The Overfinancialization of Everything

The Overfinancialization of Everything

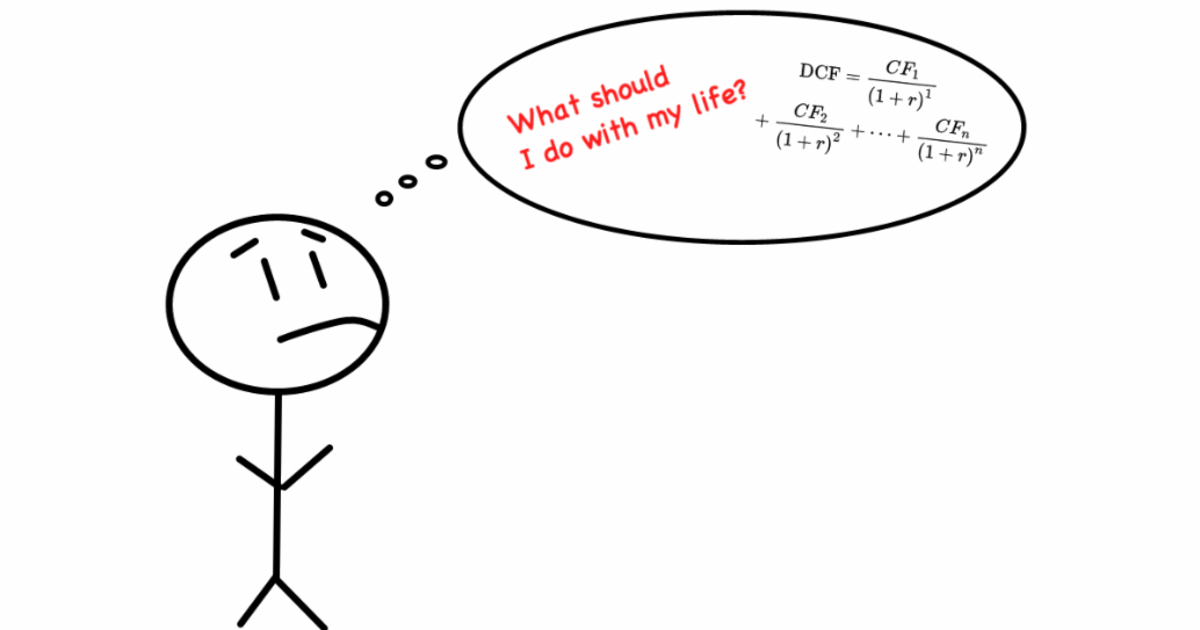

You can't DCF your life.

Author Jack Raines September 08, 2022

If you are addicted to social media (I am), you probably saw a certain "net worth" TikTok make the rounds last week. If you don't want to watch this embodiment of pure cringe, I'll give you a quick summary:

Guy with $500k net worth (really cool!) goes on a date night with his wife. He repeatedly checks his ($500k) net worth at dinner to ensure they are still on track for their portfolio goals, before ordering two $13 cocktails.

The Overfinancialization of Everything

You can't DCF your life.

Author Jack Raines September 08, 2022

If you are addicted to social media (I am), you probably saw a certain "net worth" TikTok make the rounds last week. If you don't want to watch this embodiment of pure cringe, I'll give you a quick summary:

Guy with $500k net worth (really cool!) goes on a date night with his wife. He repeatedly checks his ($500k) net worth at dinner to ensure they are still on track for their portfolio goals, before ordering two $13 cocktails. LINK

Seriously.

Our man was quite proud of his fiscally responsible decision-making. I imagine if the market had been red that morning, his wife would have been stuck with a ham sandwich and water for dinner.

This video was (rightfully) dunked on across social media, but this dude's behavior isn't as farfetched as it first appears. While most of us aren't basing our date night budgets on the intra-day movements of the S&P 500, we are guilty of more subtle examples of this same phenomenon:

The overfinancialization of everything.

As many of you know, I'm in business school right now. The decision of whether or not one should attend graduate school is quite common for mid-to-late 20-somethings these days, but how does one figure out what they "should" do?

Typically, we ask if it makes financial sense.

Many of you are probably familiar with discounted cash flows, or DCFs. For those who aren't, DCFs are financial models that we use to estimate the value of a company now based on our projections of a company's cash flows in the future. You model estimates for cash flows for X number of years, and you use a "discount rate" to calculate what those future earnings would be worth in today's dollars.

