Where to Exchange Currency (It’s Not the Bank!)

Where to Exchange Currency (It’s Not the Bank!)

January 13, 2023

A few weeks ago, I walked into Chase Bank in Florida and asked to withdraw cash from my checking account in the form of Australian dollars for an upcoming trip. The branch manager smiled and quoted me a currency exchange rate that was seven percent worse than the accepted market rate. As if that weren’t bad enough, he also told me I’d have to wait 2 business days to get my devalued money.

This type of inefficiency isn’t unique to the Chase foreign currency exchange. Almost all major banks are dinosaurs when it comes to financial technology, which is why Lauren and I go elsewhere for things like fee-free investment accounts, higher-interest savings accounts, and now — international currency conversion.

Where to Exchange Currency (It’s Not the Bank!)

January 13, 2023

A few weeks ago, I walked into Chase Bank in Florida and asked to withdraw cash from my checking account in the form of Australian dollars for an upcoming trip. The branch manager smiled and quoted me a currency exchange rate that was seven percent worse than the accepted market rate. As if that weren’t bad enough, he also told me I’d have to wait 2 business days to get my devalued money.

This type of inefficiency isn’t unique to the Chase foreign currency exchange. Almost all major banks are dinosaurs when it comes to financial technology, which is why Lauren and I go elsewhere for things like fee-free investment accounts, higher-interest savings accounts, and now — international currency conversion.

Using these four strategies, you can exchange currency without high fees or long waits in nearly any country on Earth.

1. Use Your Credit Card as an Automatic Currency Converter

Unless you specifically need cash (which we’ll get to shortly), the most convenient and efficient way to convert US dollars into foreign currency without fees is to just use a credit card for all your purchases. This is one of the few things that major banks like Chase actually get right. You just swipe your card abroad, and the purchases show up on your statement in US dollars, magically converted at the right exchange rate.

But before packing your bags, make sure you have a card with no foreign transaction fees. Our Citi DoubleCash card is great for everyday purchases in the US, but we’d never use it overseas, since Citi imposes a 3% surcharge on all international DoubleCash purchases.

Personally, we use our Chase Sapphire Preferred or IHG Rewards Traveler cards abroad; they don’t charge any fees for international transactions. And in our experience so far, they’ve automatically converted our purchases in other currencies to US dollars to within ~1% of the correct foreign exchange rate. We earn cash back and other rewards as normal, too!

There are tons of good cards out there with no foreign transaction fees, so you might already have one in your wallet without knowing it. If not, you can always find an updated list of our favorite credit cards on our Recommendations page.

By the way, when you swipe a US credit card abroad, the merchant may ask if you’d like to pay in US dollars or in the local currency. As a general rule, you should always choose the local currency and let your credit card company do the foreign currency exchange for you. Merchant terminals typically impose unfair exchange rates.

As always, make sure you follow the basic rules of using any credit card responsibly, too.

2. Exchange Currency at a Foreign ATM

To continue reading, please go to the original article here:

https://www.tripofalifestyle.com/gear-and-tips/where-to-exchange-currency/

7 Experts Share Their Best Money Advice for Kids

7 Experts Share Their Best Money Advice for Kids

January 16, 2023 Financial Pilgrimage

There are a million things to worry about when raising children. Often, teaching our kids about money doesn’t rise to the top of the list. If your kids are anything like mine, they care about video games, dolls, sports, and many other things.

There is a push and pull when raising money-smart kids. As parents, we want to provide our kids with the best life. Sometimes that means giving them the toy we always wanted as a kid but could never afford. It feels terrific when your kid is happy.

7 Experts Share Their Best Money Advice for Kids

January 16, 2023 Financial Pilgrimage

There are a million things to worry about when raising children. Often, teaching our kids about money doesn’t rise to the top of the list. If your kids are anything like mine, they care about video games, dolls, sports, and many other things.

There is a push and pull when raising money-smart kids. As parents, we want to provide our kids with the best life. Sometimes that means giving them the toy we always wanted as a kid but could never afford. It feels terrific when your kid is happy.

The hard part is thinking through the downstream impacts of giving them everything they want. Handing everything to them will make it challenging to appreciate hard work. How will they learn to appreciate how fortunate we are to live in the United States of America, one of the wealthiest countries in the world? How do we teach them there is more to life than material things?

