6 Ways You Can Tell If a Recession Is Coming (And What To Do)

I’m an Economist: 6 Ways You Can Tell If a Recession Is Coming (And What To Do)

Laura Beck Tue, September 3, 2024 GOBankingRates

Most people are worried about the economy, and the dreaded word “recession” is on many people’s lips. But how can you tell what’s actually happening and what’s not worth worrying about?

GOBankingRates spoke to economists and financial professionals to get the inside scoop on what’s going on in America right now. Here are six ways to tell if a recession is coming and what you can do about it.

Current Economic Outlook

Michael Faulkender, former assistant secretary for economic policy at the U.S. Department of Treasury and currently the dean’s professor of finance at the University of Maryland, provided a measured perspective.

I’m an Economist: 6 Ways You Can Tell If a Recession Is Coming (And What To Do)

Laura Beck Tue, September 3, 2024 GOBankingRates

Most people are worried about the economy, and the dreaded word “recession” is on many people’s lips. But how can you tell what’s actually happening and what’s not worth worrying about?

GOBankingRates spoke to economists and financial professionals to get the inside scoop on what’s going on in America right now. Here are six ways to tell if a recession is coming and what you can do about it.

Current Economic Outlook

Michael Faulkender, former assistant secretary for economic policy at the U.S. Department of Treasury and currently the dean’s professor of finance at the University of Maryland, provided a measured perspective.

“I do not think a recession is coming but I do think the recent slowdown will continue. There are parts of the economy that are not growing — manufacturing and housing are still struggling,” he outlined. “Other parts like healthcare and government spending are still expanding. The outcome is overall anemic growth, but not yet decline. What the economy looks like one to two years from now depends mightily on the economic policies implemented following the election.”

However, Albert “Pete” Kyle, distinguished university professor at the University of Maryland’s Robert H. Smith School of Business, offered a more cautious view.

“Altogether, risks are tilted towards a recession coming either later this year or next year, but it is not as obvious that this will occur as it was in 2007 or 2000,” he said. “Currently, there are some stresses in the banking system. Banks and non-bank investors are sitting on bad loans related to commercial real estate, particularly shopping malls and commercial office space. These stresses are significant. Compared to the 2008 financial crisis, they are better recognized and probably not as severe.”

Kyle also pointed out another concerning factor — the stock market.

“The stock market is currently at a very high level as a multiple of GDP,” the professor shared. “While earnings are strong, it is not clear whether for how long these high earnings will continue into the future. If there is a decline in corporate earnings, stock prices could fall a great deal.”

Professor Jonathan Ernest of Case Western Reserve University offered a more optimistic perspective. “Currently, the labor market has remained relatively strong, the rate of inflation has decreased, and GDP continues to grow year-over-year. None of these measures would traditionally signal an imminent recession.”

6 Key Recession Indicators

Given these differing views, what signs should we be watching for? Here are six key indicators highlighted by our experts.

Yield Curve Inversion and Steepening

Abe Askil, CEO at Titan Capital Managers, pointed to a historically reliable indicator.

TO READ MORE: https://news.yahoo.com/news/finance/news/m-economist-6-ways-tell-170258745.html

Regulation D And Savings Account Withdrawal Limits – Here’s What Changed

Regulation D And Savings Account Withdrawal Limits – Here’s What Changed

Matthew Goldberg Tue, September 3, 2024 Bankrate

Key takeaways

Regulation D sets reserve requirements for banks and credit unions, and it previously limited the amount of certain types of withdrawals and transfers consumers could make to six.

During the coronavirus pandemic, the limitation was lifted.

Some financial firms now allow consumers to make more than six withdrawals and transfers from deposit accounts while others have maintained the pre-2020 rule.

While banks historically limited the number of transactions that customers could make each month in savings and money market accounts, a pandemic-era rule change means you may now have easier access to your funds.

Regulation D, or Reg. D, is a Federal Reserve Board rule that previously limited withdrawals and transfers to six each statement cycle. The Fed revised the rule, but many banks have maintained the six-transaction limit. Others have increased the number of allowable withdrawals and transfers.

Regulation D And Savings Account Withdrawal Limits – Here’s What Changed

Matthew Goldberg Tue, September 3, 2024 Bankrate

Key takeaways

Regulation D sets reserve requirements for banks and credit unions, and it previously limited the amount of certain types of withdrawals and transfers consumers could make to six.

During the coronavirus pandemic, the limitation was lifted.

Some financial firms now allow consumers to make more than six withdrawals and transfers from deposit accounts while others have maintained the pre-2020 rule.

While banks historically limited the number of transactions that customers could make each month in savings and money market accounts, a pandemic-era rule change means you may now have easier access to your funds.

Regulation D, or Reg. D, is a Federal Reserve Board rule that previously limited withdrawals and transfers to six each statement cycle. The Fed revised the rule, but many banks have maintained the six-transaction limit. Others have increased the number of allowable withdrawals and transfers.

What is Regulation D?

Reg. D imposed reserve requirements on a bank’s deposits and other liabilities, with the purpose of implementing monetary policy, according to the Federal Reserve. In March 2020, reserve requirements at banks were reduced to zero percent and they’ve remained at zero for more than three years.

Reg. D also restricted the frequency of certain types of withdrawals and transfers you could make from a savings deposit account during a statement cycle. Banks no longer have to limit the number of certain withdrawals from a savings deposit account to six, but most do still restrict withdrawals on these accounts.

How Has Regulation D Changed?

In April 2020 — as Americans began to navigate the economic fallout from the coronavirus pandemic — the Fed deleted the six certain transfer or withdrawal limits from the definition of savings deposit accounts via an interim final rule.

Some banks took the Fed up on the rule change by eliminating the withdrawal limits. American Express National Bank, for example, previously allowed nine withdrawals per statement cycle, for example. Now, it doesn’t have withdrawal limits on its savings account.

The Fed’s move was termed an interim final rule, which is issued when there’s good cause to skip issuing a proposed rule, says Scott Birrenkott, assistant director of legal at the Wisconsin Bankers Association.

Still, the proposal isn’t yet set in stone.

“The Fed still hasn’t issued a final rule,” Birrenkott says. “So, some banks are still waiting for that final piece to kind of see. I know that some banks are curious whether that might change or something might be reversed, because it can be a big step to adjust all of their policies and procedures.”

Types Of Transactions Impacted By Reg. D

TO READ MORE: https://www.yahoo.com/finance/news/regulation-d-savings-account-withdrawal-195856860.html

High-Yield Savings Account Vs. Treasury Bill: Which Is Right For You?

High-Yield Savings Account Vs. Treasury Bill: Which Is Right For You?

Sarah C. Brady·Contributor Updated Tue, September 3, 2024 Yahoo Personal Finance

Both can be a great option for your savings, depending on your goals.

It was not too long ago that low-risk investments like Treasury bills were the underdogs of the financial world. While T-bills provide a safe place to store your savings while earning a fixed interest rate, they were simply not worth the low returns they offered — especially when compared to the flexibility of savings accounts.

Then, in 2022, something unusual happened: Interest rates started increasing, and they just kept on shooting upward, until the rates on some T-bills, and even savings accounts, passed 5%.

High-Yield Savings Account Vs. Treasury Bill: Which Is Right For You?

Sarah C. Brady·Contributor Updated Tue, September 3, 2024 Yahoo Personal Finance

Both can be a great option for your savings, depending on your goals.

It was not too long ago that low-risk investments like Treasury bills were the underdogs of the financial world. While T-bills provide a safe place to store your savings while earning a fixed interest rate, they were simply not worth the low returns they offered — especially when compared to the flexibility of savings accounts.

Then, in 2022, something unusual happened: Interest rates started increasing, and they just kept on shooting upward, until the rates on some T-bills, and even savings accounts, passed 5%.

In 2024, anyone who wants to earn a competitive rate on their short-to-mid-term savings would be wise to consider both as options. Which one is best for you: A high-yield savings account or Treasury bill? The answer mainly depends on when you need your money back.

What is a high-yield savings account?

A savings account is a bank account designed to help you save money. These accounts typically earn more interest than checking accounts do, and they're very low risk since most banks insure your deposits up to $250,000.

The downside? Most savings accounts don’t pay much; the national average savings account rate is just 0.46% today. You might earn more interest by leaving your money in a time-bound account like a T-bill or CD, or by investing in the market. Inflation is also likely to outpace your earnings on a savings account.

One way to maximize what you earn on your savings is to use a high-yield savings account (HYSA). These accounts work just like traditional savings account, except they can offer rates as high as 5% APY or more.

See our picks for the 10 best high-yield savings accounts available today>>

What is a Treasury bill?

Buying a Treasury bill is sort of like making a loan to the U.S. government. T-bills pay you guaranteed interest based on the length of time you invest your money. Rates currently range from 4.23% to 5.27% with terms of four to 52 weeks. You can sell a T-bill before the maturity date, but you'll lose some of the interest you would have earned otherwise.

TO READ MORE:

Here’s Why Having 2 or 3 Bank Accounts Isn’t Enough,

Here’s Why Having 2 or 3 Bank Accounts Isn’t Enough, According to Money Expert Martin Lewis

Vance Cariaga Mon, September 2, 2024 GOBankingRates

Although there are vast differences in the amount of wealth Americans have amassed, one thing almost everyone has in common is a banking relationship. Nearly 96% of U.S. households have a checking or savings account at a bank or credit union, according to the latest FDIC data.

Research from Consumer Affairs showed that the average consumer had a total of 5.3 accounts across financial institutions as recently as 2019, though many have only one or two

Here’s Why Having 2 or 3 Bank Accounts Isn’t Enough, According to Money Expert Martin Lewis

Vance Cariaga Mon, September 2, 2024 GOBankingRates

Although there are vast differences in the amount of wealth Americans have amassed, one thing almost everyone has in common is a banking relationship. Nearly 96% of U.S. households have a checking or savings account at a bank or credit union, according to the latest FDIC data.

Research from Consumer Affairs showed that the average consumer had a total of 5.3 accounts across financial institutions as recently as 2019, though many have only one or two.

More Bank Accounts Could Mean Better Money Management

If you belong to the latter group, then financial guru Martin Lewis recommends adding more accounts. Lewis, founder of the UK-based MoneySavingExpert website, recently said on his podcast that you might benefit from having 10 accounts or more, The Express reported. He compared savings accounts to a “tower of champagne glasses” where you fill one glass and then move on to the next.

“The perfect way to save is you pour your money into the account that pays the most,” Lewis said. “It might be tax-free, it might be because it only allows a small amount. Once you fill that, you trickle down to the next level then trickle down to the next level.”

He conceded that this system is not necessarily for everyone — mainly because it requires hard work to stay on top of it.

“The biggest sin in savings is that most decent rates only last for a year or so and then you have to be on top of it to ditch and switch when it ends,” Lewis added. “It’s only for the type of people who will be constantly on top of it, maybe even modelling it through a spreadsheet to manage it well. Most people want a simpler solution with two, three, maybe four accounts at most but not going into 10 different accounts.”

TO READ MORE: https://www.yahoo.com/finance/news/why-having-2-3-bank-200019928.html

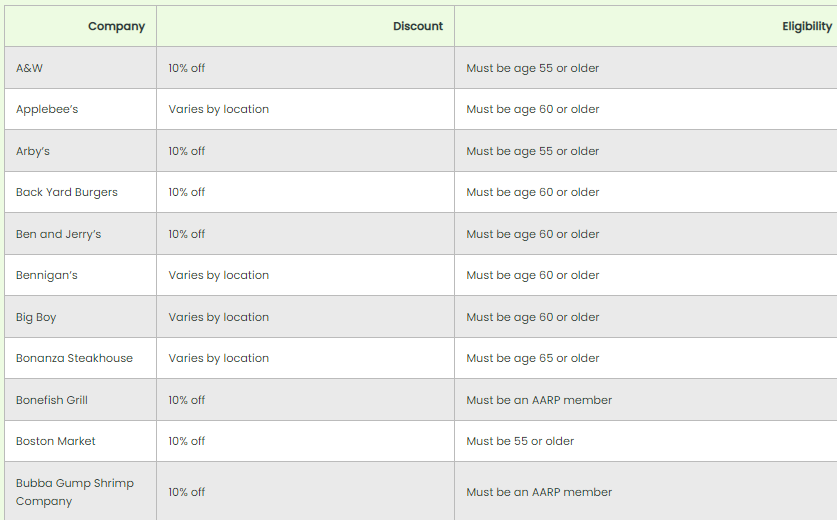

Every Senior Discount in America

Every Senior Discount in America

We’ve gone through and researched every company in America to see which ones offer discounts to seniors and retirees. Use our searchable database next time you’re stopping in at a store or restaurant to see if they offer an additional 10-50% off what you’re purchasing!

Every Senior Discount in America

We’ve gone through and researched every company in America to see which ones offer discounts to seniors and retirees. Use our searchable database next time you’re stopping in at a store or restaurant to see if they offer an additional 10-50% off what you’re purchasing!

TO READ MORE: https://retirehub.org/every-senior-discount/

16 Things Financial Advisors Never Do With Their Money

16 Things Financial Advisors Never Do With Their Money — and You Shouldn’t Either

Jennifer Taylor Sat, August 31, 2024 GOBankingRates

Financial advisors to help clients manage their money. As financial experts, they can offer advice on everything from investing to smart spending habits — but it can also be helpful to know what money moves they would never make themselves.

GOBankingRates spoke with a few financial advisors to find out what they would never do with their money. Here’s what they had to say.

16 Things Financial Advisors Never Do With Their Money — and You Shouldn’t Either

Jennifer Taylor Sat, August 31, 2024 GOBankingRates

Financial advisors to help clients manage their money. As financial experts, they can offer advice on everything from investing to smart spending habits — but it can also be helpful to know what money moves they would never make themselves.

GOBankingRates spoke with a few financial advisors to find out what they would never do with their money. Here’s what they had to say.

Ignore It

“Ignoring your money doesn’t make problems go away, nor does it lead to wealth,” said Christopher D. Musick, CFP, CKA, founder and financial planner at Purpose Financial Planning.

To be intentional with his cash flow, he sets time aside to budget monthly.

“I plan for how much is coming in, and what’s going toward spending, saving, giving, taxes and debt,” he said. “I also review my accounts regularly, including my investments.”

Use Consumer Debt

“I don’t take on debt to afford my lifestyle,” Musick said.

He said doing so isn’t sustainable.

“Car loans leave you in debt and paying interest on a depreciating asset,” he said. “Carrying credit card debt is even worse, as it often has higher interest rates and is typically used to fund immediate consumption, leaving you with nothing to show for that debt.”

He said consumer debt works against building wealth.

“It takes away from your net worth and constrains your future cash flow,” he said.

Invest My Emergency Fund

“I don’t want to worry about stock market volatility in the midst of an emergency,” Musick said. “My emergency fund is in a high-yield savings account (HYSA), but other options include things like CDs or money markets.”

He said he wants his emergency fund to be liquid, accessible and guaranteed to be there when he needs it.

Forget Taxes

“The last thing I want is to get surprised by a big tax bill in April,” Musick said.

Instead, he keeps a close watch on his earnings throughout the year to ensure he’s withholding enough taxes and determine if estimated taxes are necessary.

“I also look for tax-planning strategies that may help me lower what I owe in taxes now or in the future,” he said.

Keep It All for Myself

TO READ MORE: https://news.yahoo.com/news/finance/news/16-things-financial-advisors-never-160030886.html

Car Dealers Hate When You Ask These 3 Questions

Car Dealers Hate When You Ask These 3 Questions

Cynthia Measom Updated Fri, August 30, 2024 GOBankingRates

Buying a car can be stressful. Dealers may use tried-and-true tactics to push you into a quick sale, but knowing the right questions to ask can put you in the driver’s seat.

According to Mark Beneke, co-owner of Westland Auto Sales in Fresno, California, some questions potential buyers ask might make a dealer uncomfortable because they can reveal more about the vehicle’s true condition and history. Here are three questions that some car dealers dislike — and why they’re so important for you to ask.

Car Dealers Hate When You Ask These 3 Questions

Cynthia Measom Updated Fri, August 30, 2024 GOBankingRates

Buying a car can be stressful. Dealers may use tried-and-true tactics to push you into a quick sale, but knowing the right questions to ask can put you in the driver’s seat.

According to Mark Beneke, co-owner of Westland Auto Sales in Fresno, California, some questions potential buyers ask might make a dealer uncomfortable because they can reveal more about the vehicle’s true condition and history. Here are three questions that some car dealers dislike — and why they’re so important for you to ask.

Can I Take the Vehicle to My Mechanic To Inspect?

Why Ask: Beneke said that a third-party mechanic can provide an unbiased assessment of the car’s condition, potentially uncovering issues the dealer might have overlooked or may not take care of as part of their process. “This will also give you some insight into the attitude of the dealership and their confidence in their work,” he added.

Why Dealers Avoid It: Beneke explained that if a dealer is aware of issues with the car or isn’t confident in the quality of the work they provide, they might be hesitant to allow you to take the car to your own mechanic.

How Long Has the Vehicle Been on the Lot?

Why Ask: “Most dealerships buy their inventory through a form of credit line, so for each day that the vehicle sits on the lot, they are paying and losing the potential to buy and sell other vehicles,” explained Beneke. “Because of this, they may be more willing to negotiate the price to move the inventory.”

TO READ MORE: https://www.yahoo.com/finance/news/car-dealers-hate-ask-3-130004635.html

The Four Biggest Mistakes People Make When Buying A New Car

Edmunds: The Four Biggest Mistakes People Make When Buying A New Car

Josh Jacquot Updated Thu, August 29, 2024

Car buyers have more tools than ever to get the right vehicle at the right price. Still, mistakes can happen quite easily. Often, car buyers get blinded by emotion or rushed timing. Edmunds’ experts reveal the four biggest mistakes car shoppers often make and offer tips to avoid them.

Trading in a Vehicle with Negative Equity

Being upside down on a trade-in vehicle is occurring with increasing frequency. According to a recent Edmunds report, nearly one in four consumers who financed a new vehicle purchase with a trade-in during the second quarter of 2024 were underwater on their prior car loan.

Edmunds: The Four Biggest Mistakes People Make When Buying A New Car

Josh Jacquot Updated Thu, August 29, 2024

Car buyers have more tools than ever to get the right vehicle at the right price. Still, mistakes can happen quite easily. Often, car buyers get blinded by emotion or rushed timing. Edmunds’ experts reveal the four biggest mistakes car shoppers often make and offer tips to avoid them.

Trading in a Vehicle with Negative Equity

Being upside down on a trade-in vehicle is occurring with increasing frequency. According to a recent Edmunds report, nearly one in four consumers who financed a new vehicle purchase with a trade-in during the second quarter of 2024 were underwater on their prior car loan.

“Upside down,” “underwater” and “negative equity” are interchangeable terms for a bad situation: All three mean that the car owner owes more on the loan than the vehicle is worth. Not only has the number of upside-down trade-ins grown since 2022, but so has the amount owed on those loans.

If, for example, you are $5,000 upside down on your current vehicle and decide to trade in this car and buy a new one, you will have to pay the price of the new car plus the $5,000 you owe on the current car. Your monthly payments will be much higher because you’re rolling over what you owe on your old car to the loan on your new one.

The best financial solution is to keep your current car longer and continue paying off its loan. Waiting might be challenging — you want that new car, we get it — but if you can at least ensure your trade-in value equals your loan amount, you won’t have to pay extra for the new vehicle purchase.

Rushing Into a Vehicle Purchase

There can be legitimate reasons to expedite a vehicle purchase. Perhaps your vehicle was totaled in an accident, or maybe it broke down and it’s not worth paying to fix. Either way, you’ll need a new car right away. But many shoppers don’t think about doing valuable research beforehand.

There will be new and unfamiliar automotive features and technologies worth knowing about, especially if it’s been a while since you bought a new car. If you take your time, you’ll also be able to get several quotes before you commit to a deal and have time for a vehicle inspection if it’s a used car.

Even if you need to replace your car quickly, it’s often better to find alternative transportation while you research a new vehicle purchase. Renting a car for a few days might cost a few hundred dollars, but that’s better than picking the wrong vehicle or getting suckered into a bad deal.

TO READ MORE: https://www.yahoo.com/finance/news/edmunds-five-biggest-mistakes-people-112528264.html

5 Types of Financial Advisors — and How To Choose the Right One for You

Boomers: Here Are 5 Types of Financial Advisors — and How To Choose the Right One for You

Kellan Jansen Thu, August 29, 2024 GOBankingRates

We all need financial guidance from time to time. But the type of advice you need can depend on your age. Baby boomers, for example, often need support with stretching their funds in retirement and creating spending plans.

If you’re part of this generation and looking for a financial advisor, your search should reflect your goals. This article will lead you through a process that will get you to the right match.

The 5 Types of Financial Advisors

First, it’s worth reviewing how financial advisors earn money from their clients. There are a few different pricing models, and the one you choose could impact the kind of advice you get.

Boomers: Here Are 5 Types of Financial Advisors — and How To Choose the Right One for You

Kellan Jansen Thu, August 29, 2024 GOBankingRates

We all need financial guidance from time to time. But the type of advice you need can depend on your age. Baby boomers, for example, often need support with stretching their funds in retirement and creating spending plans.

If you’re part of this generation and looking for a financial advisor, your search should reflect your goals. This article will lead you through a process that will get you to the right match.

The 5 Types of Financial Advisors

First, it’s worth reviewing how financial advisors earn money from their clients. There are a few different pricing models, and the one you choose could impact the kind of advice you get.

For instance, if an advisor earns a commission on every trade you make and then recommends an unusually large number of trades, that’s a red flag. You might not spot something like that if you ignore how your advisor makes their money.

With that in mind, there are five main types of advisors, based on Securities and Exchange Commission regulations.

Fee-only: These advisors are paid based on the assets they manage for you. They may charge a percentage of those assets, an hourly rate or an annual fee.

Commission-based: These advisors earn a commission based on the products they sell you but may not charge you much, if anything, directly.

Fee-based: These advisors charge fees based on the assets they manage and may still earn a commission.

Registered investment advisors: These firms generally charge an annual account fee or a percentage of assets invested.

Robo-advisors: These automated online platforms offer low-cost investing advice and earn money through various account and trading fees.

You can find financial expertise across each of these pricing models. However, if you want your advisor’s incentives to align fully with your own, it’s a factor to consider.

How To Choose a Financial Advisor as a Boomer

The baby boomer generation spans 18 years, from 1946 to 1964. That means the youngest boomers are nearing retirement, while the oldest may have already been retired for a decade.

Given this gap, it’s no surprise that even people within the boomer generation have substantially different financial needs. However, with the right process, you’ll end up with a great advisor regardless of your needs. Here’s how to get there.

1. Define Your Goals

TO READ MORE: https://www.yahoo.com/finance/news/boomers-5-types-financial-advisors-140038347.html

4 Key Concepts and Strategies From a Finance Professor

Wealth Management 101: 4 Key Concepts and Strategies From a Finance Professor

Cindy Lamothe Tue, August 27, 2024 GOBankingRates

For most people, managing finances is not the funnest thing in the world. Maybe that’s why you’ve likely postponed it up until now. And maybe you’re truly interested in making a change but all of the financial jargon out there makes your head swim. How do you get started? What are the basics?

Thankfully, experts understand the challenge and are ready to break it down for you. Below, Robert R. Johnson, Ph.D., CFA and professor of finance at Creighton University‘s Heider College of Business, outlines some of the key concepts and strategies to know when it comes to wealth management.

Wealth Management 101: 4 Key Concepts and Strategies From a Finance Professor

Cindy Lamothe Tue, August 27, 2024 GOBankingRates

For most people, managing finances is not the funnest thing in the world. Maybe that’s why you’ve likely postponed it up until now. And maybe you’re truly interested in making a change but all of the financial jargon out there makes your head swim. How do you get started? What are the basics?

Thankfully, experts understand the challenge and are ready to break it down for you. Below, Robert R. Johnson, Ph.D., CFA and professor of finance at Creighton University‘s Heider College of Business, outlines some of the key concepts and strategies to know when it comes to wealth management.

Start With Limiting Debt

According to Johnson, people would be well served to realize that debt extinguishment should be a priority.

“To quote Albert Einstein, ‘Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.’

Johnson added, “People can put their financial house in order by reducing debt and acquiring assets that grow in value over time.”

He said the fastest way to improve your net worth is to obtain more assets that compound in value (e.g., stocks and CDs) and reduce your debts and interest payments.

“Typically, one should pay down the highest interest rate debt first,” he said. “And that is generally high interest rate credit card debt.”

Understand Not All Debt Is Bad

“Not all debt is bad,” Johnson said. “Some experts would contend that student loans are bad debt, but I disagree. I would categorize modest student loan debt as being good debt.”

In his opinion, student loans get a bad rap.

“There is no doubt that the system has been abused and that some students have accumulated a mountain of debt and have earned degrees that simply won’t provide the earning power to pay that debt back.”

But, used judiciously — and to earn degrees that truly build your human capital and earning power — Johnson said student loans can be essential bridges to career success.

Mortgage debt also can be considered good debt. Johnson cautioned against comparing mortgage interest against investment interest, because mortgage interest is tax deductible.

TO READ MORE: https://www.yahoo.com/finance/news/wealth-management-101-4-key-170229585.html

If A Neighbor's Tree Falls On Your Property, Who Has To Pay For The Damage?

If A Neighbor's Tree Falls On Your Property, Who Has To Pay For The Damage?

Maurie Backman Updated Thu, Aug 22, 2024,

This year has already seen a host of named storms. In July, Hurricane Beryl became the earliest category-5 Atlantic storm on record. And in August, Hurricane Debby hammered the Southeast before moving upward to inflict damage on the Northeast.

The National Oceanic and Atmospheric Administration predicts that the coming months are likely to be active ones as far as storms go. In the course of its routine mid-season update, it increased the number of anticipated named storms to 17-24, of which 8-13 could become hurricanes. And given that hurricane season runs through November 30, homeowners in the path of hurricanes and tropical storms could be in for a world of misery.

If A Neighbor's Tree Falls On Your Property, Who Has To Pay For The Damage?

Maurie Backman Updated Thu, Aug 22, 2024,

This year has already seen a host of named storms. In July, Hurricane Beryl became the earliest category-5 Atlantic storm on record. And in August, Hurricane Debby hammered the Southeast before moving upward to inflict damage on the Northeast.

The National Oceanic and Atmospheric Administration predicts that the coming months are likely to be active ones as far as storms go. In the course of its routine mid-season update, it increased the number of anticipated named storms to 17-24, of which 8-13 could become hurricanes. And given that hurricane season runs through November 30, homeowners in the path of hurricanes and tropical storms could be in for a world of misery.

It’s common for homes to sustain flood damage during a hurricane. And unfortunately, that’s not always covered by a standard homeowners insurance policy. Similarly, major storms tend to send trees flying, which could lead to all sorts of problems.

But what if a tree on a neighbor’s property ends up falling during a storm and causing damage to your property — whether by taking out a chunk of your fence, hitting your roof or falling on your car? Who is responsible for the damage? The answer might surprise you.

Who's Liable For Damages?

Laws regarding liability are more clear in some states than others, but generally speaking, when a tree falls during a storm it’s considered an act of nature. And in many cases, it’s not your neighbor’s financial responsibility, even if it was their tree that fell from their property onto yours and caused damage.

However, there can be exceptions to this rule. If it can be proven that your neighbor knew about structural problems with the tree, or that it was dead or rotted, and they failed to do anything about it, then you may be able to pin them for damages.

For example, say you sent your neighbor a series of emails asking them to take down a dead tree that’s been teetering over your fence. If your neighbor’s response was an emphatic “no” each time, and you have that paper trail, you may be able to use it as evidence against them.

But if a healthy tree falls onto your property, or even an unhealthy tree whose issues were unbeknownst to you and your neighbor, then you might be the one who’s going to have to deal with the damage.

What To Do When A Neighbor's Tree Damages Your Property

TO READ MORE: https://finance.yahoo.com/news/neighbors-tree-falls-property-pay-105000020.html