In layman's terms, a DCF can model the current value of your future earnings in different scenarios.

Oftentimes, especially for people already working in high-paying jobs, the math says "No!" to graduate school. If you are making $150,000 per year for example, why would you abandon two prime working years to take on $100,000+ in debt to go back to school?

The numbers just don't make sense.

To continue reading, please go to the original article here:

Six Types of Wealth

Six Types of Wealth

Author Jack Raines September 01, 2022

Wealth /welTH/ noun: An abundance of valuable material possessions or resources

Merriam-Webster Dictionary

Being rich isn't just a money thing. What comes to mind when you think of wealth? A list of America's ten richest people? Your neighbor with the bigger house, nicer car, and mountain home in Aspen? The multimillionaire CEO of your company? The professional athlete, musician, or movie star?

Sure, all of these people are, in a financial sense, "wealthy."

But money doesn't have a monopoly on wealth. Wealth is defined as "an abundance of valuable material possessions or resources," but nowhere in this definition is money listed as the singular valuable possession or resource.

Six Types of Wealth

Author Jack Raines September 01, 2022

Wealth /welTH/ noun: An abundance of valuable material possessions or resources

Merriam-Webster Dictionary

Being rich isn't just a money thing. What comes to mind when you think of wealth? A list of America's ten richest people? Your neighbor with the bigger house, nicer car, and mountain home in Aspen? The multimillionaire CEO of your company? The professional athlete, musician, or movie star?

Sure, all of these people are, in a financial sense, "wealthy."

But money doesn't have a monopoly on wealth. Wealth is defined as "an abundance of valuable material possessions or resources," but nowhere in this definition is money listed as the singular valuable possession or resource.

Which resources you consider valuable is just as important as the abundance of resources themselves. The key is optimizing for the right form of wealth.

Money

Money is the simplest, most obvious form of wealth, because it can be quantified.

How much is your salary? $100,000.

How expensive was your house? $500,000.

How much was your kid's college tuition? $50,000.

How much is your portfolio worth? $250,000.

Forbes tracks the world's richest people in real-time, so everyone can see just how much money the uber-wealthy have. A hedonic scoreboard for a game that never ends.

Because monetary wealth is so visible, it becomes a point of comparison. Money is the only form of wealth that allows you to look at your neighbor and say "I am richer/poorer than him."

Subconsciously, money becomes a competition. Like any other competition, we want to beat our peers. Make more money. Acquire more possessions. Indulge in more pleasures. Anything to win the game.

What gets missed is that beyond a certain point, money is a seductive scoreboard but a poor measure of wealth. It has diminishing returns. We expect satisfaction from money to look something like this:’

To continue reading, please go to the original article here:

The Money Value of Time

The Money Value of Time

Maybe you should spend more money.

Author Jack Raines November 01, 2022

The Time Value of Money is a core principle of finance that shows us how much the value of an investment will change between two points in time given an expected annual return.

The time value of money plays a role in every branch of finance. Mortgages and car loans are amortized over time. 401k plans suggest estimated contributions needed for your portfolio to hit your retirement goals. Investors discount the future cash flows of companies to estimate their fair values, and companies discount the future cash flows of projects to determine if they are worth undertaking.

The time value of money is also the basis for most mainstream personal finance advice: spend less now to have exponentially more later.

The Money Value of Time

Maybe you should spend more money.

Author Jack Raines November 01, 2022

The Time Value of Money is a core principle of finance that shows us how much the value of an investment will change between two points in time given an expected annual return.

The time value of money plays a role in every branch of finance. Mortgages and car loans are amortized over time. 401k plans suggest estimated contributions needed for your portfolio to hit your retirement goals. Investors discount the future cash flows of companies to estimate their fair values, and companies discount the future cash flows of projects to determine if they are worth undertaking.

The time value of money is also the basis for most mainstream personal finance advice: spend less now to have exponentially more later.

Over time, this has led to a deluge of advice that vilifies whimsical spending and deifies stinginess.

"Don't buy your coffee from Starbucks!" screams an army of Dave Ramsey acolytes. "That $50 per month will cost you $221,575 in 40 years!"

"Pour every nonessential dollar into your index funds!" shouts the FIRE movement's loudest supports. "Every dollar spent now just pushes your retirement back further."

And over time, well-meaning advice such as "Spend less than you make" has been warped into "Never spend or else." And when you preach this long enough, people begin to believe it.

I, like most young people, grew up viewing money as this scarce asset that should be treasured and put away for safe keeping. Save every dollar, don't overspend on anything, you know the drill. Make sure everyone else in your Uber Venmo's you. Obsess over the cash in your checking account every week.

In hindsight, it was irrational for me to be worried about money. In college, I was an upper-middle class kid with a full scholarship. Realistically, I would land a relatively high paying job as a 22-year-old college graduate and be good-to-go.

But when frugality is portrayed as the sole important value in personal finance during your formative years, you tend to conform to this standard.

This mindset stuck with me after college into my first job. Better max out that 401k and watch your weekend spending! You know, the same stuff that every other 23-year-old thinks while working their first job.

Now, if you've followed me for a while, you know what happens next. It's a story that I've told a million times, but here we go again:

I made a bunch of money trading spacs during covid and then lost half of it but i still had enough money to just quit working for a year so i lived out of a backpack in europe and south america for a year because that seemed like the most logical decision for a 24 year old who had enough money that they didn't need to work for a year and now i'm writing this blog.

I've talked about this experience in several blog posts, and I have recounted the story on a dozen podcasts. Make money, lose money, travel, start writing, here we are today. What I haven't discussed is just how much this moment altered my perception of money.

As I mentioned above, we are trained to put frugality above all else from an early age, and it isn't until you reach the point where you no longer need to be frugal that you realize just how dangerous pure frugality is.

Most people don't reach this point until retirement, but thanks to my savvy ability to buy stocks that went up, I was able to briefly experience this sensation at 23. So today, I'm going to let you in on a little secret:

When you have enough money that you no longer have to be frugal, and you are staring at those numbers behind the dollar sign, you can only think one thing: now what?

Our careers are built around the idea of acquiring as much capital as possible, but it is only once you are finally done acquiring capital, and you are contemplating what to do next, that you realize an important truth:

You can't eat money, you can't breathe it, and you can't have sex with it. Money, on its own, can't entertain you. It can't make you laugh, cry, or smile. Money alone can't provide you with fond memories, and it will never set your soul on fire. You can't form a relationship with money (many have tried, but money never returns the love that it receives).

Money, in and of itself, is shockingly worthless.

However, money can be exchanged for something infinitely valuable: experiences.

To continue reading, please go to the original article here:

5 Reasons You Should Work for as Long as You Live

5 Reasons You Should Work for as Long as You Live

These benefits might make you think twice about retirement.

Alex Valdes • November 3, 2021

While countless workers dream of retirement, millions more have decided to work full time or part time after age 65:

In fact, the U.S. Bureau of Labor Statistics predicts that by 2024, there will be about 13 million working Americans age 65 and older. Working longer might be your best option. Here are several reasons why.

5 Reasons You Should Work for as Long as You Live

These benefits might make you think twice about retirement.

Alex Valdes • November 3, 2021

While countless workers dream of retirement, millions more have decided to work full time or part time after age 65:

In fact, the U.S. Bureau of Labor Statistics predicts that by 2024, there will be about 13 million working Americans age 65 and older. Working longer might be your best option. Here are several reasons why.

1. Increase financial security

If you’re worried about outliving your savings, working longer is the answer. It can let you:

Wait to collect Social Security. Delaying claiming your benefits until age 70 earns you payments that are much larger than if you had started claiming at or before your full retirement age.

Keep adding to your retirement savings.

Leave your nest egg untouched longer. This means having more money to use later and giving your savings more time to grow and compound.

A couple of years ago, MarketWatch cited these findings from the National Bureau of Economic Research:

“The longer you work, the longer you can add to your retirement savings, the more time they have to grow, and the less you will need when you eventually retire. Throw in the boost to Social Security as well, and ‘delaying retirement by one year is roughly 3.5 times as impactful as saving an additional 1% of wages for 30 years,’ calculated financial researchers recently.”

2. Stay sharp

A job gives you projects to complete, tasks to perform, deadlines to meet and co-workers to team up with.

To continue reading, please go to the original article here:

https://www.moneytalksnews.com/7-clever-ways-to-fix-your-finances-in-10-minutes-or-less/

Using Financial Therapy to Deal With Money Issues

Using Financial Therapy to Deal With Money Issues

A financial therapist can help you get to the root of your problem

By Pat OlsenJune 26, 2019

Financial Therapy

Like many married couples, Stephen and Kathy Read of Wayne, Pa., knock heads about money. Stephen, a retired engineer in his mid-70s, is a spender. Kathy, a musician in her mid-60s, is frugal. In 2016, they decided to talk to a money therapist. “They’re supposed to know about these things,” says Stephen.

Meeting with the financial therapist, the Reads say, was a huge help. Stephen says he came away realizing that he and his wife “kind of complement each other.“ Now, he says, he has “great respect” for her financial caution.

Using Financial Therapy to Deal With Money Issues

A financial therapist can help you get to the root of your problem

By Pat OlsenJune 26, 2019

Financial Therapy

Like many married couples, Stephen and Kathy Read of Wayne, Pa., knock heads about money. Stephen, a retired engineer in his mid-70s, is a spender. Kathy, a musician in her mid-60s, is frugal. In 2016, they decided to talk to a money therapist. “They’re supposed to know about these things,” says Stephen.

Meeting with the financial therapist, the Reads say, was a huge help. Stephen says he came away realizing that he and his wife “kind of complement each other.“ Now, he says, he has “great respect” for her financial caution.

lso, as a result of their sessions, the couple were motivated to visit a financial adviser. That helped, too. Theirs is a second marriage for both and the pair had kept their assets separate since getting married, but the adviser recommended combining them.

“I didn’t think Kathy would want that, but she did it, and it really brought us together. Everything is more out in the open now,” Stephen says.

“Financial therapy normally involves talking with people about the beliefs they formed about money in childhood.”

If you have money issues that are stressful, you might want to consider seeing a financial therapist, too.

What Is Financial Therapy?

So, what exactly is financial therapy? And who offers it?

The Financial Therapy Association (FTA) describes financial therapy as “a process informed by both therapeutic and financial competencies that helps people think, feel, and behave differently with money to improve overall well-being through evidence-based practices and interventions.”

Put simply, according to FTA President Meghaan Lurtz, financial therapists help with emotional and relationship issues surrounding money. The work normally involves talking with people about the beliefs they formed about money in childhood.

Practitioners include mental health professionals such as psychologists and marriage and family therapists, as well as financial consultants and advisers. They can choose to become a Certified Financial Therapist after completing a program offered by colleges and, as of recently, the FTA, and then passing a test.

Why People See Financial Therapists

Financial therapists say people see them for a variety of reasons.

To continue reading, please go to the original article here:

A Lesson In Learning To Say "No"

A Lesson In Learning To Say "No"

Nov 24, 2014 Tim Keown ESPN Senior Writer

(Note: This Article can apply to Lotto-Winners, A Big Inheritance and Dinarians!)

HERE'S A CHALLENGE: Imagine what it feels like to be 21 years old, extremely successful, famously wealthy, wildly stressed and unbearably miserable. How, you might wonder, can all those conditions exist simultaneously?

Start here, with Cowboys All-Pro offensive tackle Tyron Smith, talking to his mother on the phone one day in 2012, his second year in the NFL, during a time of growing tension between him

A Lesson In Learning To Say "No"

Nov 24, 2014 Tim Keown ESPN Senior Writer

(Note: This Article can apply to Lotto-Winners, A Big Inheritance and Dinarians!)

HERE'S A CHALLENGE: Imagine what it feels like to be 21 years old, extremely successful, famously wealthy, wildly stressed and unbearably miserable. How, you might wonder, can all those conditions exist simultaneously?

Start here, with Cowboys All-Pro offensive tackle Tyron Smith, talking to his mother on the phone one day in 2012, his second year in the NFL, during a time of growing tension between him

"We've found a house," Frankie Pinkney told her son.

By this stage, wariness had become as intrinsic to Smith's identity as his brown eyes and bookcase shoulders. Silently, he awaited details. He had agreed to purchase a home in Southern California for his mother and stepfather. They would live in it; he would own it as an investment.

The agreed-upon budget was roughly $300,000, but over the course of the conversation, Frankie dropped the bomb. List price: more like $800,000.