I’m not sure I have found the correct answers to these questions. Or at least I am still trying to figure them out. I turned to money experts on Twitter to share their best advice for kids. The responses were excellent, and I took a few notes as a parent. So read on for money advice for kids from seven personal finance experts.

7 Experts Share Their Best Money Advice for Kids

Lesson 1: Make Their Money Work For Them

This article from the Interesting Dollar shared a great idea to use birthday money to demonstrate the value of interest. By gifting $300 a year for birthdays (between parents, grandparents, and aunts/uncles), you could demonstrate the growth provided by interest over a relatively short period. This simple exercise can help teenagers delay gratification and better understand how interest works. Below is an excerpt from the article.

“I did the math and thought that if they received $300 a year from age 10 to 17 and 8% interest, they would receive $2,592 on their 18th birthday. Then, each year they would receive the interest check on the balance in the account.”

Lesson 2: Embrace Minimalism

So much of what makes a person successful with their finances as an adult is being intentional. A high income helps, but many people make a lot of money and still live paycheck to paycheck. I love this article from One Frugal Girl about her conversations with her children. It’s not necessarily about depriving your kids of toys but getting them to be thoughtful about why they want something.

“I want them to learn how to use their imaginations to prevent boredom rather than depending on a room full of toys.“

Lesson 3: Use Money to Buy Your Time

To continue reading, please go to the original article here:

The Secrets of Stealth Wealth

The Secrets of Stealth Wealth

17. October 2022 Financial Imaginer

How many people do you know who have stealth wealth? Chances are, not many. That’s because stealth wealth is something that people living it don’t talk about. It’s a secret that they keep to themselves. But why? Why go to all the trouble of keeping your wealth a secret? In this article, I shall try to answer that question and more.

We will explore the concept of stealth wealth and discuss why it is something that everyone should be interested in. We will also provide tips on how to live a life of stealth wealth and how to recognize if others are doing the same. Lastly, we will explain what it takes for you to start living a stealthy wealthy life and why doing so can be so beneficial.

The Secrets of Stealth Wealth

17. October 2022 Financial Imaginer

How many people do you know who have stealth wealth? Chances are, not many. That’s because stealth wealth is something that people living it don’t talk about. It’s a secret that they keep to themselves. But why? Why go to all the trouble of keeping your wealth a secret? In this article, I shall try to answer that question and more.

We will explore the concept of stealth wealth and discuss why it is something that everyone should be interested in. We will also provide tips on how to live a life of stealth wealth and how to recognize if others are doing the same. Lastly, we will explain what it takes for you to start living a stealthy wealthy life and why doing so can be so beneficial.

Stealth Wealth is essentially all about having more control over your life and your finances and being able to do what you want when you want.

Contrary to popular belief, stealth wealth is not just for millionaires. Anyone can live a stealth wealth lifestyle if they know how. In this article, we will discuss the secrets of stealth wealth and how you can start living a richer life today!

The greatest wealth is to live content with little. – Plato

The Secrets of Stealth Wealth: How to Live a Bigger, Better Life on Your Own TermsCLICK TO TWEET

What is Stealth Wealth?

In short, stealth wealth is living beneath your means.

It’s about keeping your wealth hidden from others, even from family, friends and co-workers. It allows you to live the lifestyle you chose without having the outward appearance of being wealthy.

It’s about being content with what you have and not worrying about what other people think of you.

It’s about living a simple lifestyle and not constantly trying to keep up with the Joneses.

It’s about enjoying life without having to impress others with material possessions.

I’m most certain you’ve ever been curious about the financial status of people you know.

Now imagine if you’re filthy rich but don’t want anyone to know. That’s why some people lead seemingly ordinary lives while driving average cars and seem to be middle-class, while secretly being wealthy.

This is called stealth wealth, and it might just be the wisest decision anyone can make with money and wealth.

Contrary to your average “Nouveau-riche-Lambo-now Crypto Gazillionaire”, stealth wealth is about being wealthy without people knowing about it. Let’s be clear: this isn’t about hiding money away from the authorities; it’s about being aware of your surroundings’ possible responses to money and riches.

Stealth wealth is a mindset, a way of life, focusing less on bling-bling, status symbols, luxury cars, big houses, and all that stuff.

To continue reading, please go to the original article here:

How Much Cash To Have Stashed at Home at All Times

How Much Cash To Have Stashed at Home at All Times

Jordan Rosenfeld Mon, January 16, 2023

Digital payment platforms like Venmo, PayPal and CashApp have changed the way we use and keep physical cash on hand. Most people rarely keep cash on their person, much less at home. However, there are always unexpected events that can lead to a necessity for having a bit of cash on hand, particularly emergencies ranging from catastrophic weather (hurricanes, wildfire), to power outages. If you can’t access your digital currency or your banking systems are down, having cash can allow you to get gas, food, and medicines with ease.

How Much Cash To Have Stashed at Home at All Times

Jordan Rosenfeld Mon, January 16, 2023

Digital payment platforms like Venmo, PayPal and CashApp have changed the way we use and keep physical cash on hand. Most people rarely keep cash on their person, much less at home. However, there are always unexpected events that can lead to a necessity for having a bit of cash on hand, particularly emergencies ranging from catastrophic weather (hurricanes, wildfire), to power outages. If you can’t access your digital currency or your banking systems are down, having cash can allow you to get gas, food, and medicines with ease.

However, just how much cash should you have on hand? We asked experts to weigh in and the answer is: It depends.

Keep Cash to a Minimum

From a security point of view, cash is the most insecure asset you can have. Keeping it to a minimum in the house in the case of fire or theft is a good rule of thumb, said Ryan McCarty, CFP from McCarty Money Matters.

Just how minimum is up for debate among financial experts. Danielle Miura, CFP, the founder and owner of Spark Financials, suggested, “You should keep enough money on hand to get you a couple of gallons of gas, pay for a delivery tip, or to help in unfortunate events,” or around $100-$200 at a time. “Emergency funds should not be held at your home, they should be stored in a high-yield savings account of your choice.”

McCarty framed it more in terms of a ratio: “In terms of amount, don’t let your cash exceed 10% of your overall emergency fund and/or $10,000. You can’t deposit more than $10,000 in cash in a given year without raising red flags with the IRS.”

Enough for Emergency Expenses

Yasmin Purnell, a personal finance expert and founder of The Wallet Moth, a finance website, suggested you keep enough cash on hand in case of an emergency that would require you to access “temporary accommodation, food and drink, gasoline, and medication.” Purnell added, “As a general rule of thumb, having access to $1,000 in cash at home would ensure you can at least pay for immediate expenses in the case of a national emergency.”

Ted Capwell, an investment manager and co-founder of Safe Trade Binary Options, a financial news website, suggests that instead of keeping cash for this kind of emergency, you could keep staples. “For example, instead of keeping $500 for food, buy frozen food and store them in a refrigerator. Or buy an emergency kit instead of keeping money for hospital bills.”

To continue reading, please go to the original article here:

https://finance.yahoo.com/news/much-cash-keep-home-times-180337690.html

The Easiest 833x Return You Will Ever Make

The Easiest 833x Return You Will Ever Make

January 16, 2023 Simon Black, Founder Sovereign Research & Advisory

At precisely 8:13PM eastern time on the evening of October 28, 2003, a lonely 19-year old schoolboy took to the Internet to complain about the latest love interest who had left him dejected and angry.

“Jessica,” he wrote to the precisely zero people who paid attention to his LiveJournal blog, “is a bitch. I need to think of something to take my mind off her. I need to think of something to occupy my mind. Easy enough, now I just need an idea.”

The Easiest 833x Return You Will Ever Make

January 16, 2023 Simon Black, Founder Sovereign Research & Advisory

At precisely 8:13PM eastern time on the evening of October 28, 2003, a lonely 19-year old schoolboy took to the Internet to complain about the latest love interest who had left him dejected and angry.

“Jessica,” he wrote to the precisely zero people who paid attention to his LiveJournal blog, “is a bitch. I need to think of something to take my mind off her. I need to think of something to occupy my mind. Easy enough, now I just need an idea.”

It took about an 90 minutes… and a fair amount of booze… for inspiration to strike. And by 9:48PM he wrote an updated post, describing his “idea”.

He wanted to hack into the school’s official servers and download the photographs of every student on campus; he would then write a program that would randomly select two of those photos, place them side-by-side on a website, and allow other students to vote on who was more attractive.

At 11:09PM, his new website was complete. He called it FaceMash, and it attracted 22,000 page views in the first four hours.

The website’s creator, of course, is Mark Zuckerberg. And his FaceMash site eventually went on to become Facebook (originally called ‘The’ Facebook).

It was an instant sensation among users and quickly began to attract venture capital firms. Investor Peter Thiel bought 10% of the company for $500,000 the following year, in September 2004.

Three years later it was worth $15 billion. And when the company went public in May of 2012, it was worth more than $100 billion.

Today Facebook’s stock market capitalization is about $350 billion. So investors who bought in at the IPO 12 years ago have made about 3.5x their money, or about 12% per year. That’s a very solid return.

And of course, investors who were able to buy Facebook shares when it was still private are up 20x or more, which is incredible.

But returns like this are nothing compared to another investment where you can easily and consistently return 100x to 1,000x.

I’m talking about tomatoes.

Yes I’m serious.

Think about it: you can buy a pack of 100 organic, non-GMO ‘beefsteak’ tomato seeds for about three bucks (real price at WalMart). That works out to be 3 cents per seed.

It takes minutes (really seconds) to plant a tomato seed, after which, within a week or two, life will come bursting out of the soil. Before long, a full, healthy plant will have grown and begin producing tomatoes.

One plant can yield about 10 pounds of tomatoes. And even at a discount grocer, organic tomatoes cost at least $2.50 per pound.

So from a single seed (3c investment), you get $25 worth of tomatoes… a return of 833x. And given how quickly tomatoes grow, you can generate that 833x return in about four months. Pretty astonishing.

Now, tomatoes obviously require a little bit of work. They need some water, and, depending on where you live, occasional weeding and de-pesting.

But any investment requires work. Even owning Facebook stock means keeping up with quarterly reports and earnings calls (which any investor should absolutely be doing). And frankly it’s a lot more fun to be out in the garden than analyzing a company’s annual financial audit.

It’s not just tomatoes either. A lot of micro-scale agriculture comes with ridiculously high returns.

An egg-laying chicken, depending on breed, can run around $30 (though some are cheaper and others more expensive).

Chickens lay roughly 1 egg per day under the right conditions. And at roughly 30c per free-range, organic egg at the grocery store, your investment return works out to be 1% PER DAY. Junk bonds, by comparison, yield around 8% per year.

Fruit trees are another great example. A backyard apple tree can cost around $20 to $30, and, depending on species and other factors, it can yield about 50 pounds per season after several years once it begins bearing fruit.

At $1.50 per pound of organic apples, that’s $75, or about 3x per season. And the trees can produce for decades… so you could end up making 100x or more, while also increasing the value of your home.

Now, my point here isn’t to encourage you to become a tree farmer or to start raising chickens in your backyard… and certainly not to abandon sensible financial investments.

(Nor do I want to trivialize agriculture; just like any other kind of investing, you have to know what you’re doing in order for it to work.)

But we do live in a bizarre world where pessimism seems to be a dominant force. And it’s easy to understand why.

This ridiculous war is dragging on forever. Inflation is still far too high. Politicians are still far too destructive. Corporate layoffs are piling up. The stock market is falling.

Plus everyone seems to be talking about recession. ‘Experts’ are making predictions about how likely it will happen, when it will come, how severe it will be, etc. Their gloom is almost becoming a self-fulfilling prophecy.

The anticipation alone is agonizing; these forecasts for recession are like waiting on pins and needles for the oncologist to call with our cancer screening results: good or bad, we just want to get on with it already.

So it’s easy to feel frustrated these days, and even a little bit out of control.

And my comments on micro-scale agriculture are really just to show that there are small opportunities available to us every day to take back control.

It doesn’t have to be complicated or exotic.

Something as simple as planting a tomato seed is an easy way to start taking back control… while generating a return that makes Facebook stock look pitiful by comparison.

To your freedom, Simon Black, Founder Sovereign Research & Advisory

https://www.sovereignman.com/investing/the-easiest-833x-return-you-will-ever-make-145153/

6 Smart Hiding Spots for Your Emergency Cash

6 Smart Hiding Spots for Your Emergency Cash

Life savings ready to to be buried in the back yard.

Those who keep extra money, like an emergency fund, in their homes may be curious about some of the best spaces to store it. Since traditional savings vehicles like high-yield savings accounts are not applicable in this situation, those in possession of excess funds need to get creative with where they keep this money.

Consider stashing your emergency cash into some of these clever spots.

6 Smart Hiding Spots for Your Emergency Cash

Life savings ready to to be buried in the back yard.

Those who keep extra money, like an emergency fund, in their homes may be curious about some of the best spaces to store it. Since traditional savings vehicles like high-yield savings accounts are not applicable in this situation, those in possession of excess funds need to get creative with where they keep this money.

Consider stashing your emergency cash into some of these clever spots.

Fake Personal Items

This is a helpful tip for those traveling overseas as well as those seeking hacks for keeping their money safe at home. Consider fake personal items, like the following, to discreetly store any emergency funds:

A hairbrush. Use a round hairbrush with a hollowed-out middle and store cash inside the brush.

Empty lip balm tubes. Do you need to tuck a tiny bit of cash somewhere safe? Store it inside an empty lip balm tube. Try a sunscreen lotion tube or an empty shaving can if you need a larger container for your savings. Always make sure the tubes are cleaned out before use!

Feminine napkins. Carefully open a sanitary napkin and hide folded money inside it. Then, fold it all back up and re-stick the sticker in place. These items are seldom, if ever, suspected for hiding excessive amounts of cash.

Remember, though: When storing emergency cash in fake personal items, keep the items tucked away in places you won’t forget.

The Bathroom

When it comes to hiding emergency cash, there are a number of hidden spaces inside your bathroom where the money can be easily stashed.

One of the most common is the toilet’s water tank. Seal your emergency cash into a jar or another watertight container to ensure it doesn’t get wet and store it carefully inside. A toilet’s water tank also makes for a great place to store other valuable items beyond emergency cash, like jewelry or stock certificates. (Again, we can’t stress enough the importance of storing these items into watertight containers.)

Where else in the bathroom can you hide emergency cash? Have you tried using your toilet spring bar? The spring bar is what holds your toilet paper roll in place. Carefully take it apart, roll up extra money, put it inside and reassemble into place.

Fake Electrical Outlets

It’s becoming much more popular for homeowners to construct fake infrastructure in their homes where you can hide emergency cash inside.

To continue reading, please go to the original article here:

https://www.gobankingrates.com/money/financial-planning/hidden-places-to-stash-your-emergency-cash/

10 Genius Things Warren Buffett Says To Do With Your Money

10 Genius Things Warren Buffett Says To Do With Your Money

Elyssa Kirkham Sun, January 15, 2023

Warren Buffett is arguably the best-known, most-respected investor of all time. Buffett is also known for his folksy charm and his memorable quotes about the art of investing.

When you're aiming to reach the top of the mountain, it's usually wise to closely follow the footprints of those who have successfully made the climb before you. Your odds of investing success can increase exponentially if you learn and apply Buffett's best investing tips.

10 Genius Things Warren Buffett Says To Do With Your Money

Elyssa Kirkham Sun, January 15, 2023

Warren Buffett is arguably the best-known, most-respected investor of all time. Buffett is also known for his folksy charm and his memorable quotes about the art of investing.

When you're aiming to reach the top of the mountain, it's usually wise to closely follow the footprints of those who have successfully made the climb before you. Your odds of investing success can increase exponentially if you learn and apply Buffett's best investing tips.

1. Never Lose Money

One of the most popular pieces of Buffett advice is as follows: "Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1." If you're working from a loss, it's that much harder to get back to where you started, let alone to earn gains.

2. Get High Value at a Low Price

In the 2008 Berkshire Hathaway shareholder letter, Buffett shared another key principle: "Price is what you pay; value is what you get." Losing money can happen when you pay a price that doesn't match the value you get -- such as when you pay high interest on credit card debt or spend on items you'll rarely use.

Instead, live modestly like Buffett by looking for opportunities to get more value at a lower price. "Whether we're talking about socks or stocks, I like buying quality merchandise when it is marked down," Buffett wrote.

3. Form Healthy Money Habits

In a 2007 address at the University of Florida, Buffett said, "Most behavior is habitual, and they say that the chains of habit are too light to be felt until they are too heavy to be broken." Work on building positive money habits, and breaking those that hurt your wallet.

4. Avoid Debt, Especially Credit Card Debt

Buffett built his wealth by getting interest to work for him -- instead of working to pay interest, as many Americans do. "I've seen more people fail because of liquor and leverage -- leverage being borrowed money," Buffett said in a 1991 speech at the University of Notre Dame. "You really don't need leverage in this world much. If you're smart, you're going to make a lot of money without borrowing."

To continue reading, please go to the original article here:

https://finance.yahoo.com/news/10-genius-things-warren-buffett-190031207.html

How To Pass On Your Wealth, According to Experts

How To Pass On Your Wealth, According to Experts

Andrew Lisa Thu, January 12, 2023

It’s hard to imagine that anyone looks forward to planning how their stuff will be divvied up after they die. But taking the time to ensure a smooth transfer of wealth could be your final act of selflessness — and your posterity will certainly be grateful for your efforts.

“Having a well-thought-out plan prepared in writing by an estate planning attorney is essential,” said estate planning and wealth transfer attorney Robert E. Kabacy of Kell, Alterman & Runstein, L.L.P. “Without a plan, even though statutes define how an estate is handled, heirs are sometimes left with questions.”

How To Pass On Your Wealth, According to Experts

Andrew Lisa Thu, January 12, 2023

It’s hard to imagine that anyone looks forward to planning how their stuff will be divvied up after they die. But taking the time to ensure a smooth transfer of wealth could be your final act of selflessness — and your posterity will certainly be grateful for your efforts.

“Having a well-thought-out plan prepared in writing by an estate planning attorney is essential,” said estate planning and wealth transfer attorney Robert E. Kabacy of Kell, Alterman & Runstein, L.L.P. “Without a plan, even though statutes define how an estate is handled, heirs are sometimes left with questions.”

Questions are just the start of what can go wrong if you neglect to make arrangements.

A poorly planned transfer of wealth can saddle your beneficiaries with high fees, unnecessary tax obligations and, worst of all, foster infighting, resentment and prolonged legal battles among your heirs.

The good news is that a little bit of planning can prevent all of those unfortunate outcomes and enshrine your legacy for generations to come.

If Nothing Else, Write a Will

The most basic tool in the wealth-transfer process is a will, which provides a record of your wishes. Without one, the state — and your heirs — are left guessing.

“A will is used to designate how you want your assets distributed to your surviving loved ones upon your death,” said estate planning attorney Tim Hurban of Hurban Law. “If you die without a will, state law governs how your assets are distributed, which may or may not be in line with your wishes.”

Create a Written Inventory of Your Assets

Every will is only as good as the chronicling of assets that goes with it.

“The single most important thing you can do to insure that your wealth is passed onto your loved ones is to keep an inventory of your assets somewhere,” said Tim Hewson, CEO and co-founder of U.S. Legal Wills. “In your will, you typically refer to ‘my estate,’ and it is the responsibility of your executor to gather up that estate and distribute it to your beneficiaries according to the instructions in the will.”

The problem, according to Hewson, is that executors often have no idea what or where your assets are. That’s why it’s crucial to create a detailed record that includes the information, account numbers, logons and passwords needed to access them.

“A generation ago, our parents may have had two bank accounts and a monthly statement sent to them in the mail,” Hewson said. “Today our assets are distributed all over the place, including in online accounts.”

Consider a Trust To Add Clarity and Reduce Cost

To continue reading, please go to the original article here:

The Art and Science of Spending Money

The Art and Science of Spending Money

Jan 12, 2023 by Morgan Housel@morganhousel

Former General Electric CEO Jack Welch once nearly died of a heart attack. Years later he was asked what went through his mind while he was being rushed to the hospital in what could have been his last moments alive.

“Damn it, I didn’t spend enough money,” was Welch’s response. The interviewer, Stuart Varney, was puzzled, and asked why in the world that would go through his mind.

“We all are products of our background,” Welch said. “I didn’t have two nickels to rub together [when I was young], so I’m relatively cheap. I always bought cheap wine.”

After the heart attack Welch said he “swore to God I’d never buy a bottle of wine for less than a hundred dollars. That was absolutely one of the takeaways from that experience.”

“Is that it?” Varney asks, stunned.

“That’s about it,” says Welch.

The Art and Science of Spending Money

Jan 12, 2023 by Morgan Housel@morganhousel

Former General Electric CEO Jack Welch once nearly died of a heart attack. Years later he was asked what went through his mind while he was being rushed to the hospital in what could have been his last moments alive.

“Damn it, I didn’t spend enough money,” was Welch’s response. The interviewer, Stuart Varney, was puzzled, and asked why in the world that would go through his mind.

“We all are products of our background,” Welch said. “I didn’t have two nickels to rub together [when I was young], so I’m relatively cheap. I always bought cheap wine.”

After the heart attack Welch said he “swore to God I’d never buy a bottle of wine for less than a hundred dollars. That was absolutely one of the takeaways from that experience.”

“Is that it?” Varney asks, stunned.

“That’s about it,” says Welch.

Money is so complicated. There’s a human element that can defy logic – it’s personal, it’s messy, it’s emotional.

Behavioral finance is now well documented. But most of the attention goes to how people invest. Welch’s story shows how much deeper the psychology of money can go. How you spend money can reveal an existential struggle of what you find valuable in life, who you want to spend time with, why you chose your career, and the kind of attention you want from other people.

There is a science to spending money – how to find a bargain, how to make a budget, things like that.

But there’s also an art to spending. A part that can’t be quantified and varies person to person.

In my book I called money “the greatest show on earth” because of its ability to reveal things about people’s character and values. How people invest their money tends to be hidden from view. But how they spend is far more visible, so what it shows about who you are can be even more insightful.

Everyone’s different, which is part of what makes this topic fascinating. There are no black-and-white rules. But here are a few things I’ve noticed about the art of spending money.

1. Your family background and past experiences heavily influences your spending preferences.

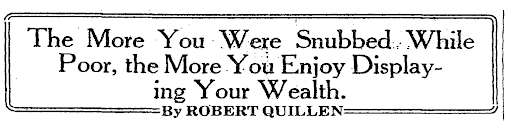

I love this Washington Post headline from June, 1927 – the Roaring ‘20s, the last hurrah before the Great Depression:

This is timeless, and explains so much.

After Covid lockdowns there was the concept of “revenge spending” – a furious blast of conspicuous consumption, letting out everything that had been pent up and held back in 2020.

Revenge spending happens at a broad level, too. The most stunning examples I’ve seen of this are wealthy adults who grew up poor – and were heckled, bullied, and teased for being poor as kids. Their revenge spending mentality can become permanent.

If you dig into it, I think you’ll see that a disproportionate share of those with the biggest homes, the fastest cars, and the shiniest jewelry, grew up “snubbed” in some way. Part of their current spending isn’t about getting value out of flashy material goods; it’s about healing a social wound inflicted when they were younger.

To continue reading, please go to the original article here: Long but well worth the time

https://collabfund.com/blog/the-art-and-science-of-spending-money/

These Historical Parallels Are Really Spooky

These Historical Parallels Are Really Spooky

Simon Black, Founder Sovereign Research & Advisory January 13, 2023

By the third century AD, it was hard to imagine Rome being in worse condition. Historians literally refer to this period in Roman history as the Crisis of the Third Century. And it was brutal.

Roman citizens couldn’t believe what they were experiencing... it was incomprehensible to them that their fatherland had become so weakened.

Inflation was running rampant. The Empire was stuck in a quagmire of foreign wars and had suffered some humiliating defeats.

These Historical Parallels Are Really Spooky

Simon Black, Founder Sovereign Research & Advisory January 13, 2023

By the third century AD, it was hard to imagine Rome being in worse condition. Historians literally refer to this period in Roman history as the Crisis of the Third Century. And it was brutal.

Roman citizens couldn’t believe what they were experiencing... it was incomprehensible to them that their fatherland had become so weakened.

Inflation was running rampant. The Empire was stuck in a quagmire of foreign wars and had suffered some humiliating defeats.

Rome experienced multiple bad pandemics, coupled with even worse government response.

Foreign invaders were flooding across their borders on a daily basis. Trade broke down, causing shortages in many vital goods.

And terrible social strife dominated people’s daily lives. Ordinary Roman citizens were at each other’s throats, and it was a time of disunity and outrage.

One contemporary writer of the era named Cyprian described the situation as follows:

“The World itself... testifies to its own declines by giving manifold concrete evidence of the process of decay... There is a decrease and deficiency in the field, of sailors on the sea, of soldiers in the barracks, of honesty in the marketplace, of justice in court, of concord in friendship, of skill in technique...”

Cyprian wasn’t just describing Rome’s obvious decline. Rather, his summary is an indictment of Rome’s inability to stop its decline.

Everyone in the imperial government knew what was happening in Rome. They simply lacked the ability to do anything about it.

Historian Arnold Toynbee called this the “Challenge and Response” effect... and it’s an interesting idea.

The concept is that every society has to deal with certain challenges; if the challenges are too great, the society will not survive... i.e. the desert is too harsh, the tundra is too frozen, etc.

But sometimes a society becomes so decadent, so prosperous, that it loses its ability to address challenges. It no longer has the social capital necessary— unity of purpose, the ability to compromise, the capacity to engage in rational debate.

That is the position where Rome found itself in the 3rd century AD. And I believe the West is quickly heading in this direction.

This is the subject of today’s podcast.

We start out talking about Rome’s mortal enemy... and how, after more than a century, Rome emerged victorious as the lone superpower in the Mediterrannean.

Everything was great, and peace and prosperity reigned for more than 200 years.

But over that time, the decadence set in. Wheras once Romans had valued hard work, freedom, and unity of purpose, their entire value system changed.

People expected, then demanded, to be taken care of by the state. Corruption became commonplace. The bureaucracy multiplied. Social conflict soared.

And eventually Rome lost the ability to meet its challenges.

I make a lot of historical parallels to our modern world, including some specific examples of absurdities which occurred just in the last couple of days.

But I also discuss why, in the end, these conditions actually create unique opportunity for creative, hard working, talented people.

You can listen to the podcast here.

To your freedom, Simon Black, Founder Sovereign Research & Advisory

https://www.sovereignman.com/podcast/challenge-and-response-145150/

7 Mistakes People Make When Choosing a Financial Advisor

7 Mistakes People Make When Choosing a Financial Advisor

Helping people make smart financial decisions

SmartAsset -- January 2023

Choosing a financial advisor is a major life decision that can determine your financial trajectory for years to come.

A 2020 Northwestern Mutual study found that 71% of U.S. adults admit their financial planning needs improvement. However, only 29% of Americans work with a financial advisor.1

The value of working with a financial advisor varies by person and advisors are legally prohibited from promising returns, but research suggests people who work with a financial advisor feel more at ease about their finances and could end up with about 15% more money to spend in retirement.2

7 Mistakes People Make When Choosing a Financial Advisor

Helping people make smart financial decisions

SmartAsset -- January 2023

Choosing a financial advisor is a major life decision that can determine your financial trajectory for years to come.

A 2020 Northwestern Mutual study found that 71% of U.S. adults admit their financial planning needs improvement. However, only 29% of Americans work with a financial advisor.1

The value of working with a financial advisor varies by person and advisors are legally prohibited from promising returns, but research suggests people who work with a financial advisor feel more at ease about their finances and could end up with about 15% more money to spend in retirement.2

Consider this example: A recent Vanguard study found that, on average, a hypothetical $500K investment would grow to over $3.4 million under the care of an advisor over 25 years, whereas the expected value from self-management would be $1.69 million, or 50% less. In other words, an advisor-managed portfolio would average 8% annualized growth over a 25-year period, compared to 5% from a self-managed portfolio.3

Being aware of these seven common blunders when choosing an advisor can help you find peace of mind, and potentially avoid years of stress.

1. Hiring an Advisor Who Is Not a Fiduciary

By definition, a fiduciary is an individual who is ethically bound to act in another person’s best interest. Fiduciary financial advisors must avoid conflicts of interest and disclose any potential conflicts of interest to clients.

All of the financial advisors on SmartAsset’s matching platform are registered fiduciaries. If your advisor is not a fiduciary and constantly pushes investment products on you, use this no-cost tool to find an advisor who has your best interest in mind.

2. Hiring the First Advisor You Meet

While it’s tempting to hire the advisor closest to home or the first advisor in the yellow pages, this decision requires more time. Take the time to interview at least a few advisors before picking the best match for you.

3. Choosing an Advisor with the Wrong Specialty

To continue reading, please go to the original article here: