grows shorter.

"It takes a long time for your money to increase," said Crawford. "You'll need to save less money over time if you get started early."

Invest In Actively Managed Funds

To continue reading, please go to the original article here:

https://finance.yahoo.com/news/worst-money-advice-keeps-going-110016373.html

Understanding Wants and Needs to Improve Your Finances

Understanding Wants and Needs to Improve Your Finances

Financial Pilgrimage

Whenever you open up a news site, go shopping or fill the gas in your car, it can remind you of how expensive everything is. Financial experts remind us to tighten our belts and watch our spending as the cost of living rises. If we’re not careful, we may be unable to afford to pay for our necessary expenses, let alone extras.

But, for many folks, drawing the line between what is necessary and what is nice to have is challenging. In other words, it can be challenging to differentiate needs from wants.

Understanding Wants and Needs to Improve Your Finances

Financial Pilgrimage

Whenever you open up a news site, go shopping or fill the gas in your car, it can remind you of how expensive everything is. Financial experts remind us to tighten our belts and watch our spending as the cost of living rises. If we’re not careful, we may be unable to afford to pay for our necessary expenses, let alone extras.

But, for many folks, drawing the line between what is necessary and what is nice to have is challenging. In other words, it can be challenging to differentiate needs from wants.

Understanding Wants and Needs

In the simplest terms, a need is something you require to live and function, while a want improves the quality of your life and that you enjoy having. Viewing wants and needs by this definition may seem easy to break down. You may think that needs would be the same for everyone and include things like food and shelter, and while it does on a fundamental level, it is more nuanced than this.

Examples of wants and needs often differ among individuals and families. You can attribute the differences to various factors like where you live and access to services.

Let’s look at a few examples.

Everyone would consider transportation a basic need. You need transportation to get to work, get your kids to school and run errands. However, if you live somewhere that has reliable public transport, you probably don’t need a car. Similarly, if where you live everything is within walking distance and it is safe to walk, you can go without a car. However, if there is no public transport or it’s unreliable or unsafe, and you live somewhere where it’s impossible to walk to where you need to go, you will need to buy a car.

So, you’ve established that a car is a need and that you will use it often. You will use it to go to work, take your kids to school and sporting events, and for all your other errands. So, what car do you get? You can get the cheapest car possible because you need to get from A to B, but an affordable car can come with problems.

It may not be safe as it has fewer safety features, and if you’re using it to transport your kids, this is a significant risk. Cheap vehicles may also come with other issues and may need lots of repairs costing you more in the long run. Lastly, if you have a big family, you probably need a big car to accommodate everyone. In this case, a more expensive vehicle is necessary for your life.

On the other hand, a cheaper car might suit your needs if you are a single person who only requires a vehicle to drive a short distance to work and won’t use it much.

If you’re struggling to establish whether something is a want or need, ask yourself if it’s possible to live and function without it. For example, can the need be met less expensively if you need it to live? Then think about what your life would be like without it.

The Best Way to Budget

To continue reading, please go to the original article here:

https://financialpilgrimage.com/understanding-wants-and-needs/

11 Mottos to Live By

11 Mottos to Live By

Marjorie Kondrack | Apr 21, 2023 HumbleDollar

LIVING BENEATH OUR means is one of the best habits to develop if we want a secure retirement. Like many others, I learned this sort of thrift from my parents and grandparents, who lived through the Great Depression and, by necessity, had to avoid waste.

Not only did our forebearers survive the Great Depression, but also the Second World War came right on its heels. These were years of conserving materials—such as metal, rubber, paper and food—to support the war effort.

11 Mottos to Live By

Marjorie Kondrack | Apr 21, 2023 HumbleDollar

LIVING BENEATH OUR means is one of the best habits to develop if we want a secure retirement. Like many others, I learned this sort of thrift from my parents and grandparents, who lived through the Great Depression and, by necessity, had to avoid waste.

Not only did our forebearers survive the Great Depression, but also the Second World War came right on its heels. These were years of conserving materials—such as metal, rubber, paper and food—to support the war effort.

My mother saved a food ration book from the war that still had some stamps in it. When she shopped, she had to hand the grocer stamps when buying meat, sugar, butter, cooking oil and canned goods. The number of stamps handed over depended on the scarcity of the item purchased. For instance, if bacon was 35 cents a pound, you might have to give the grocer seven stamps.

Once the stamps were used up for the month, people couldn’t buy any more of that food until new stamps were issued the following month. I wonder how many young people today know that, in this land of abundance, food was once rationed, and that thrift in itself can be a source of remarkable household revenue.

Mom also saved a booklet from the war years that gives information about saving or conserving just about everything—food, clothing, house furnishings, appliances, utilities, cars, even insurance. People found artful ways to scrimp on just about everything. Nothing was wasted.

We could all benefit from the advice in this little booklet. Here are 10 of the more memorable passages that appeared at the bottom of the booklet’s pages:

Willful waste makes woeful want.

te nothing. Hoard nothing. Use everything.

Spend what you must and save what you can.

He that eats and saves sets the table twice.

Waste nothing. Hoard nothing. Use everything.

Spend what you must and save what you can.

He that eats and saves sets the table twice.

To continue reading, please go to the original article here:

Class Worth Taking

Class Worth Taking

Greg Spears | Apr 20, 2023 HumbleDollar

LESS THAN HALF of Americans—46%—have tried to calculate how much they need to save to live comfortably in retirement, according to a 2022 survey by the Employee Benefit Research Institute. I often meet extremely bright people—doctors, residents, PhD students and professors—who say with a sheepish smile that they don’t understand the intricacies of their retirement plans.

For some, this lack of understanding is a choice. People who sense they haven’t saved enough, or any money at all, may not want to know where they stand financially. But arguably these and most other Americans have also been shortchanged. Personal finance is not a standard offering in the general education curriculum in the U.S. Last year, when I asked the students in my college economics class how many had previously taken a personal finance course, only one student out of 21 raised a hand.

Class Worth Taking

Greg Spears | Apr 20, 2023 HumbleDollar

LESS THAN HALF of Americans—46%—have tried to calculate how much they need to save to live comfortably in retirement, according to a 2022 survey by the Employee Benefit Research Institute. I often meet extremely bright people—doctors, residents, PhD students and professors—who say with a sheepish smile that they don’t understand the intricacies of their retirement plans.

For some, this lack of understanding is a choice. People who sense they haven’t saved enough, or any money at all, may not want to know where they stand financially. But arguably these and most other Americans have also been shortchanged. Personal finance is not a standard offering in the general education curriculum in the U.S. Last year, when I asked the students in my college economics class how many had previously taken a personal finance course, only one student out of 21 raised a hand.

This vacuum is worrying because so much rides on successfully budgeting, saving, investing and other financial decisions. Next Gen Personal Finance is a nonprofit group trying to fill that void. Its goal is to make sure every student who graduates high school has completed at least one personal finance class.

Thanks partly to the group’s lobbying, six states added a personal finance requirement for high school graduation in 2022. That brings to 18 the number of states that mandate personal finance study. Only 24% of U.S. public high school students currently receive finance education. That’s projected to rise to 40% thanks to the six additional states that just mandated a state-wide personal finance curriculum—Florida, Georgia, Kansas, Michigan, New Hampshire and South Carolina.

In the 32 states and the District of Columbia that lack a mandate, an average of just one student in 10 will take a personal finance class before graduating. In some cases, the local school district mandates a personal finance course. Most of the time, however, a money class is offered as an elective, folded into another subject like math—or it’s simply not offered at all.

To help build a personal finance curriculum, Next Gen provides school districts with free course materials and teacher training. Some 77,000 educators have been trained to teach a money curriculum, and around 20,000 more join annually, according to Tim Ranzetta, an entrepreneur from Palo Alto, California, who is Next Gen’s co-founder and chief financial backer.

Next Gen’s financial education curriculum is comprehensive. How to use credit cards. How to invest. Budgeting, taxes and insurance. And, perhaps most pertinent to high schoolers, how to afford college without sinking into a pit of debt.

“It’s about behavior change,” Ranzetta said in a telephone interview from California. After taking the class, he said, students “open up savings accounts. Set up Roth IRAs. Make better decisions on student loans.” Their knowledge can also be passed on to parents in a ripple effect. “Kids are taking this home to their families. Parents are signing up for IRAs after their son comes home” from class, Ranzetta added.

The absence of financial education is particularly acute among lower-income students. In school districts where 75% of students or more qualify for free or reduced-cost lunch, less than 5% of children are required to take a personal finance class to graduate, according to Next Gen’s research. These districts often lack the resources to add a new subject, Ranzetta said.

To continue reading, please go to the original article here:

When in Rome

When in Rome

Dennis Friedman | Apr 21, 2023 HumbleDollar

My wife and i visited Italy this year. We flew to Venice, where we stayed three days, and then hopped a train to Florence, where we spent the next five days. After that, we rented a car for three days and toured the Tuscany countryside, before catching a train to Rome for our final six days. I learned a lot about Italy, but I also learned some things about myself. Here are 11 takeaways from our trip:

1. Going home was one of my favorite parts. Before I retired, I thought I’d spend months on the road, and maybe even live overseas for a while. But after two or three weeks of traveling, I’m ready to go home.

When in Rome

Dennis Friedman | Apr 21, 2023 HumbleDollar

My wife and i visited Italy this year. We flew to Venice, where we stayed three days, and then hopped a train to Florence, where we spent the next five days. After that, we rented a car for three days and toured the Tuscany countryside, before catching a train to Rome for our final six days. I learned a lot about Italy, but I also learned some things about myself. Here are 11 takeaways from our trip:

1. Going home was one of my favorite parts. Before I retired, I thought I’d spend months on the road, and maybe even live overseas for a while. But after two or three weeks of traveling, I’m ready to go home.

I miss my home, friends and routine when I’m away for a while. I don’t see how people, no matter how much time they spend traveling, can sell their house and not have a place to go home to. I wouldn’t feel safe and secure.

2. If I’m going to travel and see everything I want to see, I better do it now. While we were in Florence, my wife and I climbed to the top of the dome that covers the Cathedral of Santa Maria del Fiore, also known as the Duomo. It was 463 steps to the top, and the passage is sometimes steep. There are many towers in Italy with breath-taking views that also involve climbing many steps.

I can’t see us being fit enough in our 80s to do things like that. Our 70s might be the last chance to travel without physical limitations.

3. Travel is not cheap. We have two more major trips planned this year. Funding these trips means drawing down our investment portfolio.

I don’t know if I’d have felt comfortable spending this much money on travel if I didn’t have a financial advisor giving me the thumbs up. That reassurance allows us to spend without fear that we’ll run out of money.

4. I wrote in another article about having only one credit card in our later years—how it would simplify our finances and make them easier to manage. I was wrong. We should have at least two credit cards.

My wife and I paid for almost everything in Italy by using credit cards. While dining at a restaurant in a small town in Tuscany, our credit card was rejected. We tried three times with no luck. I checked my Citi Mobile app and it was temporarily shut down for maintenance. Maybe that was the reason for the rejection.

Luckily, I brought another card with me—because we didn’t have enough euros to pay for the dinner. That’s another lesson I learned: Make sure you have enough local currency for emergencies, because you might not be able to charge everything to a credit card. For instance, we stayed at a hotel in a small town where we were required to pay part of the bill—the city taxes portion—in euros.

5. How to manage the exchange rate can be tricky.

To continue reading, please go to the original article here:

What To Do With Unexpected Money

What To Do With Unexpected Money

Larry Keller The Physician Philosopher

A lot of us have an idea of what we should do with money that we earn on a regular basis from our physician jobs. Oftentimes it goes towards our typical cost of living expenses: bills, debts, savings, investments. But what about money you get that you weren’t expecting?

Because yes, most of us will, at some point, get at least a little money that we didn’t expect. Regardless of the source – whether it’s an inheritance, a tax refund, or a bonus at work – we end up with one question.

What should we do with this extra money?

What To Do With Unexpected Money

Larry Keller The Physician Philosopher

A lot of us have an idea of what we should do with money that we earn on a regular basis from our physician jobs. Oftentimes it goes towards our typical cost of living expenses: bills, debts, savings, investments. But what about money you get that you weren’t expecting?

Because yes, most of us will, at some point, get at least a little money that we didn’t expect. Regardless of the source – whether it’s an inheritance, a tax refund, or a bonus at work – we end up with one question.

What should we do with this extra money?

Deciding on a plan for your extra money

I haven’t been fortunate enough to get an inheritance, but I have received bonuses from my job. In anesthesia at Wake Forest, we qualify for bonuses by working additional shifts, which I did for a few years to pay off student loans. Since then, as I’ve transitioned to working more on my business and not taking on extra shifts, I get nonclinical incentives for performing academic work.

When it comes to receiving extra money, it doesn’t have to be a large sum for you to be intentional about how you use it. Whether you’re getting extra money from a new bonus system implemented at work or you got a bigger tax refund than you were planning for, it helps to have a plan for how you want to put the extra money to use.

Apply the 10% rule for unexpected funds

The 10% rule is what I used when I first finished medical school. If my wife or I came into additional money, we would take 10% of it and spend it however we wanted to, guilt-free. This could be on anything you want: tennis issues, a television, a new sofa, a grill.

You can apply the same rule for an increase in pay. For example, if you make $4,000 per month post-tax as a resident, and it turns into $14,000, now you’ve got a $10,000 gap. Take $1000 a month and spend it on whatever you want.

But with that other 90%, I encourage you to lay a solid foundation: pay off student loans and start saving a significant portion of your money.

I paid $10,000 a month to pay off my student loans on average for the first 19 months after I finished training. So I really did take 90% of that extra money (working extra shifts and collecting bonuses by doing that) to pay off my student loans.

An option like a taxable brokerage account is an optimal way to invest some of that 90%. The money in these accounts is easier to access than retirement accounts, and it does actually offer certain tax advantages despite its name.

Five ways to use your unexpected funds

Spend it.

Save it.

Give it.

Invest it.

Pay debt.

Personal finance is personal. Many of us physicians have student loan debt, so maybe you’d use it to pay down some debt. Maybe you’re using it to pay down your mortgage or your car loan. The right answer for each person often varies, and it can vary even more based on your current stage of life.

Maybe when you were younger a lot of your extra money went towards your loans, but now you no longer have loans, and you’re able to spend or give or invest more of that money than you used to in the past.

Lisha’s value shift around handling extra money

To continue reading, please go to the original article here:

10 Harsh Money Lessons That You Never Learned in School

10 Harsh Money Lessons That You Never Learned in School

By Martin Dasko / STUDENOMICS

“They should teach personal finance in college.”

“I wish I learned more about money in school instead of studying all that useless stuff.”

I’ve seen a variation of this message on social media over the years. Personal finance is one of those topics that we have to figure out on our own as we go through life, and it can be highly frustrating. This is why I wanted to look at what you likely weren’t taught about money as a high school or college student that you should know.

Here’s what college and high school never taught you about money that you need to know.

10 Harsh Money Lessons That You Never Learned in School

By Martin Dasko / STUDENOMICS

“They should teach personal finance in college.”

“I wish I learned more about money in school instead of studying all that useless stuff.”

I’ve seen a variation of this message on social media over the years. Personal finance is one of those topics that we have to figure out on our own as we go through life, and it can be highly frustrating. This is why I wanted to look at what you likely weren’t taught about money as a high school or college student that you should know.

Here’s what college and high school never taught you about money that you need to know.

Money lessons you didn't learn in school

I can’t tell you how many times a reader or friend complained about how they learned nothing about finances in school. You have to figure out credit scores, mortgages, credit cards, investing, retirement planning, budgeting, being able to afford a Friday night with soaring inflation, and career advancement all on your own.

You don’t learn much about personal finance and money management as you go through the education system. You go from trying to get by as a broke college student to being thrust into the real world, where you suddenly have to worry about paying your bills, all while trying to figure out how to balance between saving for your retirement one day and trying to afford all of these weddings that you have to attend.

Let’s go over what every young person should learn about money right now that you probably won’t learn in college or high school. These are ten money lessons that should be taught to all young people.

Lesson #1: The World Is Designed To Separate You From Your Money.

“I firmly believe that everything in this world is designed to separate you from your money.”

An economics professor dropped this gem on us one morning (so I technically learned this in college). Since hearing this, I can’t stop thinking about it because it’s accurate. He described how everything is happening around us to take our money.

There will always be something to spend money on. You can’t scroll social media for more than two seconds without being sold something. There are ads for everything, and the ads are targeted to promote something you likely discussed an hour earlier or thought of in your mind.

What can you do about this?

Save first. Always pay yourself first. Have money automatically come off your paycheck. Don’t attempt to save when you don’t spend after getting paid. Save first.

Hide/lock your money. I call this the Houdini System. I hide my money in an investment account and ensure I cannot access it.

Stop saving your credit card details with every online retailer. It’s ridiculously easy to spend money these days. Don’t save your credit card information with Amazon. You don’t always need everything delivered to you in minutes.

Set priorities. I’ve learned that you can have anything you want, but you can’t have everything you want.

Whatever you do, never rely on willpower. Hide your money and set it aside. The world is designed to take your money from you. On top of finding ways to keep more of your money, you also have to ensure that you don’t get scammed. The video below covers this…

Lesson #2: You Must Figure Out Where Your Money’s Going.

“I have no idea where my paychecks go.”

I’ve heard this from many friends over the years, and it’s always startling. I understand why this happens, though. Life comes at you fast, and everything that you want to do is expensive. Suddenly, you’re a week removed from payday and have no idea where your money went.

You don’t have to track every penny, but knowing where your money’s going is essential. You don’t want to be confused as to why you’re broke. You have to figure out where your money’s going.

How do you figure out where your money’s going?

To continue reading, please go to the original article here:

The Number One Reason Most People Are Broke Or Have No Emergency Fund

The Number One Reason Most People Are Broke Or Have No Emergency Fund

by Todd Kunsman InvestedWallet

I’m sure if you are reading this, you’ve come across other articles that talk about the importance of building your savings or having some sort of an emergency fund. Whether that be for an unexpected medical bill, something breaks down in your car, etc. I’m not personally a fan of the “emergency fund” term, as you should be building up your savings to use for investments, retirement, etc.

But whatever it may be, most Americans are in pretty bad shape if some expensive issue comes up.

The Number One Reason Most People Are Broke Or Have No Emergency Fund

by Todd Kunsman InvestedWallet

I’m sure if you are reading this, you’ve come across other articles that talk about the importance of building your savings or having some sort of an emergency fund. Whether that be for an unexpected medical bill, something breaks down in your car, etc. I’m not personally a fan of the “emergency fund” term, as you should be building up your savings to use for investments, retirement, etc.

But whatever it may be, most Americans are in pretty bad shape if some expensive issue comes up.

Because of a lack of prep, many times people are forced to rack up credit card debt to pay for the expense or get tons of late notices with extra fees thus essentially getting stuck with more and more bills, costing you a chance to stack that money away.

Yet, what’s even scarier is the lack of savings the groups of 35 and under have saved. Whether that is for an emergency fund or retirement.

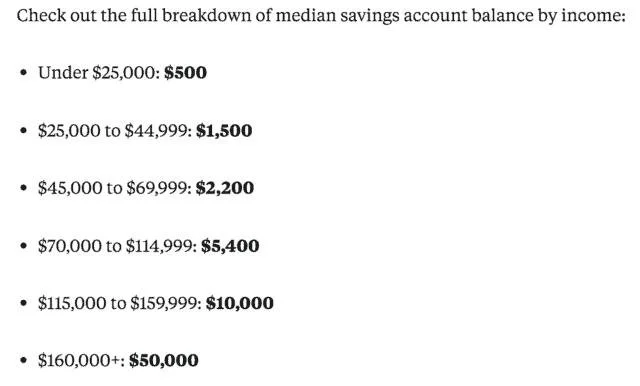

In a Business Insider article, they broke down savings rates by different categories by using data from the Federal Reserve’s Survey of Consumer Finances.

First, average savings account balance by age, which was not looking too pretty:

Another section they broke down, was the median savings account balance by income:

Understandably, higher earners are able to save more money and the older people get, the more money they will have because of time being on their side.

It also makes sense for the 35 and under group to have low savings for a few reasons: Paying off student loans, just developing their careers, maybe still going to school, etc.

Of course all the above can attribute to other things, these are just some examples.

But, we also know people with low incomes have amassed huge retirement or savings fortunes, so a lack of income is not necessarily the main cause.

So, why do people seem to have no money or struggle to save?

To continue reading, please go to the original article here:

https://investedwallet.com/number-one-reason-most-people-are-broke/

We’ve Waited Nearly 15 Years For This

We’ve Waited Nearly 15 Years For This

April 19, 2023 Simon Black, Founder Sovereign Man

Thousands of years ago on the 27th of July, 54 BC, the famed Roman senator Cicero wrote a letter to his friend Atticus complaining about all the corruption and bribery that was destroying Rome’s political system. There was an important election taking place that year for Roman consul, which had once been considered among the highest political offices in the republic.

But by 54 BC, the consuls were just political stooges… because the real power was held behind the scenes by none other than Julius Caesar, and his rival Pompey the Great.

We’ve Waited Nearly 15 Years For This

April 19, 2023 Simon Black, Founder Sovereign Man

Thousands of years ago on the 27th of July, 54 BC, the famed Roman senator Cicero wrote a letter to his friend Atticus complaining about all the corruption and bribery that was destroying Rome’s political system. There was an important election taking place that year for Roman consul, which had once been considered among the highest political offices in the republic.

But by 54 BC, the consuls were just political stooges… because the real power was held behind the scenes by none other than Julius Caesar, and his rival Pompey the Great.

Caesar and Pompey both spent enormous amounts of money to make sure their people won the elections; it was very similar to how today’s biggest political donors spend millions of dollars to push their hand-picked candidates into office. The politicians are just puppets; the real power is the money behind them.

Caesar and Pompey were certainly wealthy guys at the time. But the election of 54 BC set off a financial arms race between the two, with each one trying to out-spend the other to manipulate the election.

One of Pompey’s candidates-- a man named Scaurus the Younger-- was actually charged with extortion.

Two other candidates allegedly attempted to bribe a large voting bloc known as the centuria praerogativa for a whopping 10 million sesterces; this would be the equivalent of hundreds of millions of dollars today.

Another candidate alleged that the two outgoing consuls had been bribed with four million sesterces. The bribery allegations went on and on.

The election of 54 BC was so corrupt and cost so much money that Caesar, Pompey, and their candidates had to borrow heavily from investors to finance all the bribery.

And this is what led Cicero to remark to his friend Atticus, “Bribery is raging. And I will show you a sign of it: the interest rate has gone up from 4% on the 15th of July to 8% [on the 27th of July].”

In other words, the politicians and their financial backers spent so much money to rig the election that they had borrowed nearly all of the capital in Rome’s financial system… causing a spike in interest rates.

This makes sense when you think about it: the election of 54BC created a sudden, overwhelming demand for loans; Caesar and Pompey borrowed heavily in a very short period of time. Just like the basic law of supply and demand, that surge in demand for capital caused an increase in the “price of money”, i.e. interest rates.

Now, imagine being an ancient Roman businessman in the summer of 54 BC looking for a small business loan, perhaps to finance expansion or fund the season’s agricultural harvest.

But then you find that there’s no more money… or only very expensive, high-interest loans available... because the politicians had already borrowed all the money in the financial system.

Economists call this the ‘Crowding Out’ effect, i.e. what happens when someone borrows so much money that there’s very little capital left over for everyone else.

In modern times that ‘someone’ is typically the government, i.e. government borrowing is so extreme that they monopolize all the liquidity in the financial system, thus causing interest rates to rise and ‘crowding out’ the private sector from accessing capital.

And we’re starting to see the Crowding Out effect in our daily lives.

For most of the past 15 years, the Federal Reserve kept interest rates in the US at nearly zero. Capital was infinite. And if the government wanted to borrow more (which they did every year), the Fed simply created more money.

Between 2008 and 2022, in fact, the size of the Federal Reserve’s balance sheet soared from $850 billion to $9 trillion… a more than 10x monetary expansion.

One obvious effect of such reckless monetary policy has been historically high inflation… which ultimately prompted the Fed to reverse course and hike interest rates.

What few people talk about, though, is that the Fed has also begun the lengthy process to reduce the size of its gargantuan balance sheet… essentially draining liquidity from the financial system.

Right now the Fed’s balance sheet stands at around $8.6 trillion, down from a peak of $9 trillion a year ago. So there’s still a looooooong way to go before they get back to the 2008 level of $850 billion, or even the pre-pandemic $4 trillion.

And this takes me back to the Crowding Out effect.

We all know the federal government is addicted to unsustainable spending. Just look at the debt ceiling fiasco-- the Treasury is weeks away from default, and yet the guy who shakes hands with thin air refuses to make any spending cuts.

The Congressional Budget Office currently projects an average $2 trillion annual budget deficit, EVERY YEAR, for the next 10 years. And this estimate is probably quite optimistic; it doesn’t take into consideration any exigent funding requirements like war, natural disasters, or pandemics.

Nor does it take into consideration the multi-trillion dollar bailout required to save Social Security in only a few years’ time.

But even if we go with the government’s own projection of $2 trillion per year, that’s STILL a lot of money to borrow.

For most of the past 15 years, the government never had to worry about borrowing; the Federal Reserve was always standing by to create more money and lend it to the Treasury Department at record low rates.

But now the Fed has reversed course. They’re not loaning any more money to the federal government… meaning Uncle Sam has lost its #1 lender.

One of the government’s other top lenders-- Social Security-- is also out of the picture. Social Security has loaned trillions of dollars to the federal government over the years. But now the government is going to have to pay back those loans in order to keep the program funded, PLUS provide an additional bailout on top of that.

Another major lender-- China-- is also off the table. In fact China has SUBSTANTIALLY cut its holdings of US government debt, from a peak of $1.3 trillion, down to $848 billion today… a reduction of more than 34%.

You’re probably starting to see this ‘Crowding Out’ effect; with nearly all of its top lenders gone, yet absolutely no plans to restrain spending, the federal government is already starting to monopolize debt markets.

The amount of available capital in the financial system is falling due to the Fed’s new monetary policy. And the government is sucking up every available penny for themselves.

That leaves very little capital (compared to the last several years) available for businesses… which is actually fantastic news for investors.

Over the past decade when the money supply was expanding and capital was abundant, businesses could easily raise money from investors or borrow from banks.

And the investment terms were usually very one-sided in favor of the business; companies with no hope of ever turning a profit commanded valuations going into the tens of billions of dollars. And some businesses even sold bonds with negative yields.

But today’s conditions are totally different: businesses have to compete with the government for scarce capital. And as a result, many deals are now outrageously good for investors.

Just because the economy has slowed doesn’t mean there aren’t great investments out there. Quite the contrary. There are incredibly productive and innovative businesses all over the world that can achieve enormous success, regardless of economic conditions.

In fact the most successful company in the world today-- Apple-- is a great example. Even during peak stagflation of the 1970s, Apple earned sensational profits after releasing its highly innovative Apple II.

There will most certainly be similar examples from today’s businesses. And yet, because of this Crowding Out effect, they’re all having to roll out the red carpet to investors in order to raise money.

Well it’s about time. Investors have spent the last several years overpaying for stocks, bonds, real estate, NFTs, and just about every asset under the sun.

But right now, finally, investors can get fantastic deals on great businesses. We just don’t know how long these generous conditions are going to last.

Personally I think the Federal Reserve is going to chicken out-- and we’ve talked about this before.

Their rapid interest rate hikes have already caused so much financial destruction, including multiple bank failures. Next up we’ll probably see defaults in commercial real estate, corporate bonds, municipal bonds, and even a sovereign government or two overseas.

Most importantly, though, the Fed’s higher interest rates will eventually bankrupt the US government. The national debt is already $31.4 trillion, and it increases by $2 to $4 trillion per year. They simply cannot afford to pay 5% interest.

The Fed knows this… which is why I expect them to chicken out and start slashing rates again. The survival of the government depends on it.

And when they do, financial conditions will reverse again. Companies will easily be able to raise capital, and the deals that we see now will no longer exist.

To your freedom, Simon Black, Founder Sovereign Man

https://www.sovereignman.com/trends/weve-waited-nearly-15-years-for-this-146858/

The 10 Most Important Things to Simplify in Your Life

The 10 Most Important Things to Simplify in Your Life

Written By Joshua Becker ·

Plant in clear vase on a simple white table - how to simplify your life

“Purity and simplicity are the two wings with which man soars above the earth and all temporary nature.” —Thomas à Kempis

Simplifying your life will bring balance, freedom, and joy. When we begin to live simply and experience these benefits, we begin to ask the next question, “Where else in my life can I remove distraction and simplify life to focus on the essentials?”

Once we’re able to answer that, we will understand what is important in our own lives.

The 10 Most Important Things to Simplify in Your Life

Written By Joshua Becker ·

Plant in clear vase on a simple white table - how to simplify your life

“Purity and simplicity are the two wings with which man soars above the earth and all temporary nature.” —Thomas à Kempis

Simplifying your life will bring balance, freedom, and joy. When we begin to live simply and experience these benefits, we begin to ask the next question, “Where else in my life can I remove distraction and simplify life to focus on the essentials?”

Once we’re able to answer that, we will understand what is important in our own lives.

How to Simplify Your Life

Based on our personal journey, our conversations, and our observations, here is a list of the 10 most important things to simplify in your life today to begin living a more balanced, joyful lifestyle:

1. Your Possessions – Too many material possessions complicate our lives to a greater degree than we ever give them credit. They drain our bank account, our energy, and our attention. They keep us from the ones we love and from living a life based on our values.

If you will invest the time to declutter the non-essential possessions from your life, you will never regret it. For more inspiration, consider Simplify: 7 Guiding Principles to Help Anyone Declutter Their Home and Life.

2. Your Time Commitments – Most of us have filled our days full from beginning to end with time commitments: work, home, kid’s activities, community events, religious endeavors, hobbies… the list goes on. When possible, release yourself from the time commitments that are not in line with your greatest values.

3. Your Goals – Reduce the number of goals you are striving for in your life to one or two. By reducing the number of goals that you are striving to accomplish, you will improve your focus and your success rate.

Make a list of the things that you want to accomplish in your life and choose the three most important. Focus there.

4. Your Negative Thoughts – Most negative emotions are completely useless. Resentment, bitterness, hate, and jealousy have never improved the quality of life for a single human being. Take responsibility for your mind. Forgive past hurts and replace negative thoughts with positive ones.

5. Your Debt –

To continue reading, please go to the original article here:

https://www.becomingminimalist.com/the-10-most-important-things-to-simplify-in-your-life/