Smith, now 23, is sitting at a polished wood table in the conference room of his lawyer's Dallas office. Surrounded by his girlfriend, accountant and lawyer, he fixes his eyes on a spot somewhere high on the floor-to-ceiling window. "Yeah, my parents wanted a house," Smith says. "But it was way bigger than mine and cost way more than mine."

It's not an easy topic for Smith to discuss -- recounting the conversation appears to be nearly as hard as being on the phone in the first place. He long ago gave up trying to pinpoint when it all went wrong, when the combination of family and money turned corrosive, when one ceased to exist without the other. He recites facts, stripped of emotion, as if determined to turn a painful time in his life into an after-action report.

"That call," he says. "That was the point where I said, 'That's enough.'"

At that precise moment, as he hung up the phone without giving his mother assent or encouragement, something hardened inside him. Reclaiming his finances, that was the easy part. Demystifying his new life -- being something other than a conduit for the wishes of those around him -- that was more complicated.

It works like this: We lack the linguistic dexterity to explain the myriad paths of young men who emerge from poverty -- or a simple lack of privilege -- and achieve riches by playing a game. When words fail us, a creation myth must fill the void, and so the modern professional athlete becomes our Sedna, a massive woman of Inuit legend who lives at the bottom of the ocean, controlling the underworld by providing fish to keep her people from going hungry.

Our version of Sedna frees himself from the streets -- the temptations, the poverty, the turbulent flow of every Bad Part of Town -- through a ceaseless, unquenchable devotion to his sport. Visions of The Escape accompany every rep on the bench press, every free throw in an empty gym. In short, his life is a series of made-in-Akron, Beats by Dre moments.

Yes, he will rise up to leave it all behind, but here's where the mythological sleight of hand appears: He'll bring it all with him too. He can't forget where he came from. The myth mandates loyalty and strikes down the ingrate.

And all those people who toiled alongside, those who believed in him and sheltered him and sacrificed for him? They'll also come along, for he's the sin-eater, absorbing all debts -- moral and financial -- so others can be absolved. And his people will never go hungry again.

Jeff Wilson His family's demands for money isn't an easy topic for Smith to discuss.

IT LONG AGO became easier for an athlete to subscribe to this myth than to defy it with his personal story. Easier to nod and smile and tacitly agree to be a benign receptacle for our society's need to bundle its fairy tales into color-coded boxes.

Why else would newly minted professional athletes -- and let's cut the pretense: It's nearly always young black athletes -- invariably be asked whether they've bought their mother a new house? Or a new car? Or both? Does anyone know whether Aaron Rodgers moved his stay-at-home mother and chiropractor father out of their Chico, California, home and into a beach mansion? Has anyone ever thought to ask?

But could it be possible, ever so slightly possible, that athletes who come from similar backgrounds can have wildly dissimilar stories?

Smith's story is best told chronologically. And it begins, as so many do, in a van filled with cleaning supplies rattling down a desolate highway somewhere in the Mojave Desert.

To continue reading, please go to the original article here:

4 Steps to Make Your Money Last a Lifetime

4 Steps to Make Your Money Last a Lifetime

By Jane Bryant Quinn, AARP Bulletin

A simple, easy-to-use formula to make sure you never run out of cash

As a financial columnist, I get asked the same heartfelt question over and over: “How do I make sure I don’t outlive my money?” And that makes sense. Surveys confirm that the No. 1 worry among older Americans is running out of cash.

Fortunately, financial planners have come up with sound ways to prevent this. Collected here are their key rules for maintaining a livable income for life, plus case studies that show how to put these general rules into action. The goal is your peace of mind — knowing that you’re getting the most from the money you’ve saved and that you’ll always have enough.

4 Steps to Make Your Money Last a Lifetime

By Jane Bryant Quinn, AARP Bulletin

A simple, easy-to-use formula to make sure you never run out of cash

As a financial columnist, I get asked the same heartfelt question over and over: “How do I make sure I don’t outlive my money?” And that makes sense. Surveys confirm that the No. 1 worry among older Americans is running out of cash.

Fortunately, financial planners have come up with sound ways to prevent this. Collected here are their key rules for maintaining a livable income for life, plus case studies that show how to put these general rules into action. The goal is your peace of mind — knowing that you’re getting the most from the money you’ve saved and that you’ll always have enough.

The Magic Number

The key to long-term planning is knowing one essential number: how much money you can afford to spend annually. From there, you can adjust your expenses to fit.

You may be tempted to reverse the order — estimate your future expenses, then adjust your investment assumptions to make that spending appear possible. But that’s wishful thinking: a hope that big investment returns will rescue your budget. It leads to overspending early on, and regret later.

Instead, let’s focus on the real, guaranteed money you’ll have. There are two main sources:

Your personal savings and investments.

Your guaranteed income from other sources.

Download this worksheet to help you find your sustainable income. The key steps:

Step 1: Tally Your Guaranteed Income

The most common source is Social Security, which you may already be collecting. (If you’re not, get an estimate by calling Social Security or by opening a My Social Security account at ssa.gov.) You might also have a pension or annuity.

If you own a reliable rental property, include the amount of rent you receive after expenses.

Step 2: Estimate Your Income from Savings

How much annual income can you prudently take from your savings and investments? To get the answer, there’s a surprisingly simple rule of thumb:

Add up the current value of your spendable assets, such as bank accounts, mutual funds, stocks and bonds. Include both retirement and nonretirement savings.

Subtract from that total a cash cushion to help cover near-term expenses.

Then take 4 percent of what remains.

That’s the “safe” amount of your assets that financial planners say you can afford to spend in the first year of retirement without running the risk that your savings will run out. In each subsequent year, take the same dollar amount plus an increase for inflation.

Example: Say you have $100,000 invested (plus a cash cushion). In the first year of retirement you could spend $4,000 of that money. If inflation is running at 3 percent, your second-year withdrawal would be $4,120 — the first-year amount plus an inflation increase. Follow this pattern in each future year.

To continue reading, please go to the original article here:

https://www.aarp.org/retirement/retirement-savings/info-2018/make-money-last-lifetime.html

How To Become A Personal Finance “Black Belt”

How To Become A Personal Finance “Black Belt”

Written by Sam Getting Finances Done

David Allen in “Getting Things Done” compares productivity to the martial arts. He gives instruction on how to become a black belt in your personal productivity with a “mind like water” that allows you to handle anything that comes your way with a balanced response. When a stone is thrown into a pond, the water reacts with perfect balance. It reacts just enough to disperse the energy, no more, and then returns to a calm state. It doesn’t over or under react. Becoming a black belt and having a “mind like water” in your personal finances is very similar. It means you can take whatever is thrown at you without knocking your finances out of control. You can respond to any situation with perfect balance.

How To Become A Personal Finance “Black Belt”

Written by Sam Getting Finances Done

David Allen in “Getting Things Done” compares productivity to the martial arts. He gives instruction on how to become a black belt in your personal productivity with a “mind like water” that allows you to handle anything that comes your way with a balanced response. When a stone is thrown into a pond, the water reacts with perfect balance. It reacts just enough to disperse the energy, no more, and then returns to a calm state. It doesn’t over or under react. Becoming a black belt and having a “mind like water” in your personal finances is very similar. It means you can take whatever is thrown at you without knocking your finances out of control. You can respond to any situation with perfect balance.

Unexpected events or changes in your finances, good or bad, can be handled with optimum efficiency, and little or no stress. It means you can direct the flow of money where you need it almost effortlessly.

In an effort to help people gauge where they are in their personal finance development, I’ve defined what people at the various “belts” might look like. Where are you?

White Belt

You’ve recognized there is a problem with your finances and have committed to taking control. Recognition that there’s problem may come as a nagging doubt that you’re not meeting all your financial goals or a harsh reality check as you face mounting debt.

You have a lot of stress concerning finances (even if you’re living within your means). You tend to fight with your spouse every time you discuss financial matters. You recognize your spending isn’t in line with your true values. You have no idea where all the money goes from month to month.

You may be living paycheck to paycheck. If you saved $5 on your phone bill, it would just disappear somewhere but you don’t know where. Your idea of an emergency fund is a credit card or Home Equity Line of Credit. You frequently pay late fees on your bills and unnecessary bank fees. Net worth? What’s that?

Despite your lack of financial control, you have a strong resolve to take action even though the thought of facing the “deep mess” of your finances seems overwhelming. You and your spouse have agreed to work together. In an effort to get your spending under control, you’ve started using cash for your “out-of-control” budget categories.

You’ve stopped using credit cards somewhat reluctantly and possibly out of the sheer pain of your dire financial straights. Despite some complaining, your family has agreed to use cash as well. You’ve taken initial steps to figure out what your basic monthly income and expenses are and have tried budgeting for at least one month even though it doesn’t match reality yet.

Most importantly, you’re no longer willing to BE IN DEBT!

You’re no longer willing to constantly WORRY ABOUT MONEY!

You’re no longer willing to FIGHT ABOUT MONEY!

You’re no longer willing to PAY LATE FEES!

You’re committed to TAKING RESPONSIBILITY FOR YOUR FINANCES!

You’re committed to WORKING THROUGH FINANCIAL ISSUES TOGETHER WITH YOUR SPOUSE!

To continue reading, please go to the original article here:

Benefits of a Cash Budget – Part 2

Benefits of a Cash Budget – Part 2

Written by Sam Getting Finances Done

Be sure to check out part 1 about the benefits of a cash budget. In that article I explain how cash is the ultimate tool to help you control your spending and staying within your budget.

In part 2, I explain how budgeting will help save you time in the budgeting process.

How Cash Will Cut Your Budgeting Time By 80%

Think for a second about entering transactions into financial software like Quicken or YNAB. What are most of the transactions? By far the majority of the transactions come from categories like groceries, household, or entertainment.

Benefits of a Cash Budget – Part 2

Written by Sam Getting Finances Done

Be sure to check out part 1 about the benefits of a cash budget. In that article I explain how cash is the ultimate tool to help you control your spending and staying within your budget.

In part 2, I explain how budgeting will help save you time in the budgeting process.

How Cash Will Cut Your Budgeting Time By 80%

Think for a second about entering transactions into financial software like Quicken or YNAB. What are most of the transactions? By far the majority of the transactions come from categories like groceries, household, or entertainment.

They are purchases at the grocery store, or walmart, or the corner convenience store. What if you took those transactions away. For most people, there are only a handful or two of transactions left that occur every month. You might have utilities, a cell phone bill, a few gas transactions, but that’s about it.

Most of Your Transactions Come From Just a Few Categories

This is a classic 80/20 example. 80% of your transactions come from 20% of your budget categories. In fact, I would guess that for many people it’s more of a 90/10 rule. 90% of their transactions come from 10% of the categories. If you’ve used financial software in the past, go check this out and see if it holds true. In fact, leave a comment and let me know if it’s true. I know for us it IS true.

Now I want you to think about the time you spend budgeting every month and what that time is spent on. If you’re like us it’s spent on entering and/or categorizing transactions from the previous month. It’s spent tracking down transaction #x and finding out what it was for. Either you don’t remember or your spouse spent it and he/she doesn’t remember. You spend time tracking down missing receipts. It’s all a big mess.

Well all of that craziness doesn’t have to be. In fact, I’m going to give you permission to stop entering every transaction. How can I do that? Well let me ask this: why do you need to enter all those transactions? Do you really want to know how much you spend on milk every month?

Do you ever really care to know on an itemized basis what individual items you purchased in your grocery category? I don’t think that’s the case. If you think about it, all you really care about is spending the amount you want to spend in any given category. Well I’ve just shown that you can accomplish this goal by using cash.

You don’t accomplish this goal by tracking every little thing, if fact, doing so is a lag measure and won’t have any impact on how much you spend next month. You’ll just go through the same process taking a lot of time and experiencing the same or similar results.

One Entry To Rule Them All

To continue reading, please go to the original article here:

http://www.gettingfinancesdone.com/blog/archives/2010/04/benefits-of-a-cash-budget-part-2/

Benefits of a Cash Budget – Part 1

Benefits of a Cash Budget – Part 1

Written by Sam Getting Finances Done

In this article series of articles, I have recorded somewhat of a manifesto for using cash in your budget. You can listen to the whole thing in my podcast for week 4 of my 12 Weeks to Fiscal Fitness program, Using Cash In Your Budget.

In week 3 I talked in considerable detail about how to create a budget that works. In week 4, I’m going to talk about a tip that has been crucial in helping my wife and I stay within our budget. It has also helped us decrease the total time we spend on budgeting from month to month.

Benefits of a Cash Budget – Part 1

Written by Sam Getting Finances Done

In this article series of articles, I have recorded somewhat of a manifesto for using cash in your budget. You can listen to the whole thing in my podcast for week 4 of my 12 Weeks to Fiscal Fitness program, Using Cash In Your Budget.

In week 3 I talked in considerable detail about how to create a budget that works. In week 4, I’m going to talk about a tip that has been crucial in helping my wife and I stay within our budget. It has also helped us decrease the total time we spend on budgeting from month to month.

That’s right, I’m talking about using cash in your budget.

If you’ve been following this program faithfully, you’re already using cash in your budget. In week 1 I challenged you to use cash for your groceries and to choose to other problematic categories to use cash in. Now, I’ll finally go into the reasons for using cash.

Using cash in your budget is a tough topic. People shy away from it and toss it aside as being too much of a hassle. I want to challenge you to put those beliefs aside for a moment and let me make a case for using cash.

The fact is, I know how you feel. Using cash in our budget was one of the things I fought against most. We started using cash as part of Financial Peace University. It was one of those concepts I was ready to ignore and tried to convince my wife that we shouldn’t use cash. But she wanted to give it a shot and since I’d agreed to follow the program, I reluctantly went along.

I’m glad I did.

It quickly became clear how powerful using cash in your budget is. I was quickly converted and became a big advocate for using cash. In fact, I now consider it a requisite for having an effective budget. REALLY! I don’t know a single family who considers themselves successful at budgeting that doesn’t use cash.

On the flip side, I know plenty of people who struggle with their budget or struggle staying within their spending limits and are always trying to figure out why. Yet, they resist using cash. They just won’t give it a try. Or they give it a half-hearted try and quickly give up.

How We Saved $6,000 In One Year By Using Cash

To continue reading, please go to the original article here:

http://www.gettingfinancesdone.com/blog/archives/2010/04/benefits-of-a-cash-budget-part-1/

11 Guidelines For Using Cash In Your Budget

11 Guidelines For Using Cash In Your Budget

Written by Sam Getting Finances Done

Here’s how to tell in which categories you should use cash.

1. You Don’t Have To Use Cash For Everything

To reap the benefits of using cash in your budget, you don’t have to go exclusively to cash. Some may choose to go exclusive, but it’s not necessary. Instead, identify which categories will be most effective for using cash using the tips below. You should use cash for categories where either you tend to overspend or where there are a lot of transactions in a month.

11 Guidelines For Using Cash In Your Budget

Written by Sam Getting Finances Done

Here’s how to tell in which categories you should use cash.

1. You Don’t Have To Use Cash For Everything

To reap the benefits of using cash in your budget, you don’t have to go exclusively to cash. Some may choose to go exclusive, but it’s not necessary. Instead, identify which categories will be most effective for using cash using the tips below. You should use cash for categories where either you tend to overspend or where there are a lot of transactions in a month.

Groceries are a main perpetrator of both those criteria which is why I absolutely recommend funding that category with cash. Other problem categories are ones relating to household spending (light bulbs, cleaning products, etc), eating out, personal, and entertainment.

There are actually some categories where it is easier to NOT use cash. Specifically I’ll mention gas for your car. At first Emily and I used cash for gas but found it to be significantly more inconvenient, especially during the winter.

After looking at our gas spending we realized that we don’t tend to overspend on gas. Our gas budget went up and down depending on the price of gas, but we weren’t more likely to drive less by using cash. I still had to commute to and from work no matter what and we don’t take a lot of trips.

Gas purchases also weren’t hard to track in our financial software. We knew that if the transaction was at Texaco it was gas so it didn’t add any confusion at the end of the month. In the end we decided that it wasn’t worth it to use cash and now use a debit card.

Some categories are on the edge and could go either way. For example, haircuts is a category that I think should not be cash, but Emily likes it in cash. From my perspective it’s not hard to track haircut transactions. A transaction at SportsClips is self-evident. There aren’t a lot of haircut transactions. At most I will get one and Emilyi will get one. I’m also not likely to overspend and get haircuts more often if I’m not using cash. For me, this category doesn’t need to be in cash.

For Emily that’s not the case. She is more likely to get a haircut or styling if there’s money available for it. She also will let money accumulate from month to month and then get her hair colored with the extra money. She likes having the money in cash because as it accumulates it gives her permission to do something extra without guilt. Therefore, Emily prefers to have this category in cash.

To continue reading, please go to the original article here: