A Better Path to Contentment

A Better Path to Contentment

By Joshua Becker · becomingminimalist

People look for contentment in any number of places.

Some look for contentment in a high-paying job, yet show their discontent the first time they are passed over for a raise. Some look for it in a large home, yet show their discontent by requiring countless improvements. Many have sought contentment in a department store, believing that one more item will finally match their desire, but they are always disappointed, despite the promises made in ads.

In our consumeristic culture, where discontent is promoted and material gratification is encouraged, learning to be content can be difficult.

A Better Path to Contentment

By Joshua Becker · becomingminimalist

People look for contentment in any number of places.

Some look for contentment in a high-paying job, yet show their discontent the first time they are passed over for a raise. Some look for it in a large home, yet show their discontent by requiring countless improvements. Many have sought contentment in a department store, believing that one more item will finally match their desire, but they are always disappointed, despite the promises made in ads.

In our consumeristic culture, where discontent is promoted and material gratification is encouraged, learning to be content can be difficult.

It is a personal journey we all must travel—and nobody’s journey looks exactly the same as another’s. There is no one-size-fits-all, seven-step program to fully attain contentment in your life. I’m not here to offer one.

I do, however, want to raise a question that I think can be helpful to all of us in our pursuit.

What if we have been looking for contentment in all the wrong places?

What if contentment is actually found in the exact opposite of the place where we have been told to look?

That is, what if contentment is not found in accumulating more for ourselves but in giving more to others?

That would change everything!

Benefits of Generosity

We can quickly picture how contentment would lead to generosity—the less we need, the more we can give away. That’s the way most of us think about it.

But could it be that the inverse is also true? That the more we give, the less we need?

And that generosity is the quickest pathway to contentment?

Consider for just a moment why this might be the case:

Generous people appreciate what they have.

People who give away some possessions hold their remaining possessions in higher esteem. People who volunteer some of their time make better use of their time remaining. And people who donate money are less wasteful with the money left over.

They understand the full potential of their resources—and tend to value them more highly because of it.

Generous people live happier, more fulfilled lives.

Studies have shown that generous people are happier, healthier, and more satisfied with life. And once they find this satisfaction through generosity, they are less inclined to search for it elsewhere.

Generous people find meaning outside their possessions.

To continue reading, please go to the original article here:

https://www.becomingminimalist.com/a-better-path-to-contentment/

Be Like the Smiths

Be Like the Smiths

Adam M. Grossman | Apr 16, 2023 HumbleDollar

NETFLIX BEGAN AN experiment in 2003 that seemed crazy to management experts. It instituted a policy of unlimited vacation time for its employees. In the years since, a number of other companies have followed Netflix’s lead, offering employees unlimited paid time off.

The results have run counter to intuition: Employees who are offered unlimited vacation end up taking less time off than those working for companies with traditional vacation policies. Why? A common explanation is that people struggle when they lack clear guidelines.

Be Like the Smiths

Adam M. Grossman | Apr 16, 2023 HumbleDollar

NETFLIX BEGAN AN experiment in 2003 that seemed crazy to management experts. It instituted a policy of unlimited vacation time for its employees. In the years since, a number of other companies have followed Netflix’s lead, offering employees unlimited paid time off.

The results have run counter to intuition: Employees who are offered unlimited vacation end up taking less time off than those working for companies with traditional vacation policies. Why? A common explanation is that people struggle when they lack clear guidelines.

In this case, it appears that—in the absence of a defined policy—employees are doing what seems safest. By taking less time off than they could, they’re trying to protect their professional reputations. They want to be seen as hard workers. By contrast, when employees are told that they have, say, 15 days off, they’ll tend to take all 15 days off. In short, people do better with structure.

This idea applies in nearly every domain. I recall taking a family vacation to a destination where both food and lodging were included for one flat rate. The result: Without the usual mealtime structure, I found myself with a stomachache and a desire never to go back.

This same dynamic applies to our personal finances. Limits can be helpful. Counterintuitive as it might seem, if you have a surplus in your budget—or assets that exceed your foreseeable needs—budgeting can be tricky. “Can I afford this?” If the answer to that question is “yes” in virtually every case—or every reasonable case—it’s harder to know how to set boundaries.

For better or worse, financial decision-making is more straightforward for those with limited means. A new iPhone, for example, is either affordable or it’s not. But if you can easily afford a new phone or a new car or maybe even a new home, it’s harder to know how to establish limits. This might sound like “a good problem to have.” But in reality, it applies to many retirees, who have ready access to their life’s savings.

How do folks handle this situation? Among those who have achieved financial independence, people tend to fall into one of three categories.

The first look something like the Vanderbilt family. In the 1890s, the Vanderbilts were the wealthiest family in America. With that fortune, they built the Breakers in Newport, Rhode Island, the largest of the Newport mansions, with 30 bedrooms just for staff. In North Carolina, they constructed the Biltmore Estate, which—at nearly 180,000 square feet—is still the largest home in the U.S. And, of course, they endowed Vanderbilt University. The unhappy result, however, was that the family’s fortune dwindled in a surprisingly short period of time.

The second group couldn’t be more different from the Vanderbilts. They look something like Ronald Read. A resident of Brattleboro, Vermont, Read spent most of his career as a gas station attendant. But when he died in 2014, he left an estate of nearly $8 million, owing mostly to his frugality.

When he drove into town, for example, he would park a few blocks away from his favorite coffee shop to avoid parking meters. When the buttons fell off his jacket, he used a safety pin to hold it closed. His appearance, in fact, was such that a fellow restaurant patron once paid the tab for his meal, believing he was destitute. In short, Read took frugality to an extreme—far beyond what was necessary.

What about the third group? We might call them the Smiths—because they don’t look too different from their neighbors.

To continue reading, please go to the original article here:

What Do Fitness and Finance Have In Common?

What Do Fitness and Finance Have In Common?

APRIL 11, 2023 Financial Pilgrimage

What do physical fitness and personal finance have in common? On the surface, there are a lot of differences between your fitness program and financial wellness. One involves income, spending, saving, and investing. The other involves physical activity, nutrition, and overall health. The reality is that financial fitness (and just fitness) are some of the most critical areas of our lives. It’s no coincidence that there are striking similarities between fitness and finance once you start digging in.

What Do Fitness and Finance Have In Common?

APRIL 11, 2023 Financial Pilgrimage

What do physical fitness and personal finance have in common? On the surface, there are a lot of differences between your fitness program and financial wellness. One involves income, spending, saving, and investing. The other involves physical activity, nutrition, and overall health. The reality is that financial fitness (and just fitness) are some of the most critical areas of our lives. It’s no coincidence that there are striking similarities between fitness and finance once you start digging in.

Financial Fitness is Behavioral

Fitness programs have always been a big part of my life. So when referring to fitness, we’ll discuss both sides of the equation, including physical activity and nutrition. Being raised by a dietitian and having a love of sports had me interested in both early on. Looking back, I feel fortunate to have built habits in both areas at a relatively young age.

Growing up in a house with two younger brothers and a junk food-loving dad, the competition for unhealthy food was fierce. My mom would grocery shop every ten days, and the one bag of chips or a package of cookies would be gone within a day, sometimes minutes. That would leave us with rice cakes, fruits and veggies, and other healthy options for the rest of the week and a half. It was rough.

We had home-cooked meals that consisted of protein, carbs, and vegetables most nights. But, as I got older, I realized that having home-cooked meals was a rarity compared to other households.

We’d still get fast food on occasion. My dad was a fast-food manager, after all. With three kids in the house, sometimes the easy thing was to bring home a big bag of burgers and fries so we could eat and then make our way to evening activities. This taught me that one of the most critical nutrition lessons is “everything in moderation.” Eating fast food, sweets, or potato chips is fine occasionally as long as most of what you put into your body is more healthy.

Whenever a new diet fad becomes popular, I’ll ask my mom about it to get her thoughts. Usually, she rolls her eyes. Over the years, there have been so many diet fads—Atkins, Paleo, Intermittent Fasting, Mediterranean, South Beach, and on and on. Almost everyone will swear by one of these diets and back it with “science.” I understand that some diets result from personal beliefs or food allergies. However, most people latch onto these fad diets, stick with them for a while, and then end up right back where they started. We’ll hit on this topic more below.

Personal Finance is Personal – So Is Fitness

When attending FinCon, a conference for personal finance nerds like me, the theme was “personal finance is personal.” This statement means that everyone’s situation is different. It’s one of the reasons I believe there are so many personal finance bloggers, as we all connect to other people differently. I’ve learned through personal finance that if you want to change your behavior, you must change your habits.

Financial and fitness programs are behavioral and they’re personal.

To continue reading, please go to the original article here:

https://financialpilgrimage.com/fitness-and-personal-finance/

What’s Your Answer?

What’s Your Answer?

Jonathan Clements | Apr 15, 2023 HumbleDollar

COMMENTS FROM READERS are one of HumbleDollar’s greatest strengths. Just finished perusing an article? If you don’t scan the comments posted below, you’re often missing out on some savvy financial insights and eye-opening personal stories.

With an eye to tapping into this strength, I launched the Voices section two years ago. My hope: The questions—now 133 in total—would offer a way to organize readers’ collective wisdom and become a go-to resource for those seeking help on a particular financial topic.

What’s Your Answer?

Jonathan Clements | Apr 15, 2023 HumbleDollar

COMMENTS FROM READERS are one of HumbleDollar’s greatest strengths. Just finished perusing an article? If you don’t scan the comments posted below, you’re often missing out on some savvy financial insights and eye-opening personal stories.

With an eye to tapping into this strength, I launched the Voices section two years ago. My hope: The questions—now 133 in total—would offer a way to organize readers’ collective wisdom and become a go-to resource for those seeking help on a particular financial topic.

To be honest, the Voices questions haven’t garnered as much reader participation as I’d hoped. Still, I find the answers fascinating and, fingers crossed, perhaps the section will eventually catch fire with readers. Meanwhile, here—in order—are the nine questions that have so far generated the most responses:

1. What’s the best financial book you’ve ever read? Among the 45 comments, there’s a wide array of books and authors listed. But perhaps the most mentioned are The Millionaire Next Door by Thomas Stanley and William Danko, John Bogle’s books, Burton Malkiel’s A Random Walk Down Wall Street and William Bernstein’s books.

Incidentally, Bill has a new edition of The Four Pillars of Investing coming out in July. I had the privilege of writing the foreword. Bill also contributed an essay to My Money Journey, the HumbleDollar book that’ll be published later this month.

2. What percentage of a stock portfolio should be invested abroad? This has long been a raging debate among investors, and the responses reflect that, with folks suggesting foreign-stock allocations ranging from 0% to 50%. After strong U.S. stock returns over the past decade, maybe it isn’t surprising that many folks are content to have no money invested abroad. But if foreign markets have the edge in the decade ahead, will they feel differently? I, for one, would be happier. As I’ve mentioned before, my single biggest fund holding is Vanguard Total World Stock Index Fund (symbol: VTWAX), which has 41% allocated to foreign markets.

3. What’s your favorite financial quote? This question generated a slew of entertaining and thought-provoking responses. Among those offered, my favorite—given today’s inflation—originated with comedian Henny Youngman: “Americans are getting stronger. Twenty years ago, it took two people to carry $10 worth of groceries. Today, a five-year-old can do it.”

4. What costs are you most loath to pay?

To continue reading, please go to the original article here:

How to Never Run Out of Money in Retirement

How to Never Run Out of Money in Retirement

APRIL 15, 2023 •White Coat Investor

Are you afraid of running out of money in retirement? Use these strategies to ensure this doesn't happen to you.

One of the greatest fears of many investors and retirees is that they will run out of money in retirement. However, there are many strategies available to ensure this doesn't happen to you. By employing one or more of these, you can dramatically decrease those odds.

How to Never Run Out of Money in Retirement

APRIL 15, 2023 •White Coat Investor

Are you afraid of running out of money in retirement? Use these strategies to ensure this doesn't happen to you.

One of the greatest fears of many investors and retirees is that they will run out of money in retirement. However, there are many strategies available to ensure this doesn't happen to you. By employing one or more of these, you can dramatically decrease those odds.

8 Ways to Ensure You Don't Run Out of Money in Retirement

The greatest financial task of your life is to save up enough money for retirement. However, some people don't quite make it. Or barely make it. Or have bad things happen to them. In spite of that, there are at least eight strategies that will still allow you to avoid running out of money. Choose one or more to apply in your life.

#1 Save More

This strategy is employed by many. The 4% “rule” suggests you save up about 25X your annual spending before retiring. However, there is no law that says you can't save up 30X, 33X, 40X, or even 50X. Obviously the more you have in relation to how much you spend, the less likely you are to run out of money.

#2 Spend Less (at Least Sometimes)

Here's another great strategy that works very well. Instead of saving more, you can simply spend less. Maybe you were planning to spend $100,000 per year in retirement, but if you can manage to spend just $80,000, you are far less likely to run out of money.

You can do this by downsizing or by moving to a lower cost of living area, or you can adjust how often you go out to eat, where you go on vacation, or what you drive in retirement. Lots of options.

But you don't actually have to spend less ALL the time. You really only have to spend less when your portfolio is doing poorly. This “variable withdrawal strategy” dramatically increases how much you can spend overall, even if it means sometimes you have to spend a little less. Having spending flexibility in retirement is very valuable.

#3 Only Spend Income

If you never actually touch your principal, you will never run out of money. That doesn't mean your nest egg, your income, and your spending will be stable or that it will even keep up with inflation, but it does mean you won't run out completely. Yet, this strategy can lead to potential errors.

Perhaps the greatest is that you'll end up spending much less than you could have spent—to some people, that just means they worked too long and saved too much. It can also lead someone to inappropriately invest in a high-yielding portfolio. Just because your income is higher doesn't mean your total return is higher or even positive. Often it leads people to work and invest differently.

They might be more interested in entrepreneurship and both direct and indirect real estate investing, for instance. Nothing wrong with that, but it does require a different set of skills and adds some risk, hassle, and (often) leverage.

#4 Spend Your Legacy

To continue reading, please go to the original article here:

https://passiveincomemd.com/how-to-never-run-out-of-money-in-retirement/

Who Do You Trust?

Who Do You Trust?

Casey Snyder | Apr 14, 2023 HumbleDollar

MORE THAN 92,000 people over age 60 reported losses to fraud totaling $1.7 billion in 2021, according to the FBI’s Internet Crime Complaint Center. That represented a 74% increase in losses from the year before.

With the population of older Americans growing, the need to protect this vulnerable population is more critical than ever. Enter the concept of a trusted contact.

Who Do You Trust?

Casey Snyder | Apr 14, 2023 HumbleDollar

MORE THAN 92,000 people over age 60 reported losses to fraud totaling $1.7 billion in 2021, according to the FBI’s Internet Crime Complaint Center. That represented a 74% increase in losses from the year before.

With the population of older Americans growing, the need to protect this vulnerable population is more critical than ever. Enter the concept of a trusted contact.

The trusted contact has its origin in a Financial Industry Regulatory Authority (FINRA) rule issued in March 2020. It urged registered investment advisors to ask clients to name someone the advisor can contact in case of suspicious activity. If you’ve opened a new investment account lately, you’ve probably been asked for a trusted contact.

FINRA defines the role this way: “A trusted contact is an individual authorized by an investor to be contacted by their financial firm in limited circumstances, such as concerns about activity in the investor’s account or if the firm has been unable to reach the investor after numerous attempts.”

Who might be named? It’s most often a family member, but it can also be an attorney, accountant or another reliable third party. Whoever it is, the intent is the same—to provide “another layer of security on the account and puts the financial firm in a better position to help keep the account safe,” in the words of FINRA CEO Robert Cook.

Financial industry veteran Ron Long said the trusted contact concept arose from numerous experiences in which advisors had clients who were requesting funds from their accounts to pay for obvious financial scams.

“Scammers often rely on victims succumbing to pressure to act fast and to avoid discussing the money disbursement with anyone,” said Long, a principal at Long Life Consulting of Seattle, who was previously the head of Aging Client Services at Wells Fargo.

“When an advisor is able to involve a trusted family member, often a son or daughter, they are able to speak with that loved one and successfully break the trance which the bad guy has over their parent,” Long said. “In other instances, the trusted contact acts as an ‘in case of emergency’ resource where an advisor observes signs of diminished capacity or has difficulty contacting an elder client.”

While the concept of a trusted contact is a step in the right direction, it’s not a substitute for a more comprehensive approach to safeguarding elders and their money. For one thing, the circumstances under which a financial firm is authorized to contact the trusted contact are limited, and don’t cover all the possible scenarios in which elder fraud might occur.

As demographics shift, and the demands on clients and their advisors expand, we need to evolve our approach to prevent elder fraud. This is especially important given the increasing rates of cognitive impairment among older Americans.

Here are five steps the public and financial professionals can take to defend those most vulnerable.

To continue reading, please go to the original article here:

Lessons From A Legend

Lessons From A Legend

13 Apr By The Financial Bodyguard

The investment management industry loves its legends and there is none bigger than the nonagenarian ‘Oracle of Omaha’ Warren Buffett, CEO of the US-listed firm Berkshire Hathaway. Over the years in that role Buffett has built a portfolio of directly held companies alongside a portfolio of listed stocks. Today, he is worth over US$100 billion and is the world’s fifth wealthiest person. In anyone’s eyes, he is a highly successful investor and is often held up as a beacon in support of an active, judgmental approach to investing.

Lessons From A Legend

13 Apr By The Financial Bodyguard

The investment management industry loves its legends and there is none bigger than the nonagenarian ‘Oracle of Omaha’ Warren Buffett, CEO of the US-listed firm Berkshire Hathaway. Over the years in that role Buffett has built a portfolio of directly held companies alongside a portfolio of listed stocks. Today, he is worth over US$100 billion and is the world’s fifth wealthiest person. In anyone’s eyes, he is a highly successful investor and is often held up as a beacon in support of an active, judgmental approach to investing.

Paradoxically, Warren Buffett’s legendary status as an active investor provides some useful lessons in support of adopting a systematic, low-cost approach to investing.

Lesson 1: Believe In The Power Of Capitalism And Compounding Over Time

Buffet understands capitalism and the powerful wealth generation that it can bring. He started investing in 1941 when he was 11 years old, and now at 92 years old, has over 80 years of compounding returns from the predominantly US companies he has owned. By the age of 39 he was worth US$25 million. His life story is fascinating[1].

‘The genius of the American economy, our emphasis on a meritocracy and a market system and a rule of law has enabled generation after generation to live better than their parents did.’

Lesson 2: Patience And Emotional Fortitude Are Key

Buffett expects to hold the companies for the long-term, much like an index fund.

‘Our favorite holding period is forever.’

He strives to avoid making decisions driven by emotions in response to short-term market pressures, such as the poor relative performance of value stocks from 2018-20 or equity market falls.

‘The most important quality for an investor is temperament, not intellect.’

Lesson 3: Active Management Is Not Easy

Despite his incredible business acumen, and consequent track record, it is not easy to continue to beat the market over time. He has always been a value oriented investor and was notorious in the run up to the tech crash of 2000-3, stating that he did not get it. He was to some extent proved right.

As Berkshire has grown, finding deals that will make a material difference to performance has become harder. His early years were spent trawling for individual investment opportunities. In those post-war years, information was scarce, professional investors represented a far lower part of the investor base, and markets were probably less efficient. If he was starting out again, would he be as successful? Who knows? And there’s the rub.

Take a look at the chart below, which illustrates 20-year rolling windows of Berkshire’s performance relative to a US equity index fund. It is evident that the huge success of the early days, has given way to far more trying times. Over the past 20 years, you could have achieved virtually the same return by investing in an S&P 500 index fund.

Figure 1: Buffet’s alpha – it is not so easy to win anymore

https://thefinancialbodyguard.com/wp-content/uploads/2023/04/Picture1-768x392.png

Source: Berkshire Hathaway Inc Class A, Vanguard 500 Index Investor Fund (VFINX) USD. Morningstar Direct ©

To continue reading, please go to the original article here:

How Much Money Does a Baby Need to Invest to Become a Millionaire?

How Much Money Does a Baby Need to Invest to Become a Millionaire?

APRIL 13, 2023 Financial Pilgrimage

Compound interest may be the most powerful personal finance-related topic out there. By combining time and money, a little bit today can be worth a whole lot more tomorrow. Most of us have heard about compound interest, but for me, when I sit down and run through the numbers, the power of compound interest blows my mind. In this post, we are going to look at a few examples that stress the importance of starting early, even really early. For example, what if these compound interest examples were taken to the extreme and we started investing for retirement at birth? Let’s take a look.

How Much Money Does a Baby Need to Invest to Become a Millionaire?

APRIL 13, 2023 Financial Pilgrimage

Compound interest may be the most powerful personal finance-related topic out there. By combining time and money, a little bit today can be worth a whole lot more tomorrow. Most of us have heard about compound interest, but for me, when I sit down and run through the numbers, the power of compound interest blows my mind. In this post, we are going to look at a few examples that stress the importance of starting early, even really early. For example, what if these compound interest examples were taken to the extreme and we started investing for retirement at birth? Let’s take a look.

Compound Interest Examples from Bill, Susan, and Chris

Before we get into the power of investing as a baby, let’s look at a few more realistic compound interest examples. The three individuals below are all in different stages of life.

Susan is a college professor who invests $5,000 per year in a stock-heavy retirement account for 10 years total between the ages of 25 and 35. In total, she invests $50,000 during this period. After age 35, Susan decides to begin investing in other assets and does not put any additional money into her retirement account.

Bill is a dietician who also invests $5,000 per year in an account similar to Susan’s but does so over a 30 year time period. Unlike Susan, Bill got a late start to investing and didn’t begin until age 35. He invested $150,000 total until the age of 65-years-old.

Chris is a lab technician who gets the best of both worlds by investing his $5,000 over the full 40 year period, beginning at age 25 and stopping at 65. In total, Chris invests $200,000.

Who do you think will end up with the most money? It’s pretty obvious that Chris will consider that he has the best of both worlds. But what about Susan and Bill?

Compound Interest Examples

CHART ASSUMES 7% GROWTH RATE. SOUCE: BUSINESS INSIDER VIA JPMORGAN.COM

https://financialpilgrimage.com/wp-content/uploads/2018/01/compound-interest-blog-post-9-768x577.png

The main takeaway from the chart is Susan ($602,070) ends up with more money than Bill ($540,741) even though she only invests for a period of 10 years while he invests for 30 years. They invest the same amount of money annually yet the difference is Susan starts investing at the age of 25 (and then stops after 10 years) and Bill starts at the age of 35 and invests until retirement. So, Susan’s 10 years of investing beats Bill’s 30 years since she started at 25 and Bill started at 35.

This is an oversimplified example. In a real-life situation, investments would likely change from year-to-year, hopefully increasing over time. The interest rate of 7% would fluctuate annually, especially with a portfolio heavily invested in stocks. However, the point here is to observe the power of compound interest over time.

To continue reading, please go to the original article here:

When Being Cautious Can Lead To More Risk

When Being Cautious Can Lead To More Risk

10 FEB Financial Bodyguard.com

Financial planning, as the name rather implies, is mostly about the future. Yes, sometimes it can help to identify things which we should do now to make a positive change in our financial circumstances immediately but mostly it is about doing things, whether now or in the future, to help create a better future for ourselves.

In order to work out what these should be and when we should do them, we generally need to project forwards from our current circumstances. This will provide some insights into how feasible our goals are and also highlight where potential roadblocks might occur.

When Being Cautious Can Lead To More Risk

10 FEB Financial Bodyguard.com

Financial planning, as the name rather implies, is mostly about the future. Yes, sometimes it can help to identify things which we should do now to make a positive change in our financial circumstances immediately but mostly it is about doing things, whether now or in the future, to help create a better future for ourselves.

In order to work out what these should be and when we should do them, we generally need to project forwards from our current circumstances. This will provide some insights into how feasible our goals are and also highlight where potential roadblocks might occur.

For example, it is all well and good to see that our resources are projected to be sufficient to meet all our objectives over the next 40 years but if we are likely to run out of liquid assets in the next five years then we might need to change something to avoid that happening.

There are essentially two elements to such a projection – the knowledge of our existing assets, liabilities, income and expenditure and the extent to which these are expected to change over our desired time horizon; in most cases this will be our lifetime.

For those of us not fortunate enough to be able to see the future with perfect clarity, the latter element will require some degree of assumption about how things are likely to develop over time.

How to derive these assumptions and what they should be are issues which absorb the attention of professionals involved in the field because, particularly over long periods, they can have a huge impact on the projected outcome even where the rates are apparently small.

For example, projecting an expenditure of £10,000 at an annual rate of 4.5% rather than 5% results in a difference of more than £12,000 a year after 40 years.

In reality, we have no idea how accurate our assumptions will be as the future is, as ever, unknowable. How many forecasters predicted the timing or impact of either a global pandemic in 2020 or a war in Ukraine in 2022?

Given the impact of getting such assumptions wrong, of which the worst could be running out of resources unexpectedly, it is not hard to see the temptation to adjust our assumptions with a view to being ‘cautious’. This might entail increasing incrementally the assumed rate at which expenditure increases and/or reducing the assumed return earned on invested assets.

However,

To continue reading, please go to the original article here:

https://thefinancialbodyguard.com/when-being-cautious-can-lead-to-more-risk/

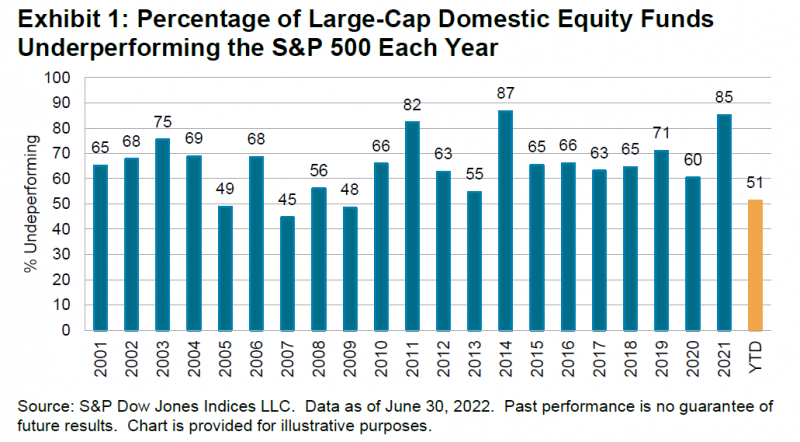

Statistical Sobriety

Statistical Sobriety

January 11, 2023 by Anthony Isola

If your financial plan relies on winning the lottery or day trading – It’s time to find a new plan. Why do people count on the improbable regarding wealth creation?

Putting human emotion aside (Easier said than done), ignoring probability and statistics tops the list.

In 1986 the American Physical Society, the primary organization of our nation’s physicists, encountered a scheduling conflict.

Initially scheduled for San Diego, their convention event was switched to Las Vegas. Four thousand physicists piled into the MGM Grand Marina.

Statistical Sobriety

January 11, 2023 by Anthony Isola

If your financial plan relies on winning the lottery or day trading – It’s time to find a new plan. Why do people count on the improbable regarding wealth creation?

Putting human emotion aside (Easier said than done), ignoring probability and statistics tops the list.

In 1986 the American Physical Society, the primary organization of our nation’s physicists, encountered a scheduling conflict.

Initially scheduled for San Diego, their convention event was switched to Las Vegas. Four thousand physicists piled into the MGM Grand Marina.

That’s when things got interesting. During the physicist’s siege, MGM had its worst week – ever. Many would guess that these brainiacs were expert poker, roulette, or craps players due to their stratospheric I.Q.s.

That wasn’t the case. Mathematics kept their wallets full. They knew the odds and refused to play. By American standards, this is a Black Swan; in 2021, Casino revenue reached an all-time high of $45 Billion!

Likely, this group doesn’t partake in another of America’s favorite pastimes, playing the lottery. We spend $100 Billion yearly in this doomed quest to become rich and famous.

Advertisers know our Kryptonite. It’s not in their playbook to display their product’s effectiveness statistics. Celebrity endorsements provide the bait. During last year’s Super Bowl, Crypto Ads were all the rage.

Matt Damon insulted the manhood of millions by mocking their fear of uncertainty and the potential wealth of digital coins. We know how this turned out for the Crypto Bros.

Stock investors fall for the same fallacies. Ignoring probabilities shouldn’t be a part of anyone’s financial portfolio.

Even the so-called experts fall prey to a lottery mentality. Ignore index funds at your peril.

SPIVA data confirm these findings.

What’s the solution to this madness?

To continue reading, please go to the original article here:

Seven Alternative Facts about your Money

Seven Alternative Facts about your Money

by Anthony Isola

People love to use words and expressions to cloud their real intentions. Often these expressions can cloak lies and make you feel better about doing something that is just plain awful.

George Orwell wrote about how governments can mask some pretty nasty stuff with word tricks.

In our time, political speech and writing are largely the defense of the indefensible. Defenseless villages are bombarded from the air; the inhabitants, driven out into the countryside; the cattle machine gunned; the huts set on fire with incendiary bullets. This is called pacification.

Seven Alternative Facts about your Money

by Anthony Isola

People love to use words and expressions to cloud their real intentions. Often these expressions can cloak lies and make you feel better about doing something that is just plain awful.

George Orwell wrote about how governments can mask some pretty nasty stuff with word tricks.

In our time, political speech and writing are largely the defense of the indefensible. Defenseless villages are bombarded from the air; the inhabitants, driven out into the countryside; the cattle machine gunned; the huts set on fire with incendiary bullets. This is called pacification.

People are imprisoned for years without trial, or shot in the back of the neck or sent to die of scurvy in Arctic lumber camps. This is called the elimination of unreliable elements.

Euphemisms can be very dangerous. They have the ability to confuse and mislead people who are unfamiliar with a situation. They can make something very bad look very good.

Money is a prime breeding ground for all manners of psychoses. Euphemisms often serve as a form of financial camouflage for our worst desires. They work silently to give us the feeling we are doing something productive when in reality the opposite is occurring.

Here are some common examples:

“I did a lot of research on this stock.”- Scientists do research using data. Choosing an investment because you saw some person you don’t know talk about it on T.V. for two minutes does not make you Marconi.

“I don’t have time to learn about my finances.” – No, you choose to do other things with your time. You may choose to spend your time watching T.V. for seven hours a day or mindlessly playing Candy Crush. Don’t confuse doing what you want to do, over doing what you don’t want to, as a lack of time.

“My house is a financial investment.” – Actually, things that pay YOU are considered to be an investment. When you have a mortgage, property taxes, and large upkeep costs, you are paying someone else. There is nothing wrong with home ownership, but don’t confuse it with something that is designed to beat inflation over long periods of time.

“I saved money because this was on sale.”- Buying something that you did not need is not saving money. You simply cut down your unnecessary spending by a small amount. Not exactly the best way to build up your savings account.

To continue reading, please go to the original article here:

https://tonyisola.com/2017/07/seven-alternative-facts-about-your-